A global fintech and crypto strategist with experience across 80+ countries and 25 residencies, beginning in Nigeria. Combines deep cross-continental market insights, regulatory expertise, and hands-on sector engagement to guide international expansion in payments, blockchain, and digital finance.

Specialized in:

- Global crypto and fintech market entry

- Cross-border regulatory navigation

- Emerging market strategy in digital finance

- Blockchain adoption and payment infrastructure

- Focused on scalable, compliant financial innovation across diverse economic landscapes.

More atricles by author

What Is EURC? Circle's Euro Stablecoin Explained for Business Payments

Most stablecoins track the US dollar. But if your revenue, costs, and recipients are in euros, paying in a dollar-pegged token means an FX round-trip on every transaction. EURC solves that: it's a euro-denominated stablecoin that lets euro-native businesses move money on blockchain rails without leaving the euro.

Most stablecoins track the US dollar. But if your revenue, costs, and recipients are in euros, paying in a dollar-pegged token means an FX round-trip on every transaction. EURC solves that: it's a euro-denominated stablecoin that lets euro-native businesses move money on blockchain rails without leaving the euro.

Here's what EURC is, how it works, and why it has become the default euro stablecoin for regulated business in 2026.

EURC in one sentence

EURC (Euro Coin) is a stablecoin pegged 1:1 to the euro, issued by Circle — the same company behind USDC — and backed fully by euro-denominated reserves. One EURC is designed to always be redeemable for one euro.

Think of it as a digital euro you can send anywhere in minutes, 24/7, without a bank wire.

Who issues EURC, and why that matters

EURC is issued by Circle, a regulated financial technology company. That matters for one reason above all: regulation. Circle holds an EU Electronic Money Institution (EMI) license in France, and that single authorization passports EURC across all 27 EU member states under MiCA, the EU's crypto framework.

In practice, EURC is a MiCA-compliant e-money token. When MiCA's rules took full effect and non-compliant stablecoins were removed from EU-regulated exchanges, EURC was one of the assets that stayed — and it captured much of the resulting demand. By 2026 it had become the dominant euro stablecoin, holding roughly 41% of the euro-stablecoin market, up from about 17% a year earlier.

For a business, that means EURC isn't a fringe experiment — it's the euro stablecoin most likely to be accepted, supported, and compliant across Europe.

What backs EURC?

EURC is 100% backed by euro reserves held in cash and cash-equivalent instruments under Circle's full-reserve model. Circle publishes regular reserve reporting, the same transparency approach it applies to USDC. Each token in circulation is matched by euros held in reserve, which is what keeps the 1:1 peg dependable.

As of 2026, EURC's circulation sits in the range of roughly €400–460 million — smaller than dollar stablecoins, but by far the largest in the euro category.

Which blockchains support EURC?

EURC is a multi-chain asset. It runs natively on:

- Ethereum (where the majority of euro-stablecoin supply sits)

- Base

- Solana

- Stellar

- Avalanche

- World Chain

The network you use determines transfer speed and fees. For payouts, low-fee chains like Solana, Base, or Stellar keep costs to cents; Ethereum is the most liquid but the most expensive to transact on.

Why businesses use a euro stablecoin

If you already operate in euros, why hold a euro on a blockchain instead of in a bank? A few concrete reasons:

- No FX round-trip. Paying euro-based recipients in a dollar stablecoin means converting EUR → USD → EUR, losing spread each way. EURC keeps euros as euros.

- Speed. EURC settles in minutes, any time — including weekends and holidays, when SEPA and bank rails are closed.

- Global reach. A recipient anywhere with a wallet can receive euros, without needing a European bank account.

- Programmability. EURC can be sent via API for automated payouts, something traditional euro rails don't offer natively.

- Regulatory comfort. As a MiCA-compliant token, EURC fits the compliance expectations of European banks, auditors, and partners.

EURC vs a bank euro balance

A euro in your bank and a euro in EURC are both euros — the difference is the rails.

EURC doesn't replace your bank — it complements it for fast, global, programmable euro movement.

Frequently asked questions

What is EURC? EURC (Euro Coin) is a euro-pegged stablecoin issued by Circle, backed 1:1 by euro reserves. It lets businesses hold and send euros on blockchain networks.

Is EURC the same as USDC? They share an issuer (Circle) and a full-reserve, MiCA-compliant model, but EURC is pegged to the euro while USDC is pegged to the US dollar. See our EURC vs USDC comparison.

Is EURC regulated? Yes. EURC is a MiCA-compliant e-money token. Circle's French EMI license passports it across all 27 EU member states.

What backs EURC? Euro-denominated reserves held 1:1 against tokens in circulation, under Circle's full-reserve model with regular reserve reporting.

Which networks support EURC? Ethereum, Base, Solana, Stellar, Avalanche, and World Chain. Choose a low-fee network for cost-efficient payouts.

Can businesses pay in EURC? Yes — EURC is widely used for euro-denominated payouts to contractors, suppliers, and partners, especially within the EU. Learn more in our guide to paying in EURC.

Move euros the modern way

If your business runs on euros, you can settle in euros on-chain — fast, global, and MiCA-compliant. INXY's EURC mass payouts let you fund and pay in euros without the FX round-trip or the crypto overhead. New to the asset? Compare it with the dollar option in EURC vs USDC.

This article is general information, not financial or legal advice.

How to Pay Contractors and Affiliates in USDC: A Practical 2026 Guide

Paying a global team through banks means FX spreads, 3–5 day waits, intermediary fees, and a recipient in another country who receives less than you sent. Paying them in USDC — a fully-reserved, dollar-pegged stablecoin — can turn that into a same-day transfer for cents. But doing it properly, at scale, and in a way your accountant accepts takes more than a wallet.

Paying a global team through banks means FX spreads, 3–5 day waits, intermediary fees, and a recipient in another country who receives less than you sent. Paying them in USDC — a fully-reserved, dollar-pegged stablecoin — can turn that into a same-day transfer for cents. But doing it properly, at scale, and in a way your accountant accepts takes more than a wallet.

This guide walks through how to pay contractors in USDC — the setup, the networks, the compliance basics, and how to keep your books in fiat.

Why businesses pay in USDC

USDC (issued by Circle) is a stablecoin pegged 1:1 to the US dollar and backed by cash and short-dated US Treasuries, with monthly attestations from Deloitte. For paying people, that combination is the point:

- Stable value. Recipients get dollars, not a volatile asset. 1 USDC ≈ $1 at send and at cash-out.

- Speed. Payments settle in minutes, 24/7, including weekends and holidays.

- Global reach. Anyone with a wallet can receive, regardless of local banking.

- Low cost. On low-fee networks, a payout costs cents rather than a wire fee.

- Regulatory standing. USDC is MiCA-compliant in the EU, which makes it a durable choice for European corridors (more on that below).

