1 July 2026. Today marks the beginning of a new chapter for Europe's digital asset industry. The transitional period under the EU's Markets in Crypto-Assets Regulation (MiCA) has ended, and the standard for operating a crypto business in Europe has been raised for good.

For years, much of the industry was built around a single jurisdiction. One license. One operating model. That worked while the rules were still evolving. It works less well now.

We want to be transparent with our clients about where INXY stands and what we did about it. INXY did not obtain a MiCA authorization in Poland. So rather than depend on any single jurisdiction, we moved to a multi-jurisdiction operating model — and before 1 July, we completed the migration of every client off our Polish entity. No payments paused. No settlement stopped.

Here's what MiCA is, what changed on 1 July, and how our model is built to keep your payments running through moments exactly like this one.

What is MiCA?

MiCA (Markets in Crypto-Assets Regulation) is the European Union's comprehensive framework for regulating crypto-assets and the companies that provide crypto services. It replaces a patchwork of national rules with a single, harmonized rulebook across all 27 member states.

In practice, MiCA does three main things:

Licenses providers. Any company offering crypto-asset services — custody, exchange, transfers, payouts — must be authorized as a Crypto-Asset Service Provider (CASP) by a national regulator. A CASP license can then be "passported" across the EU.

Regulates stablecoins. Issuers of stablecoins ("e-money tokens") must be authorized and hold strict, fully-backed reserves. This is why compliant stablecoins like USDC and EURC stayed available on EU-regulated venues while non-authorized ones were delisted. (More on this in "Is USDC regulated?")

Sets conduct and transparency standards for how services are marketed and delivered.

MiCA's rules for service providers began applying on 30 December 2024, with a transitional window for existing firms.

What changed on 1 July 2026

MiCA included a transitional ("grandfathering") period under Article 143. Firms already operating legally under national regimes before 30 December 2024 could continue serving clients — but only until they obtained a CASP license or until 1 July 2026, whichever came first. That date has now passed, and there is no extension mechanism in the regulation.

From today, any provider serving EU clients must hold a MiCA CASP authorization. A legacy national registration no longer provides cover.

The situation in Poland made this especially clear. Poland has not yet enacted the national Crypto-Asset Market Act needed for its regulator (KNF) to issue CASP licenses — the act has been vetoed repeatedly, most recently in June 2026. In practice, that left Polish-registered providers with no domestic path to a CASP license before the deadline.

The limits of a single-jurisdiction model

MiCA is not simply making it harder to launch a crypto business. It is redefining what it means to run one: no longer just "get a license and go," but "operate reliably inside a regulated financial system."

That shift began well before 1 July. Across the market, some companies are spending the coming months restructuring. Some are migrating clients. Some are rethinking how they serve Europe altogether. The common thread is that betting an entire operation on one jurisdiction has become a single point of failure.

INXY's response: a multi-jurisdiction operating model

For payment infrastructure providers, continuity is not optional. Payments cannot pause because the regulatory landscape changes. Businesses still need to settle funds. Cross-border commerce continues every day. Infrastructure should adapt so that businesses don't have to.

That is why INXY expanded beyond a single jurisdiction and built a multi-jurisdiction operating model, spanning:

Canada — registered Money Services Business (FINTRAC MSB M23375535)

El Salvador

Cyprus

Switzerland

We did not build this because a deadline forced our hand at the last minute. We built it because our B2B clients need reliability that does not depend on the regulatory status of any one country. When the Polish route closed, that model is what let us complete the migration of all clients off our Polish entity before 1 July 2026 — with no interruption to payouts, settlement, or reporting.

What this means for you

Your service continues. Clients were migrated ahead of the deadline and are served through our appropriately licensed entities. There is no gap in payouts or settlement.

Your funds and reporting are unaffected. Fiat-denominated reporting, payout records, and reconciliation continue exactly as before.

Your compliance standards are unchanged. Full KYB, KYC where needed, real-time transaction monitoring (KYT), and sanctions screening remain in force across every jurisdiction we operate in.

Regulation is becoming the foundation, not the obstacle

One conclusion runs through all of this: regulation is no longer just about compliance. It is becoming the foundation that enables institutional adoption of stablecoin infrastructure at scale. The businesses that treat regulatory resilience as core infrastructure — not paperwork — are the ones that will serve the next phase of the market.

That's the central theme of our latest research, Stablecoins 2026: The New Global Financial Settlement Layer, which maps the regulatory landscape and what it means for businesses building on stablecoin rails. (Link / request the report: [add URL].)

Frequently asked questions

Did INXY obtain a MiCA license? No. INXY did not obtain a MiCA authorization in Poland. Instead of relying on a single jurisdiction, we operate a multi-jurisdiction model across Canada, El Salvador, Cyprus, and Switzerland, chosen to give our B2B clients continuity.

What happened to clients on the Polish entity? All clients were migrated off our Polish entity before 1 July 2026. The migration was completed ahead of the MiCA transitional deadline, with no interruption to payments.

What is MiCA, in simple terms? MiCA is the EU's single set of rules for crypto companies and crypto-assets. It requires service providers to be licensed as CASPs and sets strict standards for stablecoins, consumer protection, and transparency across all member states.

What happened on 1 July 2026? MiCA's transitional period ended. From this date, providers serving EU clients must hold a MiCA CASP license; legacy national registrations no longer provide cover.

