USDT is a single asset, but it lives on more than a dozen blockchains — and the network you choose can change the cost of a transfer by 100x or more. For a one-off payment that's a rounding error. For a business sending thousands of payouts a month, picking the wrong chain quietly burns thousands of dollars.

This is a practical breakdown of the cheapest network to send USDT in 2026, what drives the fee on each chain, and how to match the network to the payout.

Why USDT fees vary so much

The fee to move USDT has nothing to do with Tether itself. It's the network's gas fee — paid in the chain's native token — that varies:

On Ethereum (ERC-20) you pay ETH gas, which is priced by network congestion and can spike sharply.

On Tron (TRC-20) you pay in TRX energy/bandwidth, which is low and stable.

On Solana, TON, and BNB Chain, base fees are engineered to be very small.

So "how much does it cost to send USDT" is really "which network did you send it on."

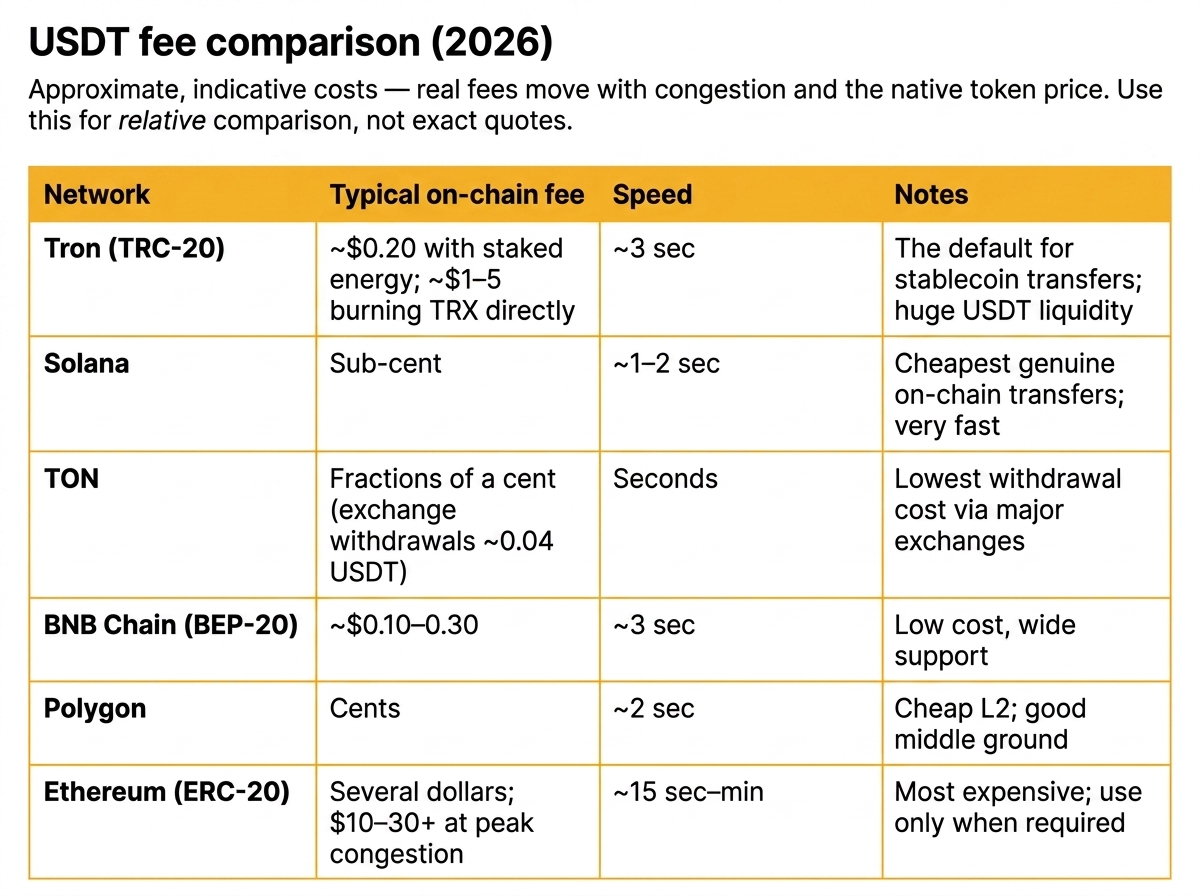

USDT fee comparison (2026)

Approximate, indicative costs — real fees move with congestion and the native token price. Use this for relative comparison, not exact quotes.

