Paying a global team through banks means FX spreads, 3–5 day waits, intermediary fees, and a recipient in another country who receives less than you sent. Paying them in USDC — a fully-reserved, dollar-pegged stablecoin — can turn that into a same-day transfer for cents. But doing it properly, at scale, and in a way your accountant accepts takes more than a wallet.

This guide walks through how to pay contractors in USDC — the setup, the networks, the compliance basics, and how to keep your books in fiat.

Why businesses pay in USDC

USDC (issued by Circle) is a stablecoin pegged 1:1 to the US dollar and backed by cash and short-dated US Treasuries, with monthly attestations from Deloitte. For paying people, that combination is the point:

Stable value. Recipients get dollars, not a volatile asset. 1 USDC ≈ $1 at send and at cash-out.

Speed. Payments settle in minutes, 24/7, including weekends and holidays.

Global reach. Anyone with a wallet can receive, regardless of local banking.

Low cost. On low-fee networks, a payout costs cents rather than a wire fee.

Regulatory standing. USDC is MiCA-compliant in the EU, which makes it a durable choice for European corridors (more on that below).

Before you start: four things to get right

1. Confirm the recipient can receive USDC. They need a wallet address on a network you both support (Ethereum, Solana, Base, Polygon, and others). Confirm the network explicitly — a USDC transfer sent to the wrong network can be lost.

2. Decide who bears the fee. Will you gross up payments so the contractor receives the full agreed amount after network fees, or net it out? Set this in the contract.

3. Handle tax and classification. Paying in stablecoin doesn't change worker classification or your reporting obligations. Contractors are still responsible for their own taxes; you still keep records. Treat USDC payouts like any other payment for compliance purposes.

4. Keep fiat records. Your accounting should capture the fiat value at the time of payout, the fee, the recipient, and the transaction hash — not just on-chain data.

Method 1: Manual USDC payments

For a few contractors, you can pay directly from a self-custody wallet or exchange.

Steps:

Fund a wallet with USDC and the network's gas token.

Confirm each contractor's address and network in writing.

Send each payment; send a small test transfer first for new, large recipients.

Record each transaction hash against the invoice and its fiat value.

Limits: no automation, no built-in screening, and manual reconciliation. It works for a handful of people and breaks down beyond that.

Method 2: Bulk USDC payouts via CSV or API

For a real team — dozens or thousands of contractors, affiliates, or creators — a payout platform is the practical route. You prepare a recipient list and process it as one batch.

A typical flow:

Fund in fiat. With a fiat-native provider like INXY, top up in EUR or USD via SEPA or SWIFT — no need to buy crypto yourself.

Upload a CSV or call the API. Include recipient, amount, and network. The API path lets you trigger payouts straight from your own platform or billing system.

Automated compliance. The provider runs KYT and sanctions screening and validates addresses before sending.

Recipients get paid. USDC lands in minutes on supported networks.

Reconcile in fiat. Export batch-level records with fiat values, fees, payout IDs, and hashes.

This removes the two hardest parts of paying a global team in crypto: compliance and accounting. You never manage keys or gas, and your finance team works in EUR or USD.

Choosing the network for USDC payouts

USDC runs natively on several chains. For payouts:

Solana / Base / Polygon: cents per transfer, fast — ideal for high-volume contractor and affiliate payments.

Ethereum (ERC-20): the most liquid and widely integrated, but the most expensive — reserve it for recipients who require it.

Match the network to the recipient's wallet and the payout size; a platform can route this automatically.

Compliance: don't skip screening

Paying contractors across borders means you're exposed to sanctions and AML rules. Two non-negotiables:

Sanctions screening of recipient wallets before payout.

Transaction monitoring (KYT) to flag high-risk addresses.

Manual and script-based payouts leave this to you. A regulated payout provider builds it into the flow — which is often the difference between "using crypto rails" and "creating a banking-risk problem."

Frequently asked questions

Can I pay international contractors in USDC? Yes. Anyone with a compatible wallet can receive USDC in minutes, regardless of country, as long as it's legal in their jurisdiction. It's widely used for cross-border contractor, freelancer, and affiliate payments.

Do I need to hold crypto to pay contractors in USDC? No. A fiat-native platform lets you fund in EUR or USD and keep accounting in fiat while recipients receive USDC.

Is paying contractors in USDC legal? Paying in USDC is legal in most jurisdictions, but you remain responsible for worker classification, tax reporting, and AML/sanctions compliance — the same as any payment method. Check local rules for your recipients.

What does it cost to pay someone in USDC? On low-fee networks like Solana, Base, or Polygon, a USDC transfer costs cents. On Ethereum it can be several dollars. Choosing the network controls the cost.

How do I keep accounting clean when paying in USDC? Record the fiat value at payout time, the fee, and the transaction hash for each payment. Payout platforms generate these exports automatically.