Before you start: four things to get right

1. Confirm the recipient can receive USDC. They need a wallet address on a network you both support (Ethereum, Solana, Base, Polygon, and others). Confirm the network explicitly — a USDC transfer sent to the wrong network can be lost.

2. Decide who bears the fee. Will you gross up payments so the contractor receives the full agreed amount after network fees, or net it out? Set this in the contract.

3. Handle tax and classification. Paying in stablecoin doesn't change worker classification or your reporting obligations. Contractors are still responsible for their own taxes; you still keep records. Treat USDC payouts like any other payment for compliance purposes.

4. Keep fiat records. Your accounting should capture the fiat value at the time of payout, the fee, the recipient, and the transaction hash — not just on-chain data.

Method 1: Manual USDC payments

For a few contractors, you can pay directly from a self-custody wallet or exchange.

Steps:

- Fund a wallet with USDC and the network's gas token.

- Confirm each contractor's address and network in writing.

- Send each payment; send a small test transfer first for new, large recipients.

- Record each transaction hash against the invoice and its fiat value.

Limits: no automation, no built-in screening, and manual reconciliation. It works for a handful of people and breaks down beyond that.

Method 2: Bulk USDC payouts via CSV or API

For a real team — dozens or thousands of contractors, affiliates, or creators — a payout platform is the practical route. You prepare a recipient list and process it as one batch.

A typical flow:

- Fund in fiat. With a fiat-native provider like INXY, top up in EUR or USD via SEPA or SWIFT — no need to buy crypto yourself.

- Upload a CSV or call the API. Include recipient, amount, and network. The API path lets you trigger payouts straight from your own platform or billing system.

- Automated compliance. The provider runs KYT and sanctions screening and validates addresses before sending.

- Recipients get paid. USDC lands in minutes on supported networks.

- Reconcile in fiat. Export batch-level records with fiat values, fees, payout IDs, and hashes.

This removes the two hardest parts of paying a global team in crypto: compliance and accounting. You never manage keys or gas, and your finance team works in EUR or USD.

Choosing the network for USDC payouts

USDC runs natively on several chains. For payouts:

- Solana / Base / Polygon: cents per transfer, fast — ideal for high-volume contractor and affiliate payments.

- Ethereum (ERC-20): the most liquid and widely integrated, but the most expensive — reserve it for recipients who require it.

Match the network to the recipient's wallet and the payout size; a platform can route this automatically.

Compliance: don't skip screening

Paying contractors across borders means you're exposed to sanctions and AML rules. Two non-negotiables:

- Sanctions screening of recipient wallets before payout.

- Transaction monitoring (KYT) to flag high-risk addresses.

Manual and script-based payouts leave this to you. A regulated payout provider builds it into the flow — which is often the difference between "using crypto rails" and "creating a banking-risk problem."

Frequently asked questions

Can I pay international contractors in USDC? Yes. Anyone with a compatible wallet can receive USDC in minutes, regardless of country, as long as it's legal in their jurisdiction. It's widely used for cross-border contractor, freelancer, and affiliate payments.

Do I need to hold crypto to pay contractors in USDC? No. A fiat-native platform lets you fund in EUR or USD and keep accounting in fiat while recipients receive USDC.

Is paying contractors in USDC legal? Paying in USDC is legal in most jurisdictions, but you remain responsible for worker classification, tax reporting, and AML/sanctions compliance — the same as any payment method. Check local rules for your recipients.

What does it cost to pay someone in USDC? On low-fee networks like Solana, Base, or Polygon, a USDC transfer costs cents. On Ethereum it can be several dollars. Choosing the network controls the cost.

How do I keep accounting clean when paying in USDC? Record the fiat value at payout time, the fee, and the transaction hash for each payment. Payout platforms generate these exports automatically.

Pay your global team without the crypto overhead

If you're paying contractors, affiliates, or creators at scale, you shouldn't be managing wallets, gas, and screening by hand. INXY's mass USDC payouts let you fund in fiat, pay globally in minutes, and reconcile in EUR or USD — with compliance built in. Building a broader payroll flow? See our contractor payroll solution, or weigh the assets in our USDT vs USDC comparison.

USDT Network Fees Compared: TRC-20 vs ERC-20 vs BEP-20 vs Solana vs TON (2026)

USDT is a single asset, but it lives on more than a dozen blockchains — and the network you choose can change the cost of a transfer by 100x or more. For a one-off payment that's a rounding error. For a business sending thousands of payouts a month, picking the wrong chain quietly burns thousands of dollars.

USDT is a single asset, but it lives on more than a dozen blockchains — and the network you choose can change the cost of a transfer by 100x or more. For a one-off payment that's a rounding error. For a business sending thousands of payouts a month, picking the wrong chain quietly burns thousands of dollars.

This is a practical breakdown of the cheapest network to send USDT in 2026, what drives the fee on each chain, and how to match the network to the payout.

Why USDT fees vary so much

The fee to move USDT has nothing to do with Tether itself. It's the network's gas fee — paid in the chain's native token — that varies:

- On Ethereum (ERC-20) you pay ETH gas, which is priced by network congestion and can spike sharply.

- On Tron (TRC-20) you pay in TRX energy/bandwidth, which is low and stable.

- On Solana, TON, and BNB Chain, base fees are engineered to be very small.

So "how much does it cost to send USDT" is really "which network did you send it on."