Will my payments pause? No. Continuity was the entire point of moving to a multi-jurisdiction model. Client migration was completed before the deadline, and settlement continues without interruption.

Talk to us

Regulatory change raises real questions for any business that moves money across borders. If you'd like to understand how our multi-jurisdiction model supports your payouts, contact our team — and we'd be glad to share our perspective as the industry enters this new phase.

This update is provided for information and does not constitute legal advice. Regulatory details are accurate as of 1 July 2026 and may evolve.

What Are Web3 Payments? Blockchain & Smart Contracts Explained

“Web3 payments” describe a new way to move money in which value travels directly across a blockchain network instead of through banks and card schemes. Unlike traditional online transactions, blockchain payments settle peer-to-peer on a public ledger, are verifiable by anyone, and can run without a central intermediary holding the funds. For businesses, this means faster settlement, lower cross-border costs, and programmable money that can enforce its own rules.

“Web3 payments” describe a new way to move money in which value travels directly across a blockchain network instead of through banks and card schemes. Unlike traditional online transactions, blockchain payments settle peer-to-peer on a public ledger, are verifiable by anyone, and can run without a central intermediary holding the funds. For businesses, this means faster settlement, lower cross-border costs, and programmable money that can enforce its own rules.

This guide explains what web3 payments are, how they work under the hood, where smart contracts fit in, and how they compare to the crypto checkout flows most merchants already know. It is written for founders, finance teams, and product managers evaluating whether on-chain rails belong in their stack.

What Are Web3 Payments?

Web3 payments are transactions executed on decentralized blockchain networks, where ownership of funds is tied to a cryptographic wallet rather than a bank account. The term “web3” refers to the third era of the internet — one built on open, user-owned protocols. In a payment context, web3 crypto payments let a payer send value (typically stablecoins such as USDC or USDT, or assets like ETH and BTC) straight to a recipient’s wallet, with the network itself confirming and recording the transfer.

Three properties separate web3 payments from conventional digital payments:

Self-custody. The payer controls the funds via private keys until the moment of transfer — there is no card issuer or bank acting as gatekeeper.

On-chain settlement. The transaction is final once confirmed by the network, usually in seconds to minutes, with no multi-day clearing cycle.

Programmability. Logic can be attached to the payment itself, so funds release only when predefined conditions are met.

The market context matters. According to recent industry analysis, fiat-backed stablecoins surpassed $300 billion in market capitalization in late 2025, with annualized on-chain settlement volumes in the mid-$20-trillion range — evidence that web3 rails are moving from experiment to real economic activity.

It helps to see where web3 payments sit relative to terms you already use. “Crypto payments” is the umbrella term for paying with digital assets at all. “Web3 payments” is the subset that runs on open, permissionless networks with user-held funds — as opposed to a closed processor that simply accepts coins and settles them to your bank. That difference in architecture is what unlocks the speed, reach, and automation covered below.

How Web3 Payments Work: Blockchain & Wallets

Blockchain payments rely on three components working together: a wallet that holds the keys, a blockchain network that validates transactions, and (for business use) a gateway that translates the on-chain event into something an accounting system can read. Here is the flow in plain terms.

The role of self-custody wallets

A crypto wallet does not “store” coins; it stores the private keys that prove ownership of a balance recorded on-chain. When a customer pays, their wallet signs the transaction with that key, authorizing the network to move the balance to the merchant’s address. Because the key never leaves the user, there is no card number to steal and no chargeback to reverse — a structural difference from card payments.