Pay your global team without the crypto overhead

If you're paying contractors, affiliates, or creators at scale, you shouldn't be managing wallets, gas, and screening by hand. INXY's mass USDC payouts let you fund in fiat, pay globally in minutes, and reconcile in EUR or USD — with compliance built in. Building a broader payroll flow? See our contractor payroll solution, or weigh the assets in our USDT vs USDC comparison.

MiCA Is Here: How INXY Built a Multi-Jurisdiction Model — and Migrated Every Client Before July 1

1 July 2026. Today marks the beginning of a new chapter for Europe's digital asset industry. The transitional period under the EU's Markets in Crypto-Assets Regulation (MiCA) has ended, and the standard for operating a crypto business in Europe has been raised for good.

1 July 2026. Today marks the beginning of a new chapter for Europe's digital asset industry. The transitional period under the EU's Markets in Crypto-Assets Regulation (MiCA) has ended, and the standard for operating a crypto business in Europe has been raised for good.

For years, much of the industry was built around a single jurisdiction. One license. One operating model. That worked while the rules were still evolving. It works less well now.

We want to be transparent with our clients about where INXY stands and what we did about it. INXY did not obtain a MiCA authorization in Poland. So rather than depend on any single jurisdiction, we moved to a multi-jurisdiction operating model — and before 1 July, we completed the migration of every client off our Polish entity. No payments paused. No settlement stopped.

Here's what MiCA is, what changed on 1 July, and how our model is built to keep your payments running through moments exactly like this one.

What is MiCA?

MiCA (Markets in Crypto-Assets Regulation) is the European Union's comprehensive framework for regulating crypto-assets and the companies that provide crypto services. It replaces a patchwork of national rules with a single, harmonized rulebook across all 27 member states.

In practice, MiCA does three main things:

Licenses providers. Any company offering crypto-asset services — custody, exchange, transfers, payouts — must be authorized as a Crypto-Asset Service Provider (CASP) by a national regulator. A CASP license can then be "passported" across the EU.

Regulates stablecoins. Issuers of stablecoins ("e-money tokens") must be authorized and hold strict, fully-backed reserves. This is why compliant stablecoins like USDC and EURC stayed available on EU-regulated venues while non-authorized ones were delisted. (More on this in "Is USDC regulated?")

Sets conduct and transparency standards for how services are marketed and delivered.

MiCA's rules for service providers began applying on 30 December 2024, with a transitional window for existing firms.

What changed on 1 July 2026

MiCA included a transitional ("grandfathering") period under Article 143. Firms already operating legally under national regimes before 30 December 2024 could continue serving clients — but only until they obtained a CASP license or until 1 July 2026, whichever came first. That date has now passed, and there is no extension mechanism in the regulation.

From today, any provider serving EU clients must hold a MiCA CASP authorization. A legacy national registration no longer provides cover.

The situation in Poland made this especially clear. Poland has not yet enacted the national Crypto-Asset Market Act needed for its regulator (KNF) to issue CASP licenses — the act has been vetoed repeatedly, most recently in June 2026. In practice, that left Polish-registered providers with no domestic path to a CASP license before the deadline.

The limits of a single-jurisdiction model

MiCA is not simply making it harder to launch a crypto business. It is redefining what it means to run one: no longer just "get a license and go," but "operate reliably inside a regulated financial system."

That shift began well before 1 July. Across the market, some companies are spending the coming months restructuring. Some are migrating clients. Some are rethinking how they serve Europe altogether. The common thread is that betting an entire operation on one jurisdiction has become a single point of failure.

INXY's response: a multi-jurisdiction operating model

For payment infrastructure providers, continuity is not optional. Payments cannot pause because the regulatory landscape changes. Businesses still need to settle funds. Cross-border commerce continues every day. Infrastructure should adapt so that businesses don't have to.

That is why INXY expanded beyond a single jurisdiction and built a multi-jurisdiction operating model, spanning:

Canada — registered Money Services Business (FINTRAC MSB M23375535)

El Salvador

Cyprus

Switzerland

We did not build this because a deadline forced our hand at the last minute. We built it because our B2B clients need reliability that does not depend on the regulatory status of any one country. When the Polish route closed, that model is what let us complete the migration of all clients off our Polish entity before 1 July 2026 — with no interruption to payouts, settlement, or reporting.

What this means for you

Your service continues. Clients were migrated ahead of the deadline and are served through our appropriately licensed entities. There is no gap in payouts or settlement.

Your funds and reporting are unaffected. Fiat-denominated reporting, payout records, and reconciliation continue exactly as before.

Your compliance standards are unchanged. Full KYB, KYC where needed, real-time transaction monitoring (KYT), and sanctions screening remain in force across every jurisdiction we operate in.

Regulation is becoming the foundation, not the obstacle

One conclusion runs through all of this: regulation is no longer just about compliance. It is becoming the foundation that enables institutional adoption of stablecoin infrastructure at scale. The businesses that treat regulatory resilience as core infrastructure — not paperwork — are the ones that will serve the next phase of the market.