The short version: for pure on-chain cost, Solana and TRC-20 lead, with TON unbeatable for exchange withdrawals. ERC-20 is the most expensive and should be reserved for recipients who specifically need it.

Match the network to the payout amount

Cheapest isn't always "correct." The right network depends on the size of the transfer and where the recipient wants the funds.

Micro-payouts (under ~$50): TRC-20, Solana, or TON. Fees would otherwise eat a meaningful slice of the payment.

Standard payouts ($50–$5,000): Solana, Polygon, or TRC-20 keep costs to pennies while settling fast.

Large transfers (over ~$5,000): Cost matters less relative to the amount. ERC-20 is acceptable if the counterparty requires it — the $10–20 fee is small against the principal, and Ethereum's liquidity and integrations are unmatched.

Beyond the headline fee

Fee-per-transfer is the obvious number. Three others matter just as much at scale:

1. Recipient acceptance. The cheapest network is useless if the recipient's wallet or exchange doesn't support it. Always confirm the network before sending — cross-network mistakes are irreversible.

2. Native-token overhead. Every network needs its gas token in your wallet. Running payouts across five chains means monitoring and topping up five different balances — an operational cost that doesn't show up in the per-transfer fee.

3. Failed and stuck transfers. Underpriced gas on congested networks means stuck transactions and support tickets. Reliability has a cost, too.

How platforms cut costs further

When you run payouts through a fiat-native platform instead of manually, network fees stop being your problem in two ways:

Automatic routing. The platform sends each payout on a supported low-fee network without you managing gas on every chain.

No native-token juggling. You fund a balance in EUR or USD; the provider handles conversion and gas. Your reporting stays in fiat.

That removes the hidden operational cost of multi-chain payouts, not just the visible per-transfer fee.

Frequently asked questions

What is the cheapest network to send USDT? For on-chain self-custody transfers, Solana and Tron (TRC-20) are cheapest, and TON offers the lowest withdrawal fees on major exchanges. Ethereum (ERC-20) is the most expensive.

Is TRC-20 always the cheapest for USDT? Not always. TRC-20 is very cheap and has the deepest USDT liquidity, but Solana and TON can be cheaper still per transfer. TRC-20 remains the most widely accepted low-fee option.

Why is sending USDT on Ethereum so expensive? ERC-20 transfers pay ETH gas, priced by network demand. During congestion, a single USDT transfer can exceed $30 in gas.

Does the network affect how much USDT the recipient receives? The network sets the fee you pay to send. Choosing a low-fee chain means more of your budget reaches recipients, especially across many small payouts.

Can I send USDT across networks? An address is tied to one network. To move USDT between chains you need a bridge or an exchange — you can't send TRC-20 USDT directly to an ERC-20 address.

Send on the right network, automatically

If you're running regular USDT payouts, you shouldn't be managing gas tokens across five blockchains. INXY's mass USDT payouts route each transfer over low-fee networks and report everything back in EUR or USD — so you get the cheapest path without the multi-chain overhead. New to bulk sending? Start with our step-by-step USDT payout guide.

The Travel Rule for Crypto Payouts: What B2B Senders Must Know in 2026

The Travel Rule requires sender and recipient identity data to accompany crypto transfers, and in 2026 it directly affects any business paying contractors, suppliers, or partners in crypto. This guide breaks down the regulatory picture by region — the EU's no-threshold TFR, the US $3,000 BSA rule plus new GENIUS Act stablecoin obligations, and FATF's $1,000 baseline — and the exact originator/beneficiary data each payout must carry, including the extra step for self-hosted wallets. It then shows how a regulated crypto gateway runs pre-send screening, KYT/AML checks, and the Travel Rule inside the payout flow, so B2B senders stay compliant without building their own compliance stack.

If your business sends crypto payouts — to contractors, suppliers, affiliates, or partners — the crypto Travel Rule now sits between you and every transfer. It is the single piece of kyc aml crypto payments regulation most likely to delay, freeze, or return a B2B payout in 2026, and most senders only learn about it after a payment is held. This guide explains what the Travel Rule is, how the 2026 rules differ by region, what data must accompany each payout, and how a regulated crypto gateway runs the checks so you don't have to build a compliance stack yourself.