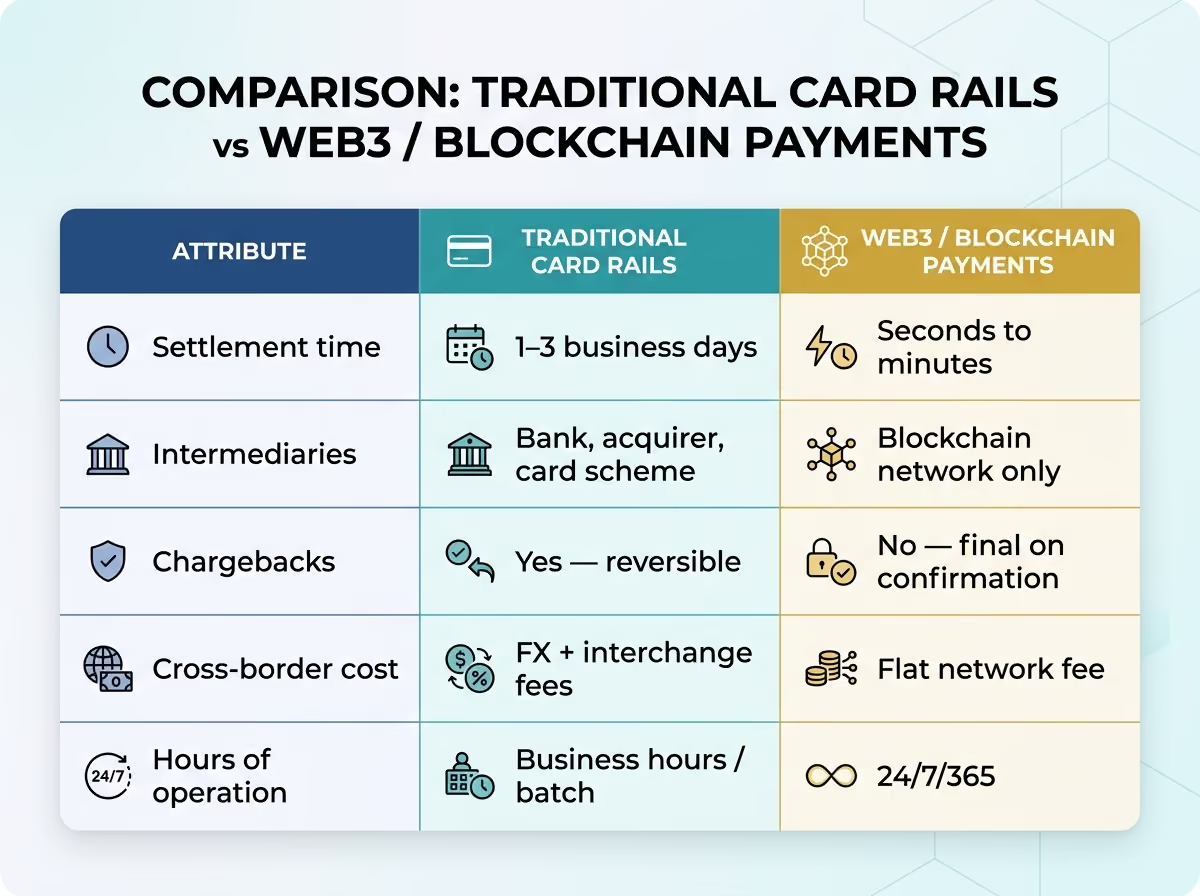

On-chain settlement vs. traditional rails

In a card transaction, authorization, clearing, and settlement happen across several institutions over one to three business days. With blockchain payments, validators confirm the transfer and write it to an immutable ledger in a single step. The table below summarizes the practical differences.

Smart Contract Payments Explained

Smart contract payments are blockchain transactions governed by self-executing code. A smart contract is a program deployed on-chain that automatically performs an action — release funds, split a payment, issue a refund — when its conditions are satisfied. No human has to intervene, and no party can alter the outcome once the contract is live.

Automated & programmable payments

This is where web3 moves beyond simple transfers. A smart contract can hold funds in escrow and release them only when a delivery is confirmed, automatically distribute revenue among several wallets, or stream a salary continuously over time. For businesses, programmable money reduces manual reconciliation and removes the trust gap in multi-party deals.

Consider a marketplace that owes three parties on every sale: the seller, an affiliate, and the platform itself. With cards, that single payment is captured, then split later through separate payout runs and reconciliation. A smart contract executes the split atomically — the moment funds arrive, each wallet receives its share in the same transaction. The same logic powers milestone-based contractor payments, automated refunds, and subscription renewals, all without a card on file or a manual approval step.

Escrow: funds lock until both sides meet their obligations.

Revenue splits: a single incoming payment is divided across partners in one transaction.

Recurring & usage-based billing: subscriptions and metered charges execute on-chain without a card on file.

Tokenized payment solutions

Tokenized payment solutions represent real-world value — a dollar, an invoice, a loyalty credit — as a transferable token on a blockchain. Stablecoins are the most widely used example: a token pegged 1:1 to fiat that combines the stability of a currency with the speed of crypto. Industry research estimates that B2B flows already account for roughly 40% of real-economy stablecoin payments and are growing about 65% per year, which is why tokenized settlement is becoming the default rail for cross-border business payments.