That's the central theme of our latest research, Stablecoins 2026: The New Global Financial Settlement Layer, which maps the regulatory landscape and what it means for businesses building on stablecoin rails. (Link / request the report: [add URL].)

Frequently asked questions

Did INXY obtain a MiCA license? No. INXY did not obtain a MiCA authorization in Poland. Instead of relying on a single jurisdiction, we operate a multi-jurisdiction model across Canada, El Salvador, Cyprus, and Switzerland, chosen to give our B2B clients continuity.

What happened to clients on the Polish entity? All clients were migrated off our Polish entity before 1 July 2026. The migration was completed ahead of the MiCA transitional deadline, with no interruption to payments.

What is MiCA, in simple terms? MiCA is the EU's single set of rules for crypto companies and crypto-assets. It requires service providers to be licensed as CASPs and sets strict standards for stablecoins, consumer protection, and transparency across all member states.

What happened on 1 July 2026? MiCA's transitional period ended. From this date, providers serving EU clients must hold a MiCA CASP license; legacy national registrations no longer provide cover.

Will my payments pause? No. Continuity was the entire point of moving to a multi-jurisdiction model. Client migration was completed before the deadline, and settlement continues without interruption.

Talk to us

Regulatory change raises real questions for any business that moves money across borders. If you'd like to understand how our multi-jurisdiction model supports your payouts, contact our team — and we'd be glad to share our perspective as the industry enters this new phase.

This update is provided for information and does not constitute legal advice. Regulatory details are accurate as of 1 July 2026 and may evolve.

Crypto Checkout That Converts: Reducing Drop-off on Stablecoin Payments

You added crypto checkout to win new buyers — but the payment page is quietly leaking them. This guide breaks down exactly where stablecoin payments lose customers: network confusion, price-lock anxiety, wallet friction, unclear confirmations, and surprise fees. Learn the design and infrastructure fixes that turn a leaky pay page into one that converts — including why a well-built crypto checkout can beat cards, clearing ~99.9% of attempts with no chargebacks.

You added a crypto checkout to capture a new segment of buyers, and the demand is real — but the payment page is leaking customers. A shopper picks crypto, lands on the pay screen, hesitates, and disappears. That gap between intent and completed payment is checkout drop-off, and on crypto rails it has its own specific causes that most teams never diagnose.

This guide breaks down where stablecoin payments lose customers, the friction points that drive abandonment, and the concrete design and infrastructure choices that turn a leaky pay page into one that converts. The goal is simple: every shopper who chooses crypto should finish paying.

Why crypto checkouts lose customers

A crypto checkout is not just a card form with different logos. It introduces steps a Web2 buyer has never seen — choosing a network, copying an address, waiting for confirmations — and every unfamiliar step is a place to quit. Unlike a card decline, which the customer understands, a stalled or confusing crypto payment feels risky, and risk kills conversion.

Where drop-off actually happens

Most teams treat the checkout as a single event. It isn't. Crypto payment drop-off clusters at four distinct stages:

Method selection — the customer considers crypto but doesn't trust it on your site, so they bounce before starting.

Network and asset choice — faced with "ERC20 / TRC20 / BEP20" they don't recognize, they freeze.

Wallet action — copying an address or scanning a QR code, switching apps, and fearing a mistake.

Confirmation wait — the payment is sent but the page gives no clear signal it worked.

You cannot fix abandonment you can't see. Instrument each of these stages separately before changing anything.

Why a one-point conversion gain is worth chasing

Checkout is the highest-leverage surface you own. Traffic, ads, and product pages all exist to deliver a customer to this screen. Recovering even a few percentage points of crypto payment conversion rate here costs nothing in additional traffic — it simply stops you paying for visitors you then lose at the last step. For a business processing meaningful volume, a high-conversion gateway is not a nice-to-have; it is the difference between crypto being a growth channel and a vanity feature.

The main causes of stablecoin payment drop-off

Network and asset confusion

The single biggest source of friction is choice the customer can't evaluate. Asking a non-technical buyer to select between Tron, Ethereum, BNB Chain, and Polygon — each with different fees and speeds — is asking them to make a decision they're unqualified to make. Hesitation becomes abandonment.

Volatility and price-lock anxiety

If the amount due appears to move while the customer reads it, they assume they'll overpay or underpay. Even with stablecoin payments, buyers worry the quote will expire or shift. Without a visibly locked rate, the page feels unsafe.

Wallet friction and manual errors

Copy the address. Switch to the wallet app. Paste. Check the network matches. Confirm the gas. Send. Switch back. Each handoff is a chance to abandon — and the fear of sending funds to the wrong address or wrong chain is enough to make cautious buyers stop entirely.

Slow or unclear confirmation

A customer who has paid but sees a spinning loader with no explanation assumes the worst. On-chain confirmation times vary by network, and a checkout that doesn't explain the wait — or sets no expectation for it — converts the final, already-committed moment into a drop-off. (For the underlying mechanics, see our guide on how long crypto withdrawals and confirmations take.)