What the crypto Travel Rule is (and why it now applies to your payouts)

The Travel Rule is an anti-money-laundering standard that requires identifying information about the sender (originator) and recipient (beneficiary) to "travel" alongside a transfer of value. It originated in traditional banking and now applies to crypto.

FATF Recommendation 16, extended to crypto

The rule comes from the Financial Action Task Force (FATF), whose Recommendation 16 was extended in 2019 to cover virtual assets. The principle is simple: when a regulated provider moves crypto on a customer's behalf, it must collect, transmit, and retain originator and beneficiary details so that law enforcement can trace funds. FATF recommendations are influential but not law in themselves — each jurisdiction decides how to implement them, which is why the picture is fragmented (more on that below).

Who counts as a VASP — and when you are the originator

The obligation falls on Virtual Asset Service Providers (VASPs): exchanges, custodial wallet providers, and crypto payment gateways. When your business initiates a payout through such a provider, the provider is the "originating institution" and carries the Travel Rule duty — but it can only meet that duty with your data. In practice this means the gateway must know who you are paying and why, and you must be able to supply recipient details on demand. The compliance burden is shared: the provider operates the machinery, but incomplete sender data is the most common reason a payout stalls.

The 2026 regulatory picture: crypto compliance and regulations by region

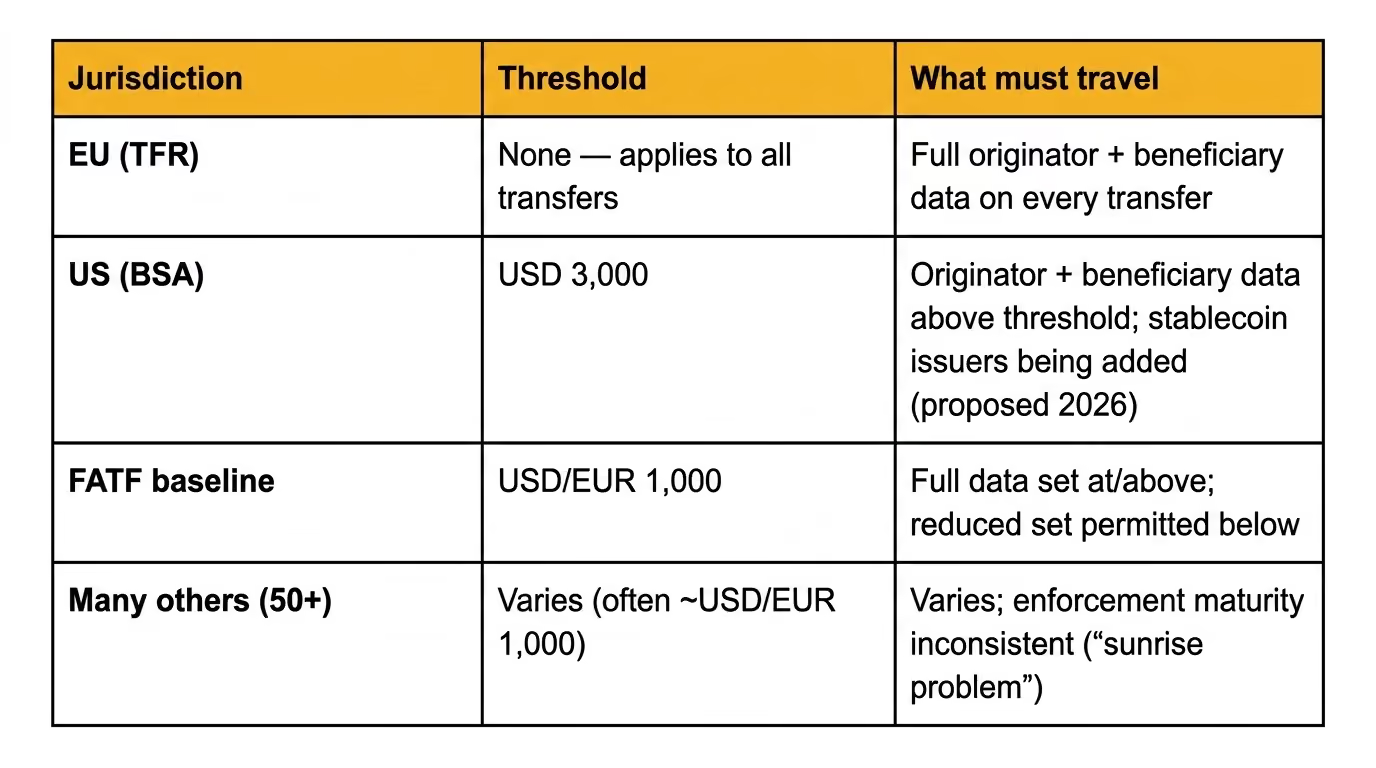

By 2026, over 50 jurisdictions have enacted Travel Rule legislation — roughly 73% of FATF-assessed jurisdictions, up from a far smaller base two years earlier. Enforcement maturity, thresholds, and required data still vary widely, so a payout that is routine in one corridor can be blocked in another.