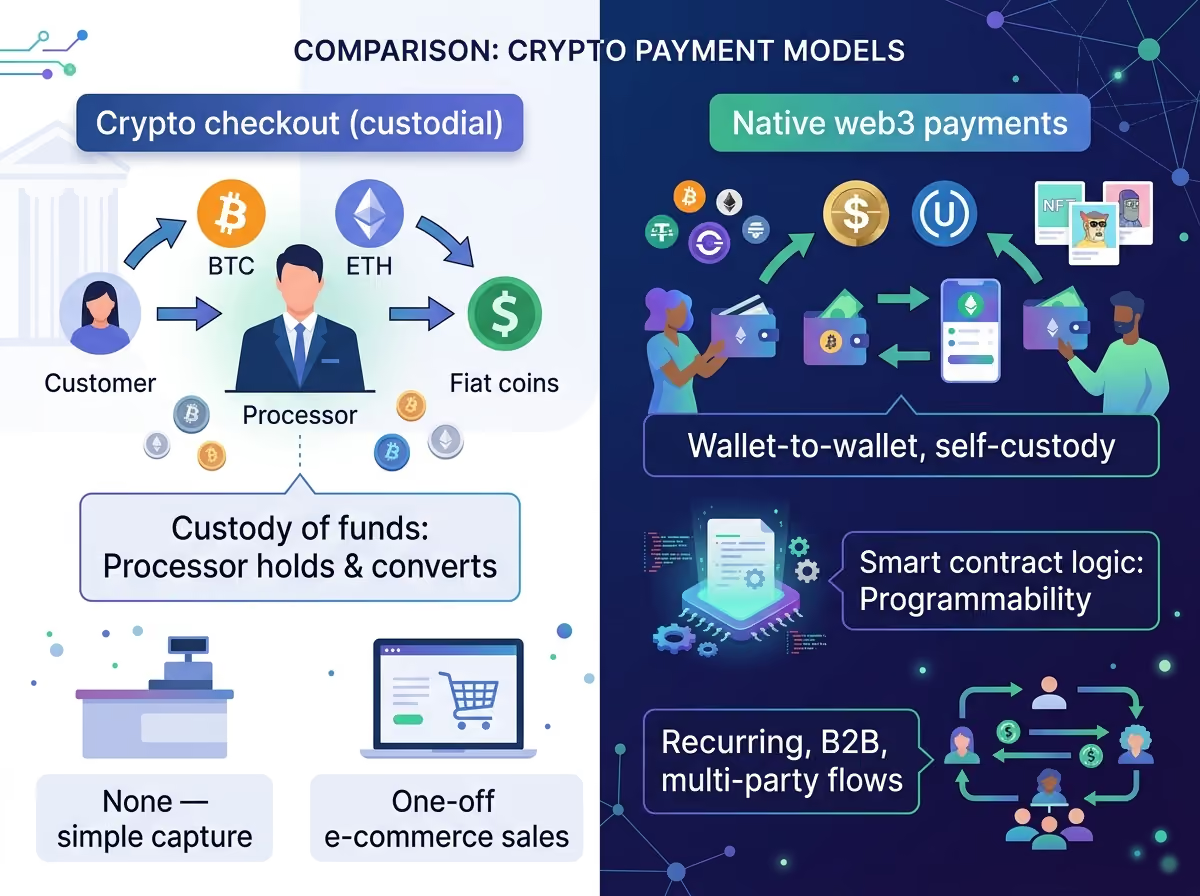

Web3 Payments vs. Traditional Crypto Checkout

Many merchants already “accept crypto” through a hosted checkout that converts coins to fiat. That is a useful on-ramp, but it is not the same as a full web3 payment model. The distinction is about who controls the funds and whether the payment carries logic.

In practice the two coexist. A business might use a custodial checkout for retail customers while using native, programmable rails for supplier payouts and partner settlements. For a deeper breakdown of provider roles, see our guide on the difference between a crypto payment gateway and a processor.

Benefits & Risks for Businesses

Web3 payments — and the broader category of blockchain smart contracts for business — offer clear operational upside, but they come with trade-offs that finance and compliance teams should weigh.

Key benefits:

Near-instant, 24/7 settlement that frees up working capital.

Lower cross-border fees by removing correspondent-banking layers.

No chargebacks, reducing fraud exposure for digital goods.

Automation of escrow, splits, and recurring billing through smart contracts.

Risks to manage:

Price volatility on non-stablecoin assets — most businesses settle in stablecoins to neutralize this.

Irreversibility means errors and misdirected payments are hard to recover.

Regulatory obligations: under frameworks like the EU’s MiCA, you must work with a licensed VASP/CASP and apply KYC/AML and Travel Rule checks.

Smart-contract risk: poorly audited code can be exploited, so use vetted, audited contracts.

For most companies the practical answer is not to choose between safety and innovation, but to adopt web3 payments through a partner that has already solved custody, compliance, and key management. That keeps the operational benefits — speed, automation, global reach — while shifting the hardest security and regulatory work to infrastructure built for it.

How to Start Accepting Web3 Payments

You do not need to build blockchain infrastructure in-house. A compliant gateway abstracts the wallet, network, and conversion layers so you can accept on-chain payments with a standard integration. A practical path:

Choose your settlement asset. Stablecoins (USDC, USDT, DAI) are the standard for business to avoid volatility.

Select a regulated provider. Confirm licensing, multi-chain support, and KYC/AML coverage for your regions.

Integrate via API or plugin. Add the checkout or payout flow and connect webhooks to your back office.

Decide what to automate. Map which payments — escrow, splits, recurring — benefit from smart-contract logic.

INXY provides a regulated, EU-compliant gateway for exactly this. Explore the web3 payments solution and our smart-contract payment infrastructure, or read how to accept crypto payments in 2026 for the full setup walkthrough.

FAQ

What are web3 payments in simple terms? They are payments sent directly between crypto wallets over a blockchain, without a bank or card network in the middle. The network verifies and records the transfer.

Are web3 payments safe? The underlying blockchain settlement is highly secure and tamper-resistant. The main risks are user error, asset volatility, and smart-contract bugs — all manageable by using stablecoins, audited contracts, and a regulated gateway.

What is a smart contract payment? A payment controlled by on-chain code that executes automatically when set conditions are met — for example, releasing escrowed funds once delivery is confirmed.

How are web3 payments different from accepting Bitcoin at checkout? A standard crypto checkout is custodial and converts coins to fiat. Native web3 payments keep funds in self-custody and can carry programmable logic, making them better suited to recurring, B2B, and multi-party flows.

Cryptocurrency is a type of digital or virtual currency. It uses cryptography to secure transactions. This makes it hard to counterfeit. Unlike traditional money, cryptocurrencies operate on a technology called blockchain. This is a decentralized system spread across many computers.

Bitcoin was the first and is the most well-known cryptocurrency. But now, there are thousands of different cryptocurrencies. Each has its own unique features. For example, some are used for fast, low-cost transactions. Others focus on privacy.

A popular feature of cryptocurrencies is their ability to be traded or exchanged easily. People can buy, sell, or trade them on different online platforms. These platforms are called exchanges. Some well-known exchanges are Binance and Coinbase.

Stablecoins are another type of cryptocurrency. They are designed to minimize price fluctuations. They achieve this by being pegged to stable assets like the US dollar. USDT and USDC are examples of stablecoins. They provide stability in the volatile crypto market.