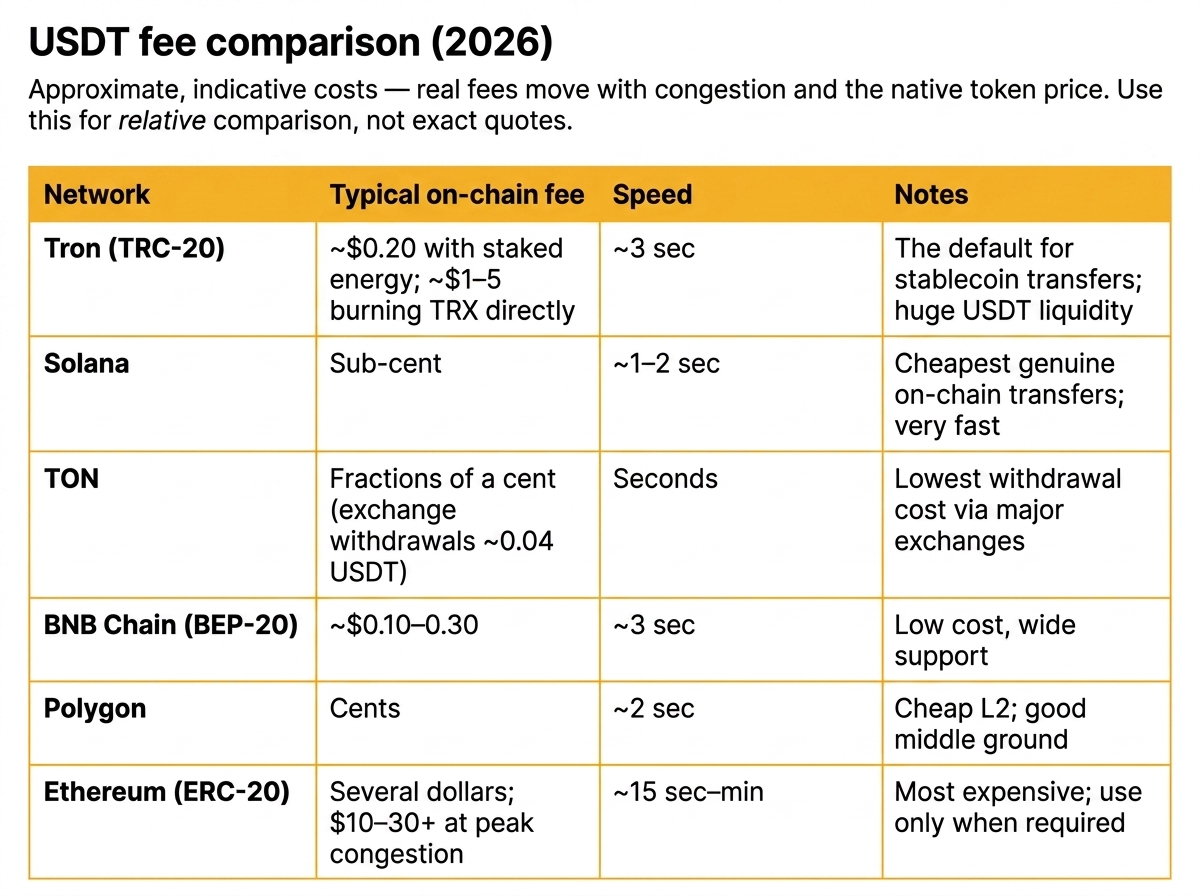

USDT fee comparison (2026)

Approximate, indicative costs — real fees move with congestion and the native token price. Use this for relative comparison, not exact quotes.

The short version: for pure on-chain cost, Solana and TRC-20 lead, with TON unbeatable for exchange withdrawals. ERC-20 is the most expensive and should be reserved for recipients who specifically need it.

Match the network to the payout amount

Cheapest isn't always "correct." The right network depends on the size of the transfer and where the recipient wants the funds.

- Micro-payouts (under ~$50): TRC-20, Solana, or TON. Fees would otherwise eat a meaningful slice of the payment.

- Standard payouts ($50–$5,000): Solana, Polygon, or TRC-20 keep costs to pennies while settling fast.

- Large transfers (over ~$5,000): Cost matters less relative to the amount. ERC-20 is acceptable if the counterparty requires it — the $10–20 fee is small against the principal, and Ethereum's liquidity and integrations are unmatched.

Beyond the headline fee

Fee-per-transfer is the obvious number. Three others matter just as much at scale:

1. Recipient acceptance. The cheapest network is useless if the recipient's wallet or exchange doesn't support it. Always confirm the network before sending — cross-network mistakes are irreversible.

2. Native-token overhead. Every network needs its gas token in your wallet. Running payouts across five chains means monitoring and topping up five different balances — an operational cost that doesn't show up in the per-transfer fee.

3. Failed and stuck transfers. Underpriced gas on congested networks means stuck transactions and support tickets. Reliability has a cost, too.

How platforms cut costs further

When you run payouts through a fiat-native platform instead of manually, network fees stop being your problem in two ways:

- Automatic routing. The platform sends each payout on a supported low-fee network without you managing gas on every chain.

- No native-token juggling. You fund a balance in EUR or USD; the provider handles conversion and gas. Your reporting stays in fiat.

That removes the hidden operational cost of multi-chain payouts, not just the visible per-transfer fee.

Frequently asked questions

What is the cheapest network to send USDT? For on-chain self-custody transfers, Solana and Tron (TRC-20) are cheapest, and TON offers the lowest withdrawal fees on major exchanges. Ethereum (ERC-20) is the most expensive.

Is TRC-20 always the cheapest for USDT? Not always. TRC-20 is very cheap and has the deepest USDT liquidity, but Solana and TON can be cheaper still per transfer. TRC-20 remains the most widely accepted low-fee option.

Why is sending USDT on Ethereum so expensive? ERC-20 transfers pay ETH gas, priced by network demand. During congestion, a single USDT transfer can exceed $30 in gas.

Does the network affect how much USDT the recipient receives? The network sets the fee you pay to send. Choosing a low-fee chain means more of your budget reaches recipients, especially across many small payouts.

Can I send USDT across networks? An address is tied to one network. To move USDT between chains you need a bridge or an exchange — you can't send TRC-20 USDT directly to an ERC-20 address.

Send on the right network, automatically

If you're running regular USDT payouts, you shouldn't be managing gas tokens across five blockchains. INXY's mass USDT payouts route each transfer over low-fee networks and report everything back in EUR or USD — so you get the cheapest path without the multi-chain overhead. New to bulk sending? Start with our step-by-step USDT payout guide.

How to Send USDT to Multiple Wallets: A Step-by-Step Bulk Payout Guide

Manual works for a handful of payees; scripts work if you want to run infrastructure. If you'd rather send USDT to hundreds or thousands of recipients from a fiat balance — with screening and clean reporting built in — that's exactly what INXY's mass USDT payouts are built for.

Paying twenty affiliates, two hundred contractors, or two thousand players one transaction at a time does not scale. If you need to send USDT to multiple wallets, the method you choose determines your cost, your error rate, and how much of your finance team's week disappears into copy-pasting addresses.

This guide covers the three practical ways to run a bulk USDT transfer in 2026 — manual, scripted, and platform-based — with the trade-offs of each, the mistakes that cost real money, and how to keep clean records for accounting.

What "mass USDT payout" actually means

A mass USDT payout is a single, structured operation that distributes Tether to many recipients at once. Instead of initiating each transfer by hand, you prepare a list of addresses and amounts and process them as a batch.

Three things make this harder than it looks:

- Network choice. USDT exists on Tron (TRC-20), Ethereum (ERC-20), BNB Chain (BEP-20), Solana, TON, Polygon and others. A recipient's address is network-specific — send TRC-20 USDT to an ERC-20 address and the funds are typically lost.

- Fees at volume. A fee that looks trivial for one transfer becomes a line item when multiplied across thousands of recipients.

- Reconciliation. Finance needs a fiat value, a timestamp, and a transaction hash for every payout — not just a wall of blockchain data.

Keep these three in mind; every method below is really a different answer to them.