Fees, minimums, and surprise costs

A network fee that appears only at the final step, or a minimum the customer trips over, reads as a bait-and-switch. Surprise costs at the moment of payment are one of the most reliable abandonment triggers in any checkout — crypto included.

Missing trust and compliance signals

Crypto still carries a perception of risk for mainstream buyers. A pay page with no licensing, security, or brand reassurance gives a nervous customer every reason to close the tab. Trust is not decoration here; it is a conversion input.

How to design a crypto checkout that converts

Invoice in fiat, settle in stablecoins

Let the customer see the price in the currency they think in — EUR or USD — and pay in crypto behind the scenes, with automatic conversion to stablecoins or fiat on your side. This removes mental math, neutralizes volatility, and lets a Web2 buyer treat the transaction like any other payment. It is the foundation of a converting crypto checkout.

Reduce choices and default to the right network

Don't make the customer a blockchain expert. Pre-select a fast, low-fee network as the default and present asset options in plain language ("Pay with USDT" rather than "TRC20"). Fewer decisions mean fewer exit points. Every option you remove from the critical path is a conversion you keep.

Lock the rate and show a countdown

Display a fixed amount due with a clear, time-boxed quote ("This price is locked for 15:00"). A visible countdown does two things at once: it removes price anxiety and creates gentle urgency that pulls the customer through. Certainty converts.

Make the confirmation state legible

Tell the customer exactly what's happening: "Payment detected — confirming on-chain. This usually takes under a minute." Replace ambiguous spinners with a status that names the step and sets a time expectation. The moment after a customer pays is the worst possible time to leave them guessing.

Add fallback paths

Some customers will start a crypto payment and stall. Offer a clean way to switch methods or retry without losing the cart. A dead-end on a failed or abandoned crypto payment is a guaranteed loss; a graceful fallback recovers a share of it.

Build trust into the page

Show licensing and security signals where the customer makes the decision. INXY operates as licensed and regulated payment infrastructure with AML/KYB controls and partners including Sumsub, Elliptic, and Crystal — the kind of compliance signal that reassures a cautious buyer at exactly the right moment. Surface it; don't bury it in a footer.

Conversion benchmarks: crypto vs cards

When the checkout is built well, crypto doesn't just match card conversion — it can beat it. The structural advantages are real:

Cards fail far more often than most merchants realize — declines, 3-D Secure friction, and cross-border blocks routinely cost 5–30% of attempts. Crypto settlement is final and irreversible, which removes chargebacks entirely and lets a well-designed gateway clear close to every legitimate attempt. For merchants serving Europe, Asia, and LatAm, that reliability is a direct conversion uplift — INXY reports helping customers increase conversion rates by up to 40%. (For a wider comparison of providers and rails, see best payment gateways for SaaS in 2026.)

A pre-launch checklist

Before you ship a crypto checkout, confirm it does all of the following:

Prices in the customer's fiat currency, with conversion handled automatically.

Defaults to a fast, low-fee network instead of forcing a choice.

Locks the rate with a visible countdown.

Shows total cost up front, including any network fee — no surprises at the last step.

Names the confirmation step and sets a time expectation.

Offers a retry or fallback for stalled payments.

Displays trust and compliance signals on the pay page itself.

Tracks drop-off by stage, not just overall completion.

How INXY reduces crypto checkout drop-off

INXY's high-conversion API paygate is built around the principles above. Customers are invoiced in fiat and pay in crypto, with automatic conversion to stablecoins or fiat to remove volatility risk. You get settled in your bank account — in EUR or USD — as soon as the next day, with full reporting and an accounting-friendly setup for Web2 companies. The gateway supports 20+ cryptocurrencies across major networks (ERC20, TRC20, BEP20, Polygon, Tron, TON, and more), charges below 1% per transaction with no setup or hidden fees, and is engineered for a ~99.9% success rate.

The result is a checkout your customers finish — built to convert, not just to accept. Add it to your checkout page, webstore, platform, or app via API integration, or book a demo to see the conversion data for your business model.

FAQ

What causes drop-off on crypto checkouts? The most common causes are network and asset confusion, price-lock anxiety, manual wallet friction, unclear confirmation states, surprise fees, and missing trust signals. Each maps to a specific stage of the checkout, so the fix starts with measuring drop-off stage by stage rather than as a single number.

How do stablecoin payments improve checkout conversion? Stablecoins remove volatility from the transaction, so the amount due stays fixed while the customer pays. Pairing that with fiat-denominated pricing and automatic conversion lets a mainstream buyer complete a crypto payment as easily as a card payment — without exposure to price swings.

Is crypto checkout conversion really higher than cards? It can be. Crypto payments have no chargebacks and final settlement, and a well-built gateway can clear close to 99.9% of legitimate attempts versus 70–95% typical card success. The advantage is largest for cross-border and emerging-market customers, where cards are frequently declined or restricted.