Cryptocurrencies are stored in digital wallets. These can be online, offline, or even hardware devices. Each wallet has a unique address. This address is used to send and receive cryptocurrencies.

While cryptocurrencies offer many benefits, they also come with risks. Their prices can be very volatile. This means they can change quickly and unpredictably. Security is another concern. If a wallet is hacked, it can lead to loss of funds.

Understanding how cryptocurrencies work is important. It helps in making informed decisions. Whether you want to invest or accept crypto payments, knowing the basics is the first step.

Setting Up Your Digital Wallet

Setting up a digital wallet for accepting crypto is like opening a new bank account, but much simpler. First, choose a wallet that suits your needs—whether it's a software wallet for easy access on your phone or a hardware wallet for extra security. Software wallets are apps you can download, making them convenient for daily transactions. Hardware wallets, on the other hand, are devices you connect to your computer, keeping your crypto offline and safe from hackers.

Next, install your chosen wallet and follow the instructions to create an account. You'll be given a unique address, like your wallet's phone number, where people can send you cryptocurrency. It’s crucial to secure your wallet with a strong password and, if possible, enable two-factor authentication for added security. Keep your recovery phrase safe; it’s your lifeline if you forget your password.

Finally, explore the wallet's features. Some wallets let you exchange one cryptocurrency for another directly within the app, while others offer detailed transaction history. Getting familiar with these options ensures smooth management of your crypto payments.

Choosing the Right Payment Processor

Picking the best payment processor for accepting crypto can feel like choosing the right car. You want something reliable, fast, and easy to handle.

In 2026, the most important thing to check is stablecoin support, not just Bitcoin. Most companies now prefer USDT, USDC, or DAI, because they offer price stability and dominate real business payments. Stablecoins now power most B2B payment growth worldwide.

Next, look at fees. Some processors charge a flat rate, others a percentage, and some add hidden spreads when converting crypto to fiat. It’s like buying a concert ticket—sometimes the “service fee” costs more than the seat.

A modern processor should integrate smoothly into your existing systems—your checkout page, invoicing software, or backend platform. Ideally, it should support both plugins (Shopify, WooCommerce) and API integration so your business can scale later.

Security matters too. Look for processors that:

screen every transaction (KYT)

support strong encryptio

offer clear, audit-friendly reporting

This is especially important as more countries enforce stricter crypto regulations, especially in the EU under MiCA.

Integrating Crypto Payments into Your Business

Integrating crypto payments into your business is easier today than ever before. Most companies start by choosing a crypto payment gateway that works alongside their existing checkout or invoicing system. These gateways support major cryptocurrencies like Bitcoin, Ethereum, and stablecoins such as USDT and USDC.

Once you choose a provider, you connect it to your website or platform. Many services offer simple plugins for Shopify, WooCommerce, and other tools. If you prefer something custom, you can use their API to build your own flow.

One helpful feature offered by most payment gateways is automatic conversion. This means that when a customer pays in crypto, the gateway can instantly convert it into stablecoins or fiat currency. Your balance stays steady, which makes bookkeeping easier and avoids the need to monitor crypto price changes. You simply receive the amount in the currency you prefer.

It also helps to clearly show on your website that you accept crypto. Customers who use digital assets often look for businesses that support their preferred payment methods.

As with any payment method, security matters. Keep your accounts protected with two-factor authentication and make sure your systems are up to date. A good gateway will also include its own safeguards, such as blockchain monitoring and fraud checks.

Offering crypto payments is a simple way to expand your payment options, make checkout more flexible, and reach customers in more parts of the world.

Tax Implications and Legal Considerations

When you begin accepting crypto payments, it’s important to understand how taxes and regulations apply in your region. Rules vary from country to country, but most treat cryptocurrency as an asset or a form of taxable income. If your business receives crypto as payment, it may need to be reported to your local tax authority. Keeping clean records of all transactions makes this process easier.

Regulation is also evolving around the world.

European Union

MiCA is now active.

Strict AML and Travel Rule checks.

You must work with a licensed VASP/CASP.

United States

Rules differ by state.

A federal stablecoin law is expected soon.

Choose a partner who follows both federal and state-level compliance.

United Kingdom

New crypto rules expected in 2026.

FCA requires AML, Travel Rule, and Financial Promotions compliance from providers.

Singapore

Very clear regulation under the Payment Services Act.

You must work only with licensed Digital Payment Token providers.

Hong Kong

Strong VASP licensing since 2023.

New stablecoin rules start in 2025.

Middle East (UAE, Bahrain)

UAE’s VARA sets strict rules for crypto companies.

Follow AML/CFT and Travel Rule requirements.

Latin America

Rules vary by country.

Brazil and Mexico are building national frameworks.

Work with partners who apply strong AML controls.

Because the landscape changes quickly, many businesses choose crypto payment processors that are already licensed or registered in their operating regions. Working with a regulated partner often simplifies compliance, especially around AML, KYC, and reporting obligations.

It’s also helpful to consult a tax or legal advisor familiar with cryptocurrency. They can guide you on reporting requirements, record-keeping, and any local rules you may need to follow.

Finally, many companies prefer accepting stablecoins like USDT or USDC. These assets are tied to national currencies and are less volatile than traditional cryptocurrencies, which can make accounting and financial planning easier.

Marketing Your Crypto Payment Options

When it comes to accepting crypto, getting the word out is key. Let people know you accept crypto payments. It can attract a new group of customers who prefer using digital currencies. To make this happen, you need a solid marketing plan tailored to this unique payment method.