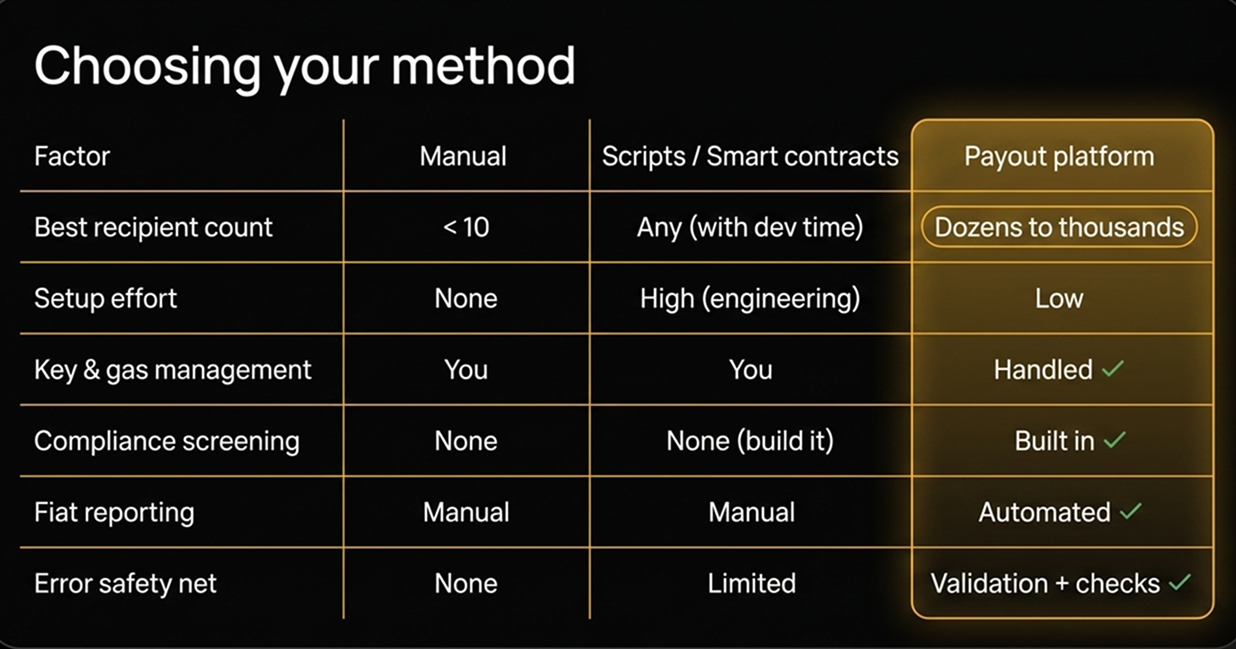

Method 1: Manual transfers from a wallet or exchange

The simplest approach is to send USDT one recipient at a time from a self-custody wallet (MetaMask, Trust Wallet, Tronlink) or an exchange account.

When it works: fewer than ~10 recipients, infrequent payouts, no automation budget.

Steps:

- Confirm each recipient's network and address in writing. Never assume the network.

- Fund your wallet with enough USDT and the native gas token (TRX for TRC-20, ETH for ERC-20, and so on).

- Send each transfer, double-checking the first and last four characters of every address.

- Save each transaction hash against the recipient's name for your records.

The catch: manual sending does not scale and has no safety net. A single mistyped address is irreversible. There is no batch confirmation, no built-in fiat reporting, and no sanctions screening. Beyond a handful of recipients, error risk climbs fast.

Method 2: Scripts and smart-contract batching

Technical teams can automate payouts with the blockchain's own tooling — a script that loops through a recipient list, or a "multisend" / "disperse" smart contract that pushes many transfers in one on-chain transaction.

When it works: you have engineering resources, a stable set of networks, and you want control over the flow.

What you gain:

- Batching efficiency. Multisend contracts bundle many recipients into a single transaction, which can reduce total gas versus sending individually on some networks.

- Full automation. A script can pull addresses from your database and fire payouts on a schedule.

What you take on:

- Key management. Your script needs access to a funded hot wallet holding private keys — an operational and security liability.

- Gas handling. You must monitor and top up the native token on every network you use.

- No compliance layer. Scripts don't screen recipients against sanctions lists or flag high-risk addresses. That's on you.

- Accounting glue. You still have to convert on-chain data into fiat-denominated records your auditors will accept.

Scripting trades human error for engineering overhead. It's powerful, but you are now running payment infrastructure as a side project.

Method 3: A payout platform (CSV or API)

A dedicated payout platform abstracts the wallet, keys, gas, and networks away. You upload a CSV of recipients or call an API, and the platform handles conversion, routing, screening, and delivery.

When it works: recurring payouts, dozens to thousands of recipients, finance teams that need clean fiat reporting, and businesses that don't want to become a crypto operation.

How a typical batch runs:

- Fund in fiat or stablecoin. Top up a balance — with a provider like INXY you can fund in EUR or USD via SEPA or SWIFT, so you never have to source crypto yourself.

- Upload or connect. Submit a CSV (recipient, amount, network) or send the batch through the API.

- Automated checks. The platform runs KYT and sanctions screening, auto-converts, and routes each payout to the right network.

- Recipients get paid. Delivery happens in minutes on supported low-fee networks.

- Report in fiat. You get batch-level exports with fiat values, fees, payout IDs, and transaction hashes — ready for reconciliation.

The trade-off is that you rely on a provider, but you remove key management, gas operations, compliance gaps, and accounting cleanup in one move.

Five mistakes that cost real money

- Wrong network. The most common irreversible loss. Always match the recipient's network to the address.

- Forgetting gas. A wallet full of USDT can't move without the native token for fees.

- No test transfer. For a new large recipient, send a small amount first and confirm receipt.

- Skipping screening. Paying a sanctioned or high-risk address is a legal and banking risk, not just a crypto one.

- Weak records. If you can't tie every hash to a fiat value and a recipient, month-end close becomes painful.

Frequently asked questions

Can I send USDT to many wallets in one transaction? On some networks, yes — a "multisend" smart contract bundles multiple recipients into one on-chain transaction. Otherwise, batching is handled off-chain by a platform that submits the transfers for you.

What's the cheapest way to send USDT in bulk? Low-fee networks such as Tron (TRC-20), Solana, and TON dramatically reduce per-transfer cost versus Ethereum. See our full USDT network fees comparison.

Do I need to hold crypto to run USDT payouts? Not with a fiat-native platform. You can fund in EUR or USD, keep your accounting in fiat, and let the provider handle conversion and delivery.

Is bulk USDT sending safe? The transfer itself is irreversible, so accuracy matters. Reputable platforms add address validation, KYT, and sanctions screening to reduce risk — protections that manual and script-based methods lack.

Scale it without the overhead

Manual works for a handful of payees; scripts work if you want to run infrastructure. If you'd rather send USDT to hundreds or thousands of recipients from a fiat balance — with screening and clean reporting built in — that's exactly what INXY's mass USDT payouts are built for.