Which network should a crypto checkout default to? Default to a fast, low-fee network so customers don't have to choose. Stablecoins on high-throughput networks settle in seconds for a fraction of the cost of slower chains, which both speeds confirmation and reduces the fee shown at checkout.

How do I add a high-conversion crypto checkout to my site? Use a payment gateway with API integration that handles fiat pricing, network selection, rate locking, and conversion for you. INXY integrates with your existing checkout, webstore, or app, and settles to your bank in EUR or USD — see get started.

Stablecoin Payments: Why Businesses Switch in 2025

Discover why businesses worldwide are switching to stablecoin payments in 2025. Learn how stablecoins work, their benefits over traditional payments, real case studies, global regulations, and what the future of digital payments looks like

Stablecoin payments are a way to use digital currencies that are pegged to stable assets, like the US dollar. This means their value doesn't swing wildly like other cryptocurrencies. Imagine you're doing business online, and you want to avoid the ups and downs of Bitcoin's value. Stablecoins, like USDC, DAI and USDT, come in handy here. They offer the benefits of crypto without the same level of risk.

These payments work through a crypto payment gateway, which acts like a bridge. It lets businesses accept stablecoins and convert them into local currency if needed. This is helpful for companies that want to tap into the crypto market without holding onto volatile assets.

Think of stablecoin payments as a digital version of cash that you can use globally, without worrying about big price changes. They're fast, often cheaper than traditional methods, and open up new markets for businesses. This makes them a popular choice for companies looking to innovate in 2025. Stablecoins also help people in emerging markets who have no access to traditional banking. Many do not have a bank account, but almost everyone has a mobile phone. Stablecoins give these users a safe and simple way to pay online.

The Rise of Digital Transactions

Digital transactions have become increasingly popular as we move further into the 21st century. People use digital payments to buy things online, pay bills, and even send money to friends. This shift has been driven by the need for faster, more convenient ways to pay.

One example is mobile wallets, which let you store your credit or debit card information on your phone. This makes it easy to pay with just a tap. Businesses are also seeing the benefits. They can reach more customers who prefer digital payments, and they can process transactions more quickly.

Cryptocurrencies like Bitcoin and stablecoins like USDC and USDT offer new ways to pay digitally. These currencies are secure, and they don't rely on traditional banks. This can lower costs and increase access to financial services.

The growth of digital transactions is also supported by better technology. Faster internet speeds and improved security measures make it easier and safer for everyone to use digital payments. As more people and businesses adopt these methods, digital transactions are set to become the norm.