One way to start is by updating your website and social media profiles. Highlight your new payment option. Create eye-catching banners or badges that say you accept cryptocurrencies like Bitcoin, Ethereum, or stablecoins such as USDT and USDC. This visual cue can grab attention and encourage visitors to explore more.

Consider writing blog posts or articles about the benefits of accepting crypto. These can educate your audience and position you as a forward-thinking business. Explain why crypto payments are secure, fast, and cost-effective. Use simple language to break down complex concepts. This helps even those new to crypto understand its advantages.

Social media is a powerful tool. Use it to announce your new payment methods. Platforms like Twitter, Instagram, and Facebook allow you to reach a wide audience. Create engaging posts with hashtags related to cryptocurrency. These can help your posts appear in searches made by crypto enthusiasts.

Collaborations with crypto influencers can extend your reach. Find influencers who align with your brand. They can showcase your business to their followers, who might be interested in using crypto. A positive mention from a trusted voice can enhance your credibility.

Email marketing can also play a role. Send newsletters to your subscribers informing them about your new payment option. Offer exclusive promotions or discounts for those who choose to pay with crypto. This can motivate them to try out the new payment method.

Hosting events or webinars about cryptocurrency can engage your audience. These can be opportunities to answer questions and demonstrate how paying with crypto works. Educating potential customers can remove doubts and make them more comfortable using digital currencies.

By using these marketing strategies, you can effectively promote your crypto payment options. This can lead to increased customer engagement and potentially boost your sales.

Future Trends in Cryptocurrency Payments

Let's talk about the exciting trends in cryptocurrency payments as we look ahead to 2026. Cryptocurrencies are changing the way we think about money, and it's only going to get more interesting. Businesses and freelancers should keep an eye on these trends to stay ahead of the curve.

One major trend is the rise of stablecoins. These are digital currencies that are tied to real-world assets like the US dollar. Examples include USDT and USDC. They provide the benefits of cryptocurrencies without the wild price swings. This makes them attractive for businesses that want to accept crypto without worrying about losing value overnight. Stablecoins are becoming a popular choice for payments because they offer stability and trust.

Another trend is the growing acceptance of crypto by big companies. More and more large businesses are starting to accept crypto payments. This is because they see the potential of reaching new customers worldwide. When big players jump on board, smaller businesses often follow. This could lead to more widespread use of crypto in everyday transactions.

There's also a push for better technology to support crypto payments. Developers are working on making transactions faster and cheaper. Right now, some cryptocurrencies take too long to process or have high fees. But new technologies, like the Lightning Network, aim to solve these problems. They allow instant transactions with very low fees. This makes crypto more practical for everyday use.

Security is always a concern with cryptocurrencies. As we move forward, we can expect improvements in this area too. Developers are creating more secure wallets and platforms to protect users from scams and hacks. This is crucial for building trust in the system.

Regulations are another important factor. Governments around the world are trying to figure out how to handle cryptocurrencies. In 2026, we might see more clear rules and regulations. This could make it easier for businesses to accept crypto without worrying about legal issues.

Lastly, as more people become familiar with cryptocurrency, we'll likely see an increase in its use. Education is key here. The more people know about how crypto works, the more comfortable they'll feel using it. This could lead to a significant increase in crypto payments.

In summary, the future of cryptocurrency payments looks promising. With stablecoins, big company adoption, better technology, increased security, clear regulations, and greater awareness, businesses and freelancers have much to look forward to in 2026. Keep an eye on these trends to stay ahead in the evolving world of crypto.

FAQ

What is cryptocurrency, and why should I consider accepting it as a payment method?

Cryptocurrency is a digital or virtual form of currency that uses cryptography for security and operates on decentralized networks like blockchain technology. Accepting crypto payments can broaden your customer base, lower transaction fees, and enhance your business's image as forward-thinking and tech-savvy.

How do I choose the right digital wallet for my business?

When selecting a digital wallet, consider factors like security features, compatibility with multiple cryptocurrencies, user interface, and customer support. Look for wallets with strong encryption and backup options to ensure your funds remain secure.

What should I look for in a cryptocurrency payment processor?

Key considerations for choosing a crypto payment processor include transaction fees, supported cryptocurrencies, ease of integration with existing systems, and customer support. Compare different options to find a processor that aligns with your business needs and budget.

How can I integrate cryptocurrency payments into my existing payment systems?

To integrate cryptocurrency payments, you can use plugins or APIs provided by your chosen payment processor. These tools allow you to seamlessly add crypto payment options to your website or point-of-sale systems, offering customers a smooth checkout experience.

What are the tax implications of accepting cryptocurrency payments?

The tax implications can vary based on your location, but generally, cryptocurrencies are treated as property for tax purposes. This means you need to track transactions and report any capital gains or losses. Consult with a tax professional to ensure compliance with local regulations.

How can I effectively market my acceptance of crypto payments?

Promote your crypto payment options through your website, social media, and email marketing. Highlight the benefits, such as lower fees and enhanced security, to attract tech-savvy customers. Collaborating with crypto influencers and participating in blockchain events can also boost visibility.

What future trends should I be aware of in the cryptocurrency payment space?

Stay informed about trends like the rise of decentralized finance (DeFi), the increasing use of stablecoins, and advancements in blockchain technology. These developments could offer new opportunities for reducing costs and enhancing transaction security in the coming years.