MiCA Is Here: How INXY Built a Multi-Jurisdiction Model — and Migrated Every Client Before July 1

1 July 2026. Today marks the beginning of a new chapter for Europe's digital asset industry. The transitional period under the EU's Markets in Crypto-Assets Regulation (MiCA) has ended, and the standard for operating a crypto business in Europe has been raised for good.

1 July 2026. Today marks the beginning of a new chapter for Europe's digital asset industry. The transitional period under the EU's Markets in Crypto-Assets Regulation (MiCA) has ended, and the standard for operating a crypto business in Europe has been raised for good.

For years, much of the industry was built around a single jurisdiction. One license. One operating model. That worked while the rules were still evolving. It works less well now.

We want to be transparent with our clients about where INXY stands and what we did about it. INXY did not obtain a MiCA authorization in Poland. So rather than depend on any single jurisdiction, we moved to a multi-jurisdiction operating model — and before 1 July, we completed the migration of every client off our Polish entity. No payments paused. No settlement stopped.

Here's what MiCA is, what changed on 1 July, and how our model is built to keep your payments running through moments exactly like this one.

What is MiCA?

MiCA (Markets in Crypto-Assets Regulation) is the European Union's comprehensive framework for regulating crypto-assets and the companies that provide crypto services. It replaces a patchwork of national rules with a single, harmonized rulebook across all 27 member states.

In practice, MiCA does three main things:

- Licenses providers. Any company offering crypto-asset services — custody, exchange, transfers, payouts — must be authorized as a Crypto-Asset Service Provider (CASP) by a national regulator. A CASP license can then be "passported" across the EU.

- Regulates stablecoins. Issuers of stablecoins ("e-money tokens") must be authorized and hold strict, fully-backed reserves. This is why compliant stablecoins like USDC and EURC stayed available on EU-regulated venues while non-authorized ones were delisted. (More on this in "Is USDC regulated?")

- Sets conduct and transparency standards for how services are marketed and delivered.

MiCA's rules for service providers began applying on 30 December 2024, with a transitional window for existing firms.

What changed on 1 July 2026

MiCA included a transitional ("grandfathering") period under Article 143. Firms already operating legally under national regimes before 30 December 2024 could continue serving clients — but only until they obtained a CASP license or until 1 July 2026, whichever came first. That date has now passed, and there is no extension mechanism in the regulation.

From today, any provider serving EU clients must hold a MiCA CASP authorization. A legacy national registration no longer provides cover.

The situation in Poland made this especially clear. Poland has not yet enacted the national Crypto-Asset Market Act needed for its regulator (KNF) to issue CASP licenses — the act has been vetoed repeatedly, most recently in June 2026. In practice, that left Polish-registered providers with no domestic path to a CASP license before the deadline.

The limits of a single-jurisdiction model

MiCA is not simply making it harder to launch a crypto business. It is redefining what it means to run one: no longer just "get a license and go," but "operate reliably inside a regulated financial system."

That shift began well before 1 July. Across the market, some companies are spending the coming months restructuring. Some are migrating clients. Some are rethinking how they serve Europe altogether. The common thread is that betting an entire operation on one jurisdiction has become a single point of failure.

INXY's response: a multi-jurisdiction operating model

For payment infrastructure providers, continuity is not optional. Payments cannot pause because the regulatory landscape changes. Businesses still need to settle funds. Cross-border commerce continues every day. Infrastructure should adapt so that businesses don't have to.

That is why INXY expanded beyond a single jurisdiction and built a multi-jurisdiction operating model, spanning:

- Canada — registered Money Services Business (FINTRAC MSB M23375535)

- El Salvador

- Cyprus

- Switzerland

We did not build this because a deadline forced our hand at the last minute. We built it because our B2B clients need reliability that does not depend on the regulatory status of any one country. When the Polish route closed, that model is what let us complete the migration of all clients off our Polish entity before 1 July 2026 — with no interruption to payouts, settlement, or reporting.

What this means for you

- Your service continues. Clients were migrated ahead of the deadline and are served through our appropriately licensed entities. There is no gap in payouts or settlement.

- Your funds and reporting are unaffected. Fiat-denominated reporting, payout records, and reconciliation continue exactly as before.

- Your compliance standards are unchanged. Full KYB, KYC where needed, real-time transaction monitoring (KYT), and sanctions screening remain in force across every jurisdiction we operate in.

Regulation is becoming the foundation, not the obstacle

One conclusion runs through all of this: regulation is no longer just about compliance. It is becoming the foundation that enables institutional adoption of stablecoin infrastructure at scale. The businesses that treat regulatory resilience as core infrastructure — not paperwork — are the ones that will serve the next phase of the market.

That's the central theme of our latest research, Stablecoins 2026: The New Global Financial Settlement Layer, which maps the regulatory landscape and what it means for businesses building on stablecoin rails. (Link / request the report: [add URL].)

Frequently asked questions

Did INXY obtain a MiCA license? No. INXY did not obtain a MiCA authorization in Poland. Instead of relying on a single jurisdiction, we operate a multi-jurisdiction model across Canada, El Salvador, Cyprus, and Switzerland, chosen to give our B2B clients continuity.

What happened to clients on the Polish entity? All clients were migrated off our Polish entity before 1 July 2026. The migration was completed ahead of the MiCA transitional deadline, with no interruption to payments.

What is MiCA, in simple terms? MiCA is the EU's single set of rules for crypto companies and crypto-assets. It requires service providers to be licensed as CASPs and sets strict standards for stablecoins, consumer protection, and transparency across all member states.

What happened on 1 July 2026? MiCA's transitional period ended. From this date, providers serving EU clients must hold a MiCA CASP license; legacy national registrations no longer provide cover.

Will my payments pause? No. Continuity was the entire point of moving to a multi-jurisdiction model. Client migration was completed before the deadline, and settlement continues without interruption.

Talk to us

Regulatory change raises real questions for any business that moves money across borders. If you'd like to understand how our multi-jurisdiction model supports your payouts, contact our team — and we'd be glad to share our perspective as the industry enters this new phase.

This update is provided for information and does not constitute legal advice. Regulatory details are accurate as of 1 July 2026 and may evolve.

Crypto Checkout That Converts: Reducing Drop-off on Stablecoin Payments

You added crypto checkout to win new buyers — but the payment page is quietly leaking them. This guide breaks down exactly where stablecoin payments lose customers: network confusion, price-lock anxiety, wallet friction, unclear confirmations, and surprise fees. Learn the design and infrastructure fixes that turn a leaky pay page into one that converts — including why a well-built crypto checkout can beat cards, clearing ~99.9% of attempts with no chargebacks.

You added a crypto checkout to capture a new segment of buyers, and the demand is real — but the payment page is leaking customers. A shopper picks crypto, lands on the pay screen, hesitates, and disappears. That gap between intent and completed payment is checkout drop-off, and on crypto rails it has its own specific causes that most teams never diagnose.