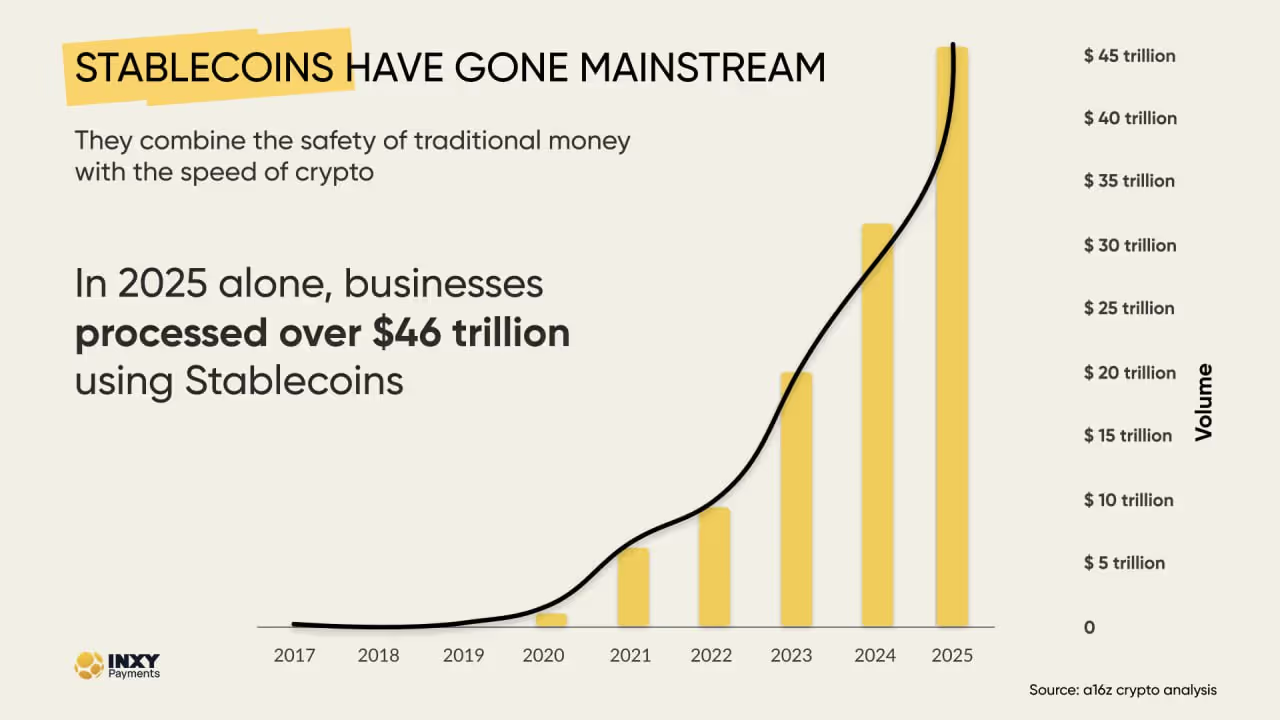

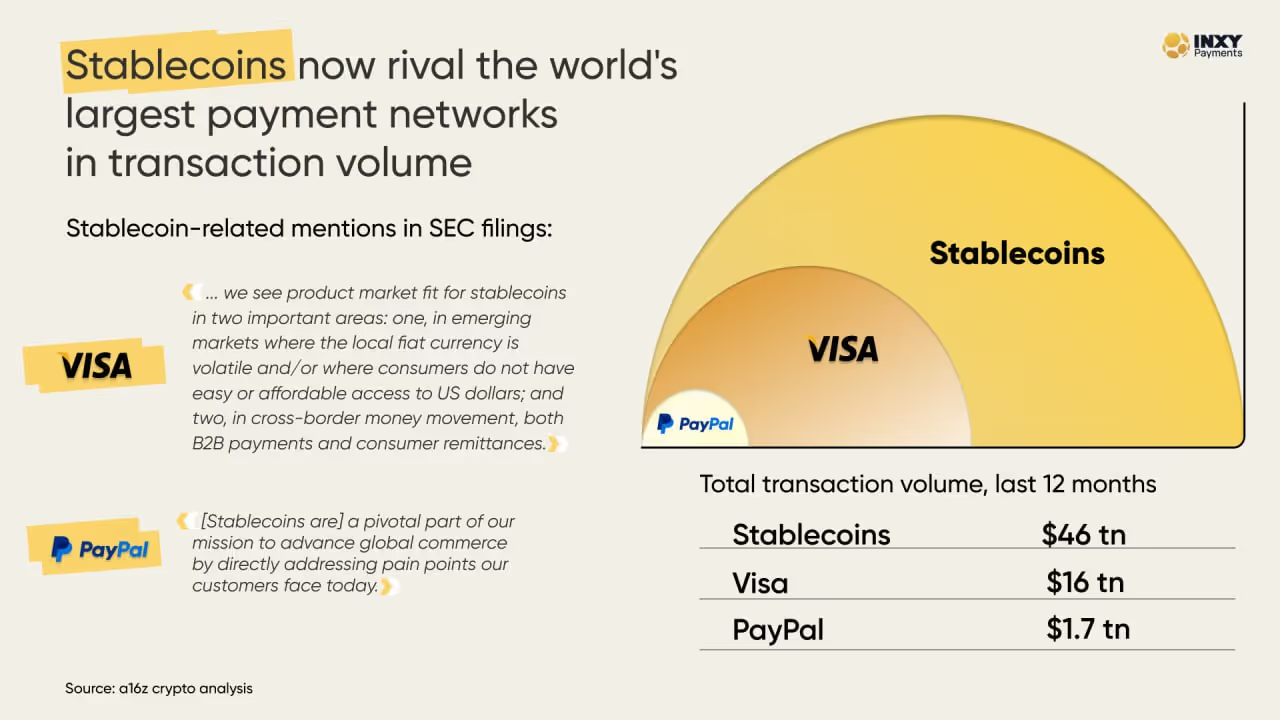

Today, more than 824 million people worldwide own cryptocurrency.

Stablecoins alone processed over $46 trillion last year — more than Visa and PayPal combined.

This shows that digital payments are not a niche trend. They are becoming the main way money moves online.

Benefits for Businesses

Stablecoin payments offer several advantages for businesses. They're less volatile than other cryptocurrencies like Bitcoin. Imagine you're a business owner. You want to know the value of your money won't change drastically overnight. Stablecoins, backed by assets like the US dollar, provide that peace of mind.

Transaction fees with stablecoins can be lower than traditional banking systems. This means businesses save money, especially on international transactions. For example, sending money across borders usually involves hefty fees. With stablecoins, these costs can be minimized.

Another perk is the speed. Traditional bank transfers can take days. Stablecoin transactions, on the other hand, can be processed in minutes. This speed is crucial for businesses that need quick access to funds. Plus, the use of stablecoins can open doors to new markets, reaching customers who prefer using digital currencies.

also let businesses reach new markets. Many people in emerging regions cannot use cards or access banks, but they can use digital wallets and stablecoins on their phones. This opens the door to millions of new customers who were previously locked out of traditional online payments.