How to Verify a Merchant Account? Step-by-Step Guide

Navigating the regulatory landscape of 2026 is crucial for any business accepting digital assets. This guide provides a comprehensive, step-by-step walkthrough of the merchant verification process for crypto payment gateways in the European Union. From understanding the Markets in Crypto-Assets (MiCA) regulation to mastering the Know Your Business (KYB) documentation requirements, we detail exactly how to secure a verified, bank-grade account. Whether you are in e-commerce, hosting, or high-risk industries, this unified framework ensures your business is compliant, secure, and ready for the global economy.

The institutionalization of the digital asset economy within the European Union has reached a definitive stage. As the financial sector navigates the complexities of the mid-2020s, regulatory compliance and operational excellence are no longer optional for businesses seeking to leverage blockchain-based financial rails.

For crypto payment gateways based in the EU, such as INXY Payments, the verification workflow represents the first and most critical touchpoint in establishing a secure, bank-grade relationship with professional partners. This report provides an exhaustive analysis of the merchant verification process, grounded in the primary directives of the Markets in Crypto-Assets (MiCA) Regulation and the practical requirements of the Know Your Business (KYB) standards.

The Regulatory Landscape: MiCA, TFR, and DAC8

The "Regulatory Rubicon" has been crossed, shifting the focus of European authorities from drafting policy to aggressive enforcement. Central to this environment is the Markets in Crypto-Assets Regulation (MiCA), which has successfully harmonized the rules for digital assets across all 27 EU member states.

The verification process is now governed by three key frameworks:

MiCA Authorization: Eliminates the "Wild West" era, ensuring only fully authorized providers operate within the EEA.

Transfer of Funds Regulation (TFR): Enforces a "Zero Threshold" policy for the "Travel Rule," requiring detailed data on the originator and beneficiary for every transaction.

DAC8: Mandates strict tax reporting and the collection of Tax Identification Numbers (TINs) to ensure fiscal transparency.

Architecture of the Know Your Business (KYB) Process

Know Your Business (KYB) is the primary defensive mechanism used by fintech gateways. Unlike Know Your Customer (KYC), which focuses on individuals, KYB requires a deeper exploration of corporate hierarchies.

The Verification Objectives:

Legal Existence: Proving the business is a real, registered entity.

Control Disclosure: Identifying the Ultimate Beneficial Owners (UBOs) to prevent the use of shell companies for illicit activities.

Risk Scoring: Evaluating the industry, geography, and transaction profile of the merchant.

The INXY Payments Verification Workflow: A Step-by-Step Guide

The verification process is designed to be rigorous yet streamlined, ensuring all participants meet EU compliance standards. This is a unified process applicable to all merchants, regardless of their industry or integration method.

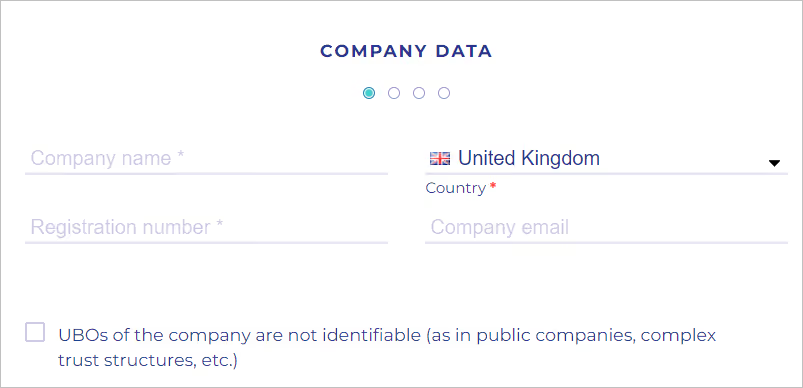

Step 1: Initial Company Data Intake

The process commences with the "Company data form." The merchant must enter fundamental identifying information, including the legal Company Name, official Registration Number, and Country of Registration.

Note: Providing a direct company email is recommended to ensure a clear line of communication with compliance officers.

Step 2: Comprehensive Documentation Upload

Merchants must validate their legal status by uploading a robust evidentiary file. Mandatory documents typically include:

Certificate of Incorporation / Business Registration: Proof that the entity exists in a government registry.

Articles of Association (AOA): Defines the entity's operations and leadership structure.

Operating License: Required only if the merchant operates in a specifically regulated sector (e.g., gambling, forex).

Identifying the natural persons who ultimately control the entity is the cornerstone of EU AML regulations.

The 25% Rule: Merchants must identify any natural person holding more than 25% of ownership shares or voting rights.

Verification: For each UBO, the system requires their full name, date of birth, and contact details. Identity verification can be performed live or via a secure link sent to the stakeholder.