This guide breaks down where stablecoin payments lose customers, the friction points that drive abandonment, and the concrete design and infrastructure choices that turn a leaky pay page into one that converts. The goal is simple: every shopper who chooses crypto should finish paying.

Why crypto checkouts lose customers

A crypto checkout is not just a card form with different logos. It introduces steps a Web2 buyer has never seen — choosing a network, copying an address, waiting for confirmations — and every unfamiliar step is a place to quit. Unlike a card decline, which the customer understands, a stalled or confusing crypto payment feels risky, and risk kills conversion.

Where drop-off actually happens

Most teams treat the checkout as a single event. It isn't. Crypto payment drop-off clusters at four distinct stages:

- Method selection — the customer considers crypto but doesn't trust it on your site, so they bounce before starting.

- Network and asset choice — faced with "ERC20 / TRC20 / BEP20" they don't recognize, they freeze.

- Wallet action — copying an address or scanning a QR code, switching apps, and fearing a mistake.

- Confirmation wait — the payment is sent but the page gives no clear signal it worked.

You cannot fix abandonment you can't see. Instrument each of these stages separately before changing anything.

Why a one-point conversion gain is worth chasing

Checkout is the highest-leverage surface you own. Traffic, ads, and product pages all exist to deliver a customer to this screen. Recovering even a few percentage points of crypto payment conversion rate here costs nothing in additional traffic — it simply stops you paying for visitors you then lose at the last step. For a business processing meaningful volume, a high-conversion gateway is not a nice-to-have; it is the difference between crypto being a growth channel and a vanity feature.

The main causes of stablecoin payment drop-off

Network and asset confusion

The single biggest source of friction is choice the customer can't evaluate. Asking a non-technical buyer to select between Tron, Ethereum, BNB Chain, and Polygon — each with different fees and speeds — is asking them to make a decision they're unqualified to make. Hesitation becomes abandonment.

Volatility and price-lock anxiety

If the amount due appears to move while the customer reads it, they assume they'll overpay or underpay. Even with stablecoin payments, buyers worry the quote will expire or shift. Without a visibly locked rate, the page feels unsafe.

Wallet friction and manual errors

Copy the address. Switch to the wallet app. Paste. Check the network matches. Confirm the gas. Send. Switch back. Each handoff is a chance to abandon — and the fear of sending funds to the wrong address or wrong chain is enough to make cautious buyers stop entirely.

Slow or unclear confirmation

A customer who has paid but sees a spinning loader with no explanation assumes the worst. On-chain confirmation times vary by network, and a checkout that doesn't explain the wait — or sets no expectation for it — converts the final, already-committed moment into a drop-off. (For the underlying mechanics, see our guide on how long crypto withdrawals and confirmations take.)

Fees, minimums, and surprise costs

A network fee that appears only at the final step, or a minimum the customer trips over, reads as a bait-and-switch. Surprise costs at the moment of payment are one of the most reliable abandonment triggers in any checkout — crypto included.

Missing trust and compliance signals

Crypto still carries a perception of risk for mainstream buyers. A pay page with no licensing, security, or brand reassurance gives a nervous customer every reason to close the tab. Trust is not decoration here; it is a conversion input.

How to design a crypto checkout that converts

Invoice in fiat, settle in stablecoins

Let the customer see the price in the currency they think in — EUR or USD — and pay in crypto behind the scenes, with automatic conversion to stablecoins or fiat on your side. This removes mental math, neutralizes volatility, and lets a Web2 buyer treat the transaction like any other payment. It is the foundation of a converting crypto checkout.

Reduce choices and default to the right network

Don't make the customer a blockchain expert. Pre-select a fast, low-fee network as the default and present asset options in plain language ("Pay with USDT" rather than "TRC20"). Fewer decisions mean fewer exit points. Every option you remove from the critical path is a conversion you keep.

Lock the rate and show a countdown

Display a fixed amount due with a clear, time-boxed quote ("This price is locked for 15:00"). A visible countdown does two things at once: it removes price anxiety and creates gentle urgency that pulls the customer through. Certainty converts.

Make the confirmation state legible

Tell the customer exactly what's happening: "Payment detected — confirming on-chain. This usually takes under a minute." Replace ambiguous spinners with a status that names the step and sets a time expectation. The moment after a customer pays is the worst possible time to leave them guessing.

Add fallback paths

Some customers will start a crypto payment and stall. Offer a clean way to switch methods or retry without losing the cart. A dead-end on a failed or abandoned crypto payment is a guaranteed loss; a graceful fallback recovers a share of it.

Build trust into the page

Show licensing and security signals where the customer makes the decision. INXY operates as licensed and regulated payment infrastructure with AML/KYB controls and partners including Sumsub, Elliptic, and Crystal — the kind of compliance signal that reassures a cautious buyer at exactly the right moment. Surface it; don't bury it in a footer.

Conversion benchmarks: crypto vs cards

When the checkout is built well, crypto doesn't just match card conversion — it can beat it. The structural advantages are real:

Cards fail far more often than most merchants realize — declines, 3-D Secure friction, and cross-border blocks routinely cost 5–30% of attempts. Crypto settlement is final and irreversible, which removes chargebacks entirely and lets a well-designed gateway clear close to every legitimate attempt. For merchants serving Europe, Asia, and LatAm, that reliability is a direct conversion uplift — INXY reports helping customers increase conversion rates by up to 40%. (For a wider comparison of providers and rails, see best payment gateways for SaaS in 2026.)

A pre-launch checklist

Before you ship a crypto checkout, confirm it does all of the following:

- Prices in the customer's fiat currency, with conversion handled automatically.

- Defaults to a fast, low-fee network instead of forcing a choice.

- Locks the rate with a visible countdown.

- Shows total cost up front, including any network fee — no surprises at the last step.

- Names the confirmation step and sets a time expectation.

- Offers a retry or fallback for stalled payments.

- Displays trust and compliance signals on the pay page itself.

- Tracks drop-off by stage, not just overall completion.

How INXY reduces crypto checkout drop-off

INXY's high-conversion API paygate is built around the principles above. Customers are invoiced in fiat and pay in crypto, with automatic conversion to stablecoins or fiat to remove volatility risk. You get settled in your bank account — in EUR or USD — as soon as the next day, with full reporting and an accounting-friendly setup for Web2 companies. The gateway supports 20+ cryptocurrencies across major networks (ERC20, TRC20, BEP20, Polygon, Tron, TON, and more), charges below 1% per transaction with no setup or hidden fees, and is engineered for a ~99.9% success rate.

The result is a checkout your customers finish — built to convert, not just to accept. Add it to your checkout page, webstore, platform, or app via API integration, or book a demo to see the conversion data for your business model.

FAQ

What causes drop-off on crypto checkouts? The most common causes are network and asset confusion, price-lock anxiety, manual wallet friction, unclear confirmation states, surprise fees, and missing trust signals. Each maps to a specific stage of the checkout, so the fix starts with measuring drop-off stage by stage rather than as a single number.