EU — Transfer of Funds Regulation (TFR), no de-minimis threshold

The EU's recast Transfer of Funds Regulation (TFR) took effect on 30 December 2024. It is the strictest major regime: full originator and beneficiary data must accompany every crypto-asset transfer handled by a regulated provider, with no minimum threshold. A €5 payout and a €500,000 payout carry the same data obligation. The TFR operates alongside MiCA, the EU's broader crypto-asset framework, which governs licensing of providers.

US — Bank Secrecy Act Travel Rule, USD 3,000 threshold

In the United States the Travel Rule lives under the Bank Secrecy Act (BSA), administered by FinCEN, with a threshold of USD 3,000 — notably higher than FATF's recommendation. A 2026 development matters for stablecoin senders: following the GENIUS Act (signed July 2025), the U.S. Treasury proposed a rule on 8 April 2026 treating permitted stablecoin issuers as BSA financial institutions, subject to AML programs, recordkeeping, and the Travel Rule, with compliance expected around April 2027. The direction of travel is clear — stablecoin rails are being pulled fully into the same compliance perimeter as the banking system.

FATF global threshold and the "sunrise problem"

FATF recommends a standard threshold of USD/EUR 1,000, below which a reduced data set may apply. Because jurisdictions adopt the rule at different speeds, the industry faces the "sunrise problem": a compliant provider in a regulated market may need to send Travel Rule data to a counterparty in a market that has not yet implemented the rule and cannot receive it. For B2B senders this means a payout's success can depend on the recipient platform's jurisdiction, not just your own.

What data must "travel" with a B2B crypto payout

The required data set is consistent across regimes, even where thresholds differ.

Required originator (sender) fields

Name of the originator (your business or the paying entity).

Wallet address used for the transfer (or a transaction reference).

Physical/registered address, and in some regimes an official identifier or account number.

Required beneficiary (recipient) fields

Name of the recipient.

Wallet address receiving the funds.

In addition, the transaction amount, execution date, and a unique transaction identifier are recorded with every transfer. For your operations, the practical takeaway is that recipient name + wallet must be accurate and verifiable before you send — a mismatch is a hold.

Self-hosted (unhosted) wallet payouts — the extra step

Paying out to a self-hosted (non-custodial) wallet — common when paying contractors or partners who hold their own keys — changes the mechanics. There is no counterparty VASP to receive the Travel Rule message, so the data isn't transmitted onward; instead, your provider must still collect originator and beneficiary information from you, and above the relevant threshold may require verification of wallet ownership based on a risk assessment. Expect to attest that the recipient controls the destination address for larger payouts.

How a regulated crypto gateway runs the Travel Rule on outbound payouts

This is where a regulated crypto gateway earns its keep. Rather than connecting to Travel Rule messaging protocols, screening providers, and sanctions lists yourself, the gateway runs the controls inside the payout flow. Using INXY's outbound model as a concrete example, an outgoing payout passes through several gates before any transfer is created.

Pre-send checks — address risk and blacklist screening

A payout starts as a withdrawal request, not an immediate send. A pre-send validation stage runs first and can stop the operation with an error so that no transaction is ever formed. As part of this, the recipient address is looked up against historical risk data: a previously unseen address is treated cautiously, while a known address carries its last risk result. This means a problematic payout is caught at draft stage, not after funds have left.

KYT/AML screening of the recipient

Next is the outbound KYT (Know Your Transaction) sequence. The recipient address is checked against a blacklist; a match fails the request outright with no transaction created. If it clears, a risk provider screens the address and returns an outcome:

Low or Medium → the payout draft passes and proceeds.

High → the request fails, no transaction is created, and an error is returned.

This is the kyc aml crypto payments layer working in real time on the money leaving your account.