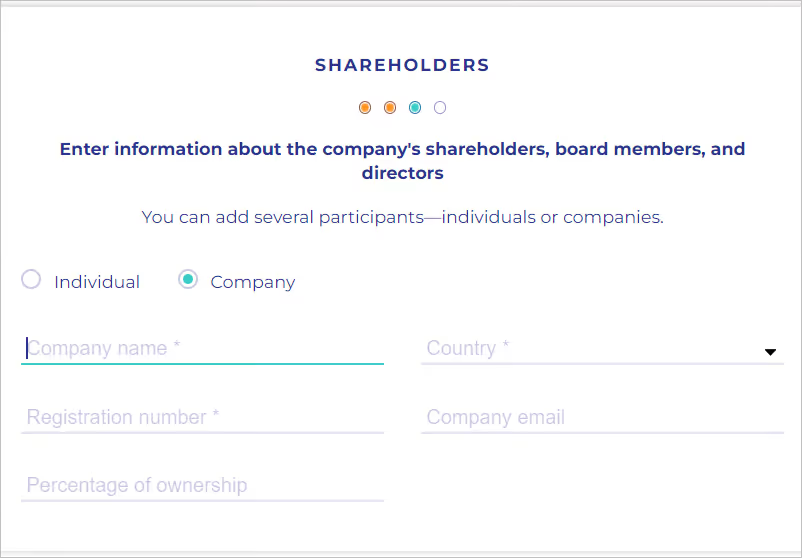

Step 4: Shareholder and Representative Verification

Corporate Shareholders: If a shareholder is another company, the merchant must provide that entity's Articles of Association and trace the ownership chain back to a natural person.

Legal Representative: Data must be provided for the person acting on behalf of the company, ensuring they have the legal authority (e.g., Director status or Power of Attorney) to open financial accounts.

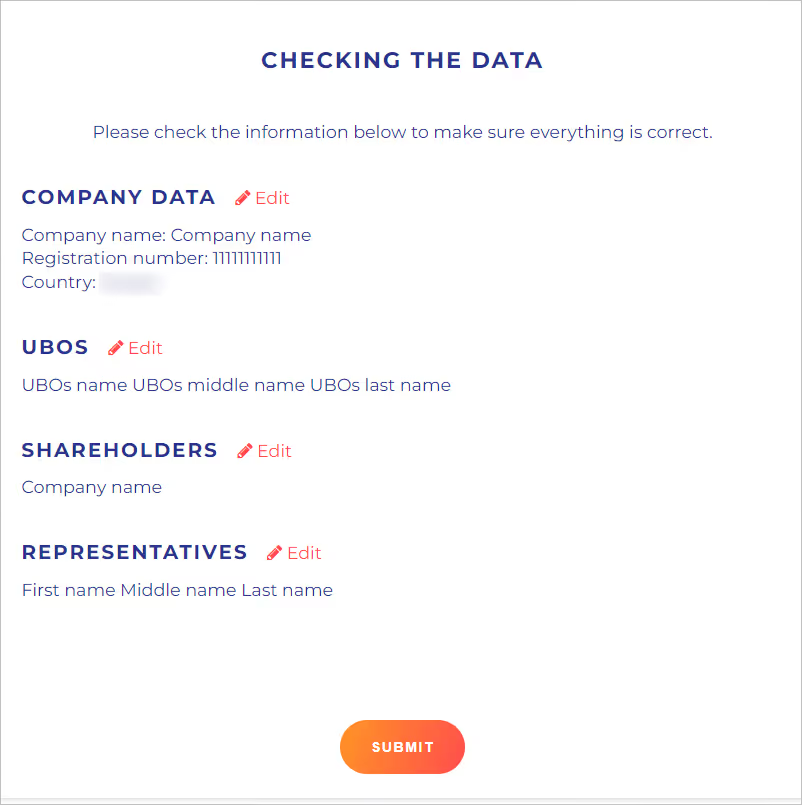

Step 5: Final Validation and Submission

The penultimate step is a thorough review of all provided data. Once confirmed, the application enters the compliance review queue. Thanks to automated systems, merchants can track their status in real-time via their dashboard.

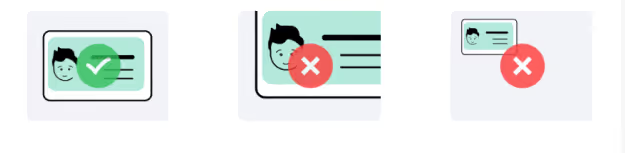

Document Requirements and Authentication Standards

The integrity of the verification process relies entirely on the quality of the documentation. The European fintech environment maintains a high bar for validity.

Mandatory Conditions for Approval:

Language: All documents must be in English. If the original is in another language, a notarized translation is required.

Authentication: Documents must be "official," bearing the necessary stamps, signatures, or qualified electronic seals as per local laws.

Recency: Extracts from commercial registries generally should not be older than 3 months to ensure the data is current.

Common Reasons for Rejection:

Typos: Mismatches between the input form and the uploaded PDF.

Missing Pages: Uploading incomplete Articles of Association.

Low Quality: Blurry scans or photos where text is illegible.

Security and Data Protection (GDPR & DORA)

The sensitive nature of KYB data requires the highest levels of protection.

GDPR Compliance: Data is used solely for client identification and activity justification, adhering to the principle of "Purpose Limitation."

DORA (Digital Operational Resilience Act): Mandates that payment gateways demonstrate resilience against cyber threats. Data is encrypted at rest and in transit, with role-based access ensuring only authorized compliance personnel can view identity files.

Conclusion: Compliance as a Competitive Advantage

Completing the merchant verification process is more than a regulatory hurdle; it is a strategic move that positions a business as a credible player in the global economy. By adhering to this standardized verification workflow, merchants—whether they are hosting providers, e-commerce stores, or digital service agencies—secure a stable, bank-grade foundation for their financial operations.

In the mature crypto economy of 2026, a verified account is the key to unlocking global markets, ensuring seamless settlements, and protecting business capital from regulatory friction.