How do stablecoin payments improve checkout conversion? Stablecoins remove volatility from the transaction, so the amount due stays fixed while the customer pays. Pairing that with fiat-denominated pricing and automatic conversion lets a mainstream buyer complete a crypto payment as easily as a card payment — without exposure to price swings.

Is crypto checkout conversion really higher than cards? It can be. Crypto payments have no chargebacks and final settlement, and a well-built gateway can clear close to 99.9% of legitimate attempts versus 70–95% typical card success. The advantage is largest for cross-border and emerging-market customers, where cards are frequently declined or restricted.

Which network should a crypto checkout default to? Default to a fast, low-fee network so customers don't have to choose. Stablecoins on high-throughput networks settle in seconds for a fraction of the cost of slower chains, which both speeds confirmation and reduces the fee shown at checkout.

How do I add a high-conversion crypto checkout to my site? Use a payment gateway with API integration that handles fiat pricing, network selection, rate locking, and conversion for you. INXY integrates with your existing checkout, webstore, or app, and settles to your bank in EUR or USD — see get started.

Losing customers at the crypto pay page? Explore INXY's high-conversion payment gateway and turn stablecoin checkout into a channel that converts.

How Long Do Crypto Withdrawals Take? Processing Times, Fees & Speed Explained

This guide breaks down realistic timeframes by network, the factors that slow withdrawals down, whether "instant" withdrawals are genuine, and how to keep withdrawal fees low.

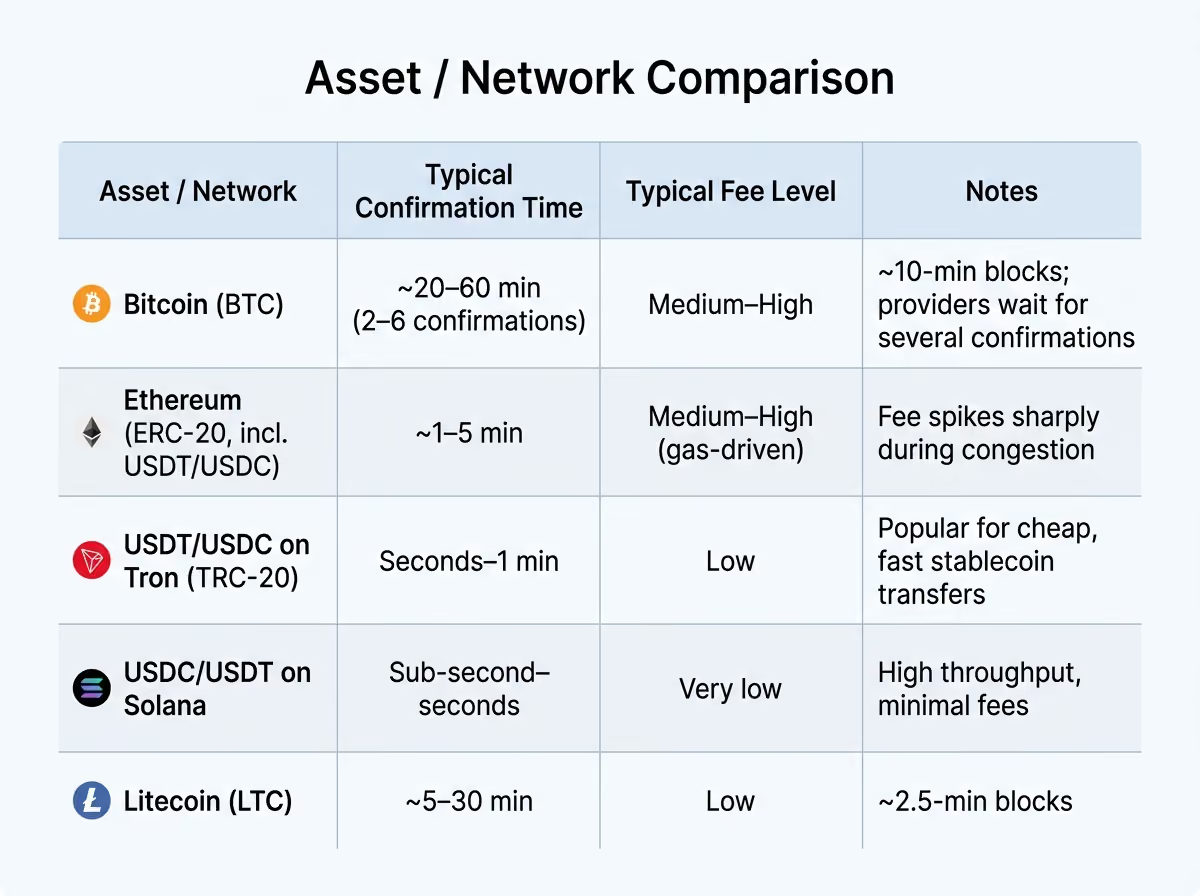

How long do crypto withdrawals take? In most cases, a crypto withdrawal clears in anywhere from a few seconds to about an hour — but the real answer depends on the blockchain you use, network congestion, and your provider's internal processing. A USDT transfer on a fast network can settle in under a minute, while a Bitcoin withdrawal held for multiple confirmations can take 30–60 minutes. This guide breaks down realistic timeframes by network, the factors that slow withdrawals down, whether "instant" withdrawals are genuine, and how to keep withdrawal fees low.

What Is a Crypto Withdrawal?

A crypto withdrawal is the process of moving digital assets out of an account — typically an exchange, custodial wallet, or payment platform — to an external blockchain address you control. Unlike an internal transfer between two accounts on the same platform, a crypto currency withdrawal is recorded on-chain, which means it must be broadcast to the network, validated by miners or validators, and confirmed in one or more blocks before it is final.

Two distinct stages determine how long the whole thing takes:

- Platform processing — the time your exchange or provider needs to review, batch, and sign the transaction before it ever touches the blockchain.

- Blockchain confirmation — the time the network needs to include your transaction in a block and add enough subsequent blocks to consider it irreversible.

A delay at either stage affects the total. A platform can sit on a request for 30 minutes for security reasons even when the underlying network would settle it in seconds.

How Long Do Crypto Withdrawals Take on Average?

For a healthy network and a provider without manual holds, most crypto withdrawals complete within a few minutes to one hour. The variance comes almost entirely from which chain you pick.

Exchange processing time vs blockchain confirmation time

Platform processing usually adds a few seconds to several minutes. Many providers batch outgoing transactions or run automated risk checks before broadcasting. After broadcast, the clock is controlled by the network: your transaction needs to be picked up by validators and then earn a number of confirmations — additional blocks built on top of it. The more confirmations a provider requires, the safer the transaction and the longer the wait.