The Travel Rule message exchange

Only after screening passes does the Travel Rule step run, packaging and exchanging the required originator/beneficiary information with the counterparty provider where one exists. The payout then proceeds to settlement. The sequence matters: screen first, transmit data, then send.

Approved contacts and recipient allow-lists

Gateways typically maintain a contact list of approved recipients. A recipient flagged as declined blocks the payout regardless of other checks — a useful control for finance teams that want a vetted, reusable set of payees for recurring or mass payouts.

KYB is the gate to the platform; KYT is the gate to each transaction; the Travel Rule is the data that rides along with it. A gateway that handles all three is what "secure crypto payments" actually means in operational terms.

Compliance risks of getting payouts wrong

For a B2B sender, Travel Rule failures are not abstract — they hit cash flow and counterparties directly:

Held or returned transfers. Missing or mismatched recipient data is the most common cause of a stalled payout. Funds can sit in review or be returned, delaying contractor and supplier payments.

Counterparty refusal. If the receiving platform can't accept Travel Rule data (the sunrise problem) or flags your transfer, it may bounce the payment.

Regulatory exposure. Operating outbound flows without proper screening and recordkeeping exposes the business to AML penalties — increasingly so as stablecoin issuers are folded into BSA-style obligations.

Operational drag. Building and maintaining screening, sanctions, and Travel Rule messaging in-house is expensive and never "done," because rules and thresholds keep shifting.

How to automate crypto payouts without owning the compliance stack

The practical answer for most B2B senders is to run payouts through a regulated crypto gateway that treats the Travel Rule, KYT, and sanctions screening as part of the payout itself — not as something you bolt on.

With INXY, every outbound payout passes through pre-send validation, blacklist and KYT risk screening, and the Travel Rule step before settlement, and recurring payees can be managed through an approved contact list. Because the same flow is exposed via API and webhooks, you can run mass payouts — paying hundreds of contractors or partners at once — with compliance checks applied per recipient automatically, and receive status events back into your own systems. That is what "how to automate crypto payouts" looks like when compliance is built in rather than improvised.

If compliance posture is your priority, start with INXY's security & compliance capabilities; if payout mechanics are the focus, see crypto payouts and the cross-border and payroll options that build on the same rails.

FAQ

Does the Travel Rule apply to stablecoin payouts? Yes. Stablecoin transfers handled by a regulated provider are subject to the Travel Rule like any other virtual asset. In the EU, full data is required regardless of amount; in the US, stablecoin issuers are being brought explicitly into BSA Travel Rule obligations under a rule proposed in April 2026.

What is the Travel Rule threshold in 2026? It depends on the jurisdiction. FATF recommends USD/EUR 1,000; the US applies USD 3,000 under the BSA; the EU applies no threshold — every transfer carries full data.

Do I need to collect data for self-hosted (unhosted) wallet payouts? Yes. Even though there's no counterparty provider to receive the message, your gateway must still collect originator and beneficiary information, and above the relevant threshold may require proof that the recipient controls the destination wallet.

Is the Travel Rule the same as KYC? No. KYC/KYB verifies identity at onboarding. The Travel Rule governs the transmission of identity data alongside each transfer. They work together but are distinct obligations.

Who is responsible — the sender or the recipient platform? Both sides carry obligations. The originating provider must collect and transmit sender/recipient data; the beneficiary provider must receive and retain it. As the business initiating the payout, you're responsible for supplying accurate recipient information to your provider.

How to Integrate a Crypto Payment API: A Developer’s Guide for 2026

Integrating crypto payments is no longer just about generating a wallet address—it’s about building a robust, scalable financial pipeline. In this 2026 Developer’s Guide, we strip away the complexity of blockchain interactions and provide a clear roadmap for API integration.

How to Integrate a Crypto Payment API: A Developer’s Guide for 2026

In the fast-moving world of fintech, the question is no longer if a business should accept cryptocurrency, but how seamlessly it can be integrated. As we move through 2026, the European market has reached a point of high maturity. With the full enforcement of MiCA (Markets in Crypto-Assets) regulations, crypto payments have transitioned from a niche experiment to a standardized financial tool for EU-based enterprises.

For developers and product managers, integrating a crypto payment API is now as streamlined as traditional fiat gateways, provided you follow the right architectural patterns.