Challenges of Traditional Payment Methods

When we talk about traditional payment methods, we're often referring to cash, credit cards, and bank transfers. While these methods have been the backbone of commerce for years, they come with their own set of challenges. Let's explore these issues to understand why businesses are looking at alternatives like stablecoin payments.

Traditional payments are slow and costly. Bank transfers and card payments can take days to settle, especially across borders. Fees are also high — from card fees to bank transfer fees to currency conversion charges — cutting into margins and slowing business growth.

Security is another concern. Credit card fraud and data breaches are not uncommon. When customers hand over their card details, there's always a risk of that information being misused. This situation not only affects the customers but can also damage the business's reputation. A single security breach might lead to a loss of customer trust, which takes a long time to rebuild.

Limited access is an issue too. Not everyone has access to credit cards or bank accounts. Some customers might prefer alternative payment methods like digital wallets or cryptocurrencies. Businesses that only accept traditional payments could miss out on potential sales from these customers. It's like having a store but keeping the door locked for some shoppers.

Traditional payments also lack transparency. It's often hard for both businesses and customers to track where the money is at any given moment. For example, if a payment is delayed, it can be challenging to pinpoint the reason or the stage at which it's stuck. This lack of visibility can cause frustration and distrust among customers.

Lastly, there's the issue of adaptability. As technology evolves, businesses need payment systems that can keep up with the changes. Traditional payment methods are often slow to adapt to new needs and innovations. For instance, they might struggle to integrate with new e-commerce platforms or to support emerging payment trends.

These challenges make it clear why businesses are exploring other options. Stablecoin payments offer solutions to some of these issues, providing a faster, more secure, and cost-effective alternative. As businesses continue to grow and change, finding flexible payment solutions becomes even more critical.

Case Studies: Companies Making the Switch

Let's dive into some real-world examples of businesses that have embraced stablecoin payments. Each company has its unique reasons, and their experiences offer valuable insights for others considering this path.

One notable case is a well-known online retailer. This company decided to accept USDC, DAI and USDT as part of their payment options. The primary motivation was the global reach of crypto. Customers from different countries found it easier to pay in stablecoins without worrying about currency conversion issues. It also allowed the retailer to reduce transaction fees, which were a burden when using traditional payment gateways.

Another interesting example is a tech startup focused on software development. They started accepting stablecoin payments for their services. The team found that using a crypto payment gateway streamlined their operations. It provided faster transaction times and reduced paperwork. The transparency of blockchain technology also appealed to their tech-savvy customers, who appreciated the added layer of security.

A third case involves a popular restaurant chain. The chain began to accept stablecoin payments during the pandemic. Traditional cash payments were less desirable due to health concerns. By adopting stablecoins, they not only offered a contactless payment solution but also attracted a younger clientele. Many of these customers were already familiar with crypto and eager to use it in everyday transactions.

Then there's a logistics company that made the switch. This company operates internationally, and stablecoins helped them manage cross-border payments more efficiently. The predictability of stablecoin values, unlike volatile cryptocurrencies, made financial planning easier. They could handle transactions with partners and vendors with greater confidence in cost predictability.

Lastly, a freelance platform adopted stablecoin payments to simplify payouts to freelancers around the globe. Freelancers appreciated receiving payments in USDC or USDT for their stability and ease of conversion to local currencies. This shift also solved issues related to delayed payments through traditional banking systems.

These examples illustrate the diverse motivations behind the switch to stablecoin payments. From reducing costs to improving speed and security, businesses find multiple benefits in adopting this modern approach. Each company's journey showcases how stablecoin payments can address specific challenges and open up new opportunities.

These stories reflect a broader trend. In 2024 and 2025, stablecoins became one of the fastest-growing payment methods worldwide, especially for online services and global businesses.

Regulatory Landscape in 2025

Stablecoin payments have been gaining traction, and 2025 is shaping up to be a pivotal year for their regulation. Governments around the world are crafting policies to manage these digital currencies. This is crucial as stablecoins like USDC and USDT become more popular in the business world.

One major development is the introduction of global standards. International bodies are working to create a unified framework for stablecoin regulation. This helps ensure that businesses using stablecoins can operate smoothly across borders. Without such standards, companies might face different rules in each country, making international trade complex.

Local governments are also busy. Each country is trying to balance innovation with security. They want to encourage the use of stablecoins while making sure that financial systems remain safe. For example, some countries are adopting stricter compliance measures. This means businesses need to ensure all transactions are transparent and traceable.

In the European Union, new laws are being drafted. These laws aim to protect consumers and prevent illegal activities. They require that stablecoin providers hold sufficient reserves. This ensures that the value of the stablecoins remains stable and reliable.

Meanwhile, in the United States, regulators are focusing on oversight. They want to ensure that stablecoin issuers are transparent about their operations. This includes regular audits and public disclosures. Such measures help build trust among users and businesses.