1. Understanding the 2026 Integration Workflow

Modern crypto integration follows a predictable RESTful pattern. Unlike the early days of manual wallet monitoring, today’s gateways handle the blockchain's complexity, allowing your backend to interact with simple JSON payloads.

The standard lifecycle of a crypto payment includes:

Initialization: Your server requests a unique payment address for a specific order.

Monitoring: The gateway monitors the blockchain (Bitcoin, Ethereum, Tron, etc.) for incoming transactions.

Confirmation: The gateway verifies the transaction depth (number of block confirmations).

Webhook Notification: Your system receives an asynchronous callback to update the order status.

2. Step-by-Step API Integration

Phase A: Environment Setup

Before hitting production, high-quality gateways provide a Sandbox environment. This allows you to simulate successful payments, timeouts, and underpayments without risking real capital. You’ll typically need two headers for every request:

X-API-KEY: Your unique identifier.

X-PAY-SIGNATURE: A HMAC-SHA512 hash to ensure data integrity.

Phase B: Creating the Payment

To start a checkout, your backend sends a POST request to the /invoices or /payments endpoint.

The gateway responds with a destination address and a QR code URL. In 2026, the best UX practice is to offer "Invisible Crypto"—where the user sees a familiar interface, and the gateway handles the real-time conversion behind the scenes.

Phase C: Handling the Webhook

This is the most critical part of the integration. Since blockchain transactions are asynchronous, your server must be ready to receive a POST callback.

Pro Tip: Always verify the webhook signature. Never update an order status based solely on the incoming payload without checking that the request actually originated from your provider.

3. Security and Compliance in the EU

In the 2026 fintech landscape, security isn't just about encryption; it's about regulatory alignment. Within the EU, businesses must ensure their payment partner adheres to Transfer of Funds Regulation (TFR) and AML (Anti-Money Laundering) standards.

When choosing a provider, look for features like:

Auto-Conversion: Instantly swapping volatile assets into stablecoins or EUR to protect your margins.

Audit-Ready Reporting: Financial statements that your accounting team can actually use for VAT and tax filings.

This is where specialized gateways like INXY (inxy.io) excel. Built specifically for the EU market, INXY acts as a regulated bridge. It doesn't just provide an API; it provides a compliant infrastructure that allows Web2 companies to scale into Web3 without the headache of managing private keys or worrying about crypto volatility. By integrating a solution like INXY, businesses can reduce processing fees by up to 70% compared to traditional card networks, while benefiting from instant SEPA settlements.

4. Testing and Optimization

Before going live, run "Chaos Tests" on your integration. What happens if a user sends too little? What if they pay after the 20-minute price-lock window? A robust API should provide clear error codes for these scenarios, allowing your frontend to guide the user toward a resolution—such as a partial refund or a top-up payment.

Conclusion

Integrating a crypto payment API in 2026 is a strategic move that opens your business to a global, tech-savvy audience. By utilizing professional gateways that handle the heavy lifting of compliance and conversion, your team can focus on what matters: the product.

Ready to modernize your payment stack? Would you like me to draft a technical checklist for your dev team to use during the INXY sandbox testing phase?

Explore the mechanics behind cryptocurrency exchanges, from matching engines and liquidity pools to the differences between CEXs and DEXs. While exchanges power the digital economy for traders, discover why forward-thinking businesses are turning to specialized crypto payment gateways to safely accept digital assets and drive revenue.

In May 2010, a hungry programmer made financial history by trading 10,000 Bitcoins for two Papa John’s pizzas. At the time, there were no global marketplaces, no flashing price tickers, and absolutely no liquidity—just a simple forum post and a massive leap of faith. Today, the landscape has transformed beyond recognition. Those same pizzas would now be worth hundreds of millions of dollars, and the digital asset market has evolved into a trillion-dollar ecosystem.

At the beating heart of this financial revolution is the cryptocurrency exchange. Whether you are a retail investor looking to buy your first fraction of a Bitcoin, a professional trader executing high-frequency strategies, or a modern business owner trying to tap into a global, borderless customer base, understanding what a crypto exchange is and how it functions is the crucial first step to entering the digital economy.

The Engine of the Digital Economy

On any given day, top cryptocurrency exchanges process combined trading volumes exceeding $100 billion. They are the bustling, hyper-active metropolises of the digital age.