Asia is also seeing changes. Countries like Japan and Singapore are leading in creating crypto-friendly regulations. They are developing policies that encourage innovation while ensuring that user rights are protected.

These regulatory changes are significant for businesses. Companies need to stay informed and adapt to these new rules. Understanding the regulatory landscape is key to leveraging stablecoin payments effectively. As 2025 unfolds, businesses will need to navigate this evolving landscape carefully.

The Future of Payments: What’s Next?

Stablecoin payments are gaining popularity, and it's not hard to see why. They bring a fresh wave of possibilities to the table. Businesses are starting to notice how stablecoins can change the payment landscape. Let's explore what the future might hold.

One big reason stablecoins are appealing is their stability. Unlike other cryptocurrencies, stablecoins are tied to real-world assets like the US dollar. This means they don't bounce around in value as much. For businesses, this stability is a huge plus. They can accept payments without worrying about losing money due to market fluctuations.

Stablecoins also make international payments easier. In the past, sending money across borders was slow and costly. With stablecoins, transactions can be completed quickly and with lower fees. This is great news for companies working with international clients or suppliers. It allows them to save both time and money.

Security is another reason businesses are interested in stablecoins. Traditional payment systems can be vulnerable to fraud and hacking. Stablecoins offer a more secure option as transactions are recorded on a blockchain. This technology makes it difficult for unauthorized changes to occur.

Looking ahead, we might see stablecoins being used in more everyday transactions. Imagine buying a coffee or paying rent with stablecoins. As more businesses and consumers become comfortable with the technology, this could become a reality.

Stablecoins may also impact how we save and invest money. People are starting to explore options like earning interest on their stablecoin holdings. This could lead to new financial products and services emerging in the market.

In the coming years, regulations will play a crucial role in shaping the stablecoin landscape. Governments and financial institutions will likely establish rules to ensure safe and fair use. These regulations could boost trust and encourage more businesses to adopt stablecoin payments.

The future of payments is changing, and stablecoins are at the forefront. As technology continues to evolve, we can expect even more innovative uses for stablecoins. They have the potential to simplify and enhance the way we handle money.

Supported Stablecoins & Blockchains (2025)

Many stablecoins run on different blockchains. This makes payments fast and affordable anywhere in the world.

Supported stablecoins:

USDT — ERC20, TRC20, BEP20, Polygon

USDC — ERC20, TRC20, BEP20, Polygon

DAI — ERC20, BEP20, Polygon

Other popular coins: BTC · ETH · BNB · LTC · DOGE · TRX · MATIC

Supported blockchains: Bitcoin · Ethereum · Tron · Polygon · Binance Smart Chain · Litecoin · Ton · and others. The mix of currencies and blockchains makes stablecoin payments work for almost anyone, even in places where card payments fail.

FAQ

What are stablecoin payments and how do they work?

Stablecoin payments involve using digital currencies designed to minimize price volatility by pegging their value to a stable asset, like a fiat currency or commodity. They work like any other digital payment method but offer the added benefit of price stability, making them more reliable for transactions.

Why are stablecoins becoming popular in digital transactions?

Stablecoins are gaining popularity in digital transactions due to their ability to offer the benefits of cryptocurrencies, such as decentralization and transparency, while avoiding the price volatility associated with traditional cryptocurrencies. This makes them an attractive option for businesses looking for secure and stable payment methods.

What benefits do stablecoin payments offer to businesses?

Stablecoin payments provide several benefits, including lower transaction fees compared to traditional payment methods, faster processing times as transactions are often completed in seconds, and enhanced security due to blockchain technology, which reduces fraud and chargebacks.

What challenges do traditional payment methods face that stablecoins address?

Traditional payment methods often suffer from high transaction fees, lengthy processing times, and issues with cross-border payments. Stablecoins address these challenges by offering reduced fees, instantaneous transactions, and seamless international payments, thus providing a more efficient alternative.

Can you provide examples of businesses that have switched to stablecoin payments?

Many companies across various industries have transitioned to stablecoin payments. For instance, a tech company might use stablecoins to streamline international payroll, while an online retailer could adopt them to reduce transaction costs and improve payment processing speed.

How is the regulatory landscape for stablecoins evolving in 2025?

In 2025, the regulatory landscape for stablecoins is evolving to provide clearer guidelines and protections for businesses and consumers. Governments and financial bodies are working on frameworks to ensure stablecoin security and transparency, influencing business decisions towards stablecoin adoption.

In the European Union, the new MiCA framework brings clear rules for stablecoins and crypto service providers. These rules aim to protect users while supporting innovation. Similar frameworks are emerging in Asia, the U.S., and Latin America.

What does the future hold for stablecoin payments and their impact on the economy?

The future of stablecoin payments looks promising, with potential for widespread adoption as more businesses recognize their benefits. This could lead to significant changes in the payment industry, driving innovation and possibly reshaping economic structures by making transactions more efficient and accessible worldwide.

.avif)