At its core, a cryptocurrency exchange is a highly secure digital marketplace that allows users to buy, sell, or trade cryptocurrencies for other assets. These assets can include conventional fiat money (like US Dollars or Euros) or other digital tokens. Exchanges act as the vital intermediary, providing the infrastructure, security, and liquidity necessary for the global crypto market to operate 24/7 without interruption.

Under the Hood: How an Exchange Functions

How does a platform handle millions of transactions per second without collapsing? Buying crypto might look like a simple tap on a smartphone screen, but the magic happens under the hood through several interconnected, highly advanced systems:

The Matching Engine: This is the absolute brain of the operation. The matching engine is an advanced software algorithm that continuously monitors and pairs buy and sell orders. When a buyer's bid meets a seller's asking price, the engine executes the trade in milliseconds.

Order Books and Market Depth: An order book is an electronic, real-time ledger of all the outstanding buy and sell orders for a specific trading pair (e.g., BTC/USD). It visualizes the current market depth, allowing traders to gauge ongoing supply, demand, and potential price movements.

Liquidity Pools: Liquidity dictates how easily an asset can be converted into cash without drastically affecting its market price. High liquidity means there are plenty of active buyers and sellers, resulting in lightning-fast transaction times and highly stable pricing.

Integrated Wallets: To facilitate instant trading, exchanges provide users with proprietary digital wallets. This allows traders to temporarily store their funds directly within the platform’s ecosystem for rapid deployment.

Centralized vs. Decentralized Exchanges (CEX vs. DEX)

As the industry has matured, two distinct philosophies have emerged regarding how these marketplaces should operate:

Centralized Exchanges (CEX): Platforms like Binance or Coinbase are owned and operated by a central corporate entity. They act as a trusted third party, offering deep institutional liquidity, fiat-to-crypto on-ramps, and user-friendly interfaces. The trade-off is that you must trust the corporation with the custody of your funds.

Decentralized Exchanges (DEX): Platforms like Uniswap operate entirely on blockchain technology using automated smart contracts. There is no central authority. Users retain 100% control of their funds by connecting their own private wallets. While they offer superior privacy and eliminate centralized points of failure, they can be intimidating for beginners.

The Commercial Shift: Why Businesses Need More Than an Exchange

This is where the story shifts from pure speculation to real-world commercial utility. With over 420 million active cryptocurrency users worldwide, digital assets are no longer just a niche internet hobby. They represent a massive, highly lucrative, and untapped consumer base. Recent industry surveys reveal a staggering metric: merchants who begin accepting crypto payments see an average ROI of up to 327%, with nearly 40% of their crypto-paying customers being entirely new to the brand.

However, here is the critical catch for corporate adoption. While exchanges are engineering marvels for individual traders, they are fundamentally not optimized for commercial B2B operations. If an online retailer or a global enterprise wants to accept crypto, directing clients to a standard exchange order book is a logistical nightmare. It leads to severe accounting errors, subjects the company to unpredictable withdrawal fees, and exposes business revenue to extreme, day-to-day price volatility.

To truly capitalize on the crypto economy, modern businesses require specialized, enterprise-grade infrastructure. The optimal solution is an advanced crypto payment gateway like inxy.io.

Instead of forcing merchants to navigate the speculative chaos of a trading platform, inxy.io is built specifically for seamless corporate integration. As a premier crypto payment gateway, it bridges the gap between digital assets and traditional commerce by offering:

An Automated Checkout Experience: It seamlessly integrates into a company's existing website or application, allowing global customers to pay in their preferred cryptocurrency in just a few clicks.

Instant Volatility Shielding: A premium gateway like inxy.io can instantly convert volatile crypto payments into stablecoins or fiat currency at the exact moment of the transaction, protecting the merchant's bottom line from sudden market crashes.

Cost-Efficiency and Compliance: By completely avoiding the heavy withdrawal constraints and hidden spread fees of retail exchanges, inxy.io provides transparent pricing, clear accounting, and professional invoicing tailored for corporate legal compliance.

Conclusion

Understanding the mechanics of a crypto exchange is essential for anyone navigating the modern financial landscape. They provide the necessary liquidity and global accessibility that keep the blockchain economy thriving. However, as digital assets move from the trading floor to the retail checkout, the tools we use must also evolve. While speculators will always rely on CEXs and DEXs, forward-thinking businesses must look toward specialized solutions. By leveraging a dedicated crypto payment gateway like inxy.io, companies can safely, efficiently, and profitably open their doors to the future of global commerce.