Typical withdrawal times by network

The table below shows realistic ranges. Treat these as typical, not guaranteed — congestion and provider policy shift them.

The practical takeaway: the asset and network you choose matter far more than the platform. Sending the same stablecoin over Tron instead of Ethereum can turn a multi-minute, higher-fee withdrawal into a near-instant, low-cost one.

What Affects Crypto Withdrawal Speed?

When a withdrawal takes longer than expected, the cause is almost always one of three things.

Network congestion and gas fees

Every blockchain has limited block space. When demand is high, transactions compete to get included, and those attaching higher fees are prioritized. On networks like Ethereum, a low fee during a busy period can leave your transaction pending for much longer. This is why the same crypto withdrawal can clear in seconds one day and crawl the next.

Exchange security holds and withdrawal limits

Providers routinely apply temporary holds to protect funds. Common triggers include:

- A recent password, 2FA, or device change — many platforms freeze withdrawals for 24–48 hours afterward.

- First-time withdrawals to a new address, which may need additional verification.

- Amounts that exceed your tier's withdrawal limit, forcing a manual review or a split across days.

These holds are deliberate friction, not network delays — and they are the most common reason a withdrawal "stalls" while the blockchain itself is idle.

AML/KYC compliance checks

Regulated platforms screen withdrawals against anti-money-laundering and sanctions rules. Most checks are automated and invisible, but a flagged transaction can be paused for manual review. Larger amounts, transfers to newly seen addresses, or activity that breaks your normal pattern are more likely to be queued for a compliance look before release.

Are Instant Crypto Withdrawals Real?

The term instant crypto withdrawal is mostly marketing shorthand, and it means one of two things:

- Genuinely fast settlement on a fast chain. On high-throughput networks like Solana, or stablecoins on Tron, an instant crypto withdrawal is effectively real — confirmation lands in seconds. There is no magic here; the network is simply fast and cheap.

- Internal "instant" transfers. Some platforms advertise instant withdrawals that are actually off-chain movements between accounts on the same provider. These clear immediately because nothing is broadcast to the blockchain at all — which is fast, but only works inside that provider's ecosystem.

So crypto instant withdrawal is achievable, but read the fine print. A true on-chain "instant" withdrawal depends on the network you select. No provider can make a congested Bitcoin or Ethereum transaction settle instantly without raising the fee.

Crypto Withdrawal Fees Explained

Speed and cost are linked: paying a higher fee can buy faster inclusion, while choosing the wrong network can cost you both time and money. Understanding crypto withdrawal fees helps you optimize for both.

Network fees vs platform fees

A withdrawal fee usually has two components:

- Network (miner/validator) fee — paid to the blockchain to process the transaction. This is dynamic and rises with congestion. It is unavoidable, though it varies enormously by chain.

- Platform fee — an additional charge some providers add on top of the network fee. This is set by the provider and may be flat or percentage-based.

When comparing a crypto withdrawal fee across providers, separate these two. A platform advertising "zero fees" may still pass through a high network fee, and vice versa.

How to reduce crypto withdrawal fees

You have more control over cost than most people assume:

- Choose the right network. Sending stablecoins over Tron or Solana instead of Ethereum is the single biggest lever for low fees.

- Avoid peak congestion. Fees on busy chains drop when network demand falls.

- Batch withdrawals. Consolidating several payouts into fewer transactions reduces total network fees — valuable for businesses running frequent transfers.

- Mind the minimums. Small, frequent withdrawals get eaten by fixed costs; fewer, larger ones are more efficient.

For a crypto cash withdrawal — converting to fiat and sending to a bank — expect an extra layer of timing. The on-chain step may be fast, but the fiat leg typically settles in 1–5 business days depending on the banking rails (SEPA, SWIFT, ACH).

How Businesses Handle High-Volume Crypto Withdrawals

For a business paying suppliers, contractors, or affiliates, withdrawal speed is an operational metric, not a curiosity. Manual, one-by-one withdrawals on a slow or expensive network do not scale.

The businesses that get this right standardize on a few principles:

- Default to fast, low-fee networks for routine payouts, reserving slower chains only when a counterparty specifically requires them.

- Batch and automate outgoing transactions through an API rather than processing them by hand.

- Build compliance into the flow so AML/KYC checks happen up front and don't stall releases later.

This is exactly the problem a dedicated payouts infrastructure solves. INXY's crypto payouts let businesses automate high-volume transfers across networks with predictable timing and fees, while exchange and conversion tools handle the asset and fiat legs. The result is withdrawal speed you can plan around instead of monitoring anxiously.

FAQ

How long do crypto withdrawals take? Most crypto withdrawals complete within a few minutes to an hour. Stablecoins on fast networks like Tron or Solana can settle in seconds, while Bitcoin withdrawals held for several confirmations typically take 30–60 minutes. Platform security holds can add more time independent of the network.

Why is my crypto withdrawal taking so long? The usual causes are network congestion, a provider security hold (often after a recent password or device change), an AML/KYC compliance review, or a low network fee that deprioritizes your transaction. The blockchain itself may be idle while a platform-side hold is the real delay.

What is the fastest crypto to withdraw? Stablecoins on high-throughput networks — such as USDT on Tron or USDC on Solana — are among the fastest and cheapest to withdraw, typically settling in seconds for a low fee.

Can I get instant crypto withdrawals? Yes, in two senses: genuinely fast on-chain settlement on networks like Solana or Tron, or off-chain "instant" transfers between accounts on the same platform. A truly instant crypto withdrawal on a congested network like Bitcoin or Ethereum, however, is not realistic without paying a premium fee.

What is a crypto withdrawal? A crypto withdrawal moves digital assets from an account to an external blockchain address you control. It is recorded on-chain and must be confirmed by the network, which distinguishes it from an instant internal transfer within a single platform.

Ready to move crypto on a timeline you can plan around? Explore INXY's crypto payout and exchange tools for fast, low-fee transfers at scale.

Cross-Border B2B Payments With Stablecoins: The 2026 Guide to Faster, Cheaper Settlement

This guide explains how cross-border stablecoin payments actually work, how they compare to SWIFT, where they make the most sense, and what it takes to start accepting them.

For most businesses, sending money across borders still feels like it did a decade ago: slow, opaque, and expensive. Cross-border crypto payments built on stablecoins are changing that. Instead of routing an international crypto payment through a chain of correspondent banks, a stablecoin transfer settles directly on a blockchain in seconds, for a fraction of the cost. In 2026 this is no longer a fringe experiment — it is one of the fastest-growing segments in business payments, and the data behind it is hard to ignore.

This guide explains how cross-border stablecoin payments actually work, how they compare to SWIFT, where they make the most sense, and what it takes to start accepting them.

Why cross-border crypto payments are replacing the old rails

The traditional system was never designed for the speed of modern commerce. It was designed for banks talking to banks.

The hidden cost of SWIFT and correspondent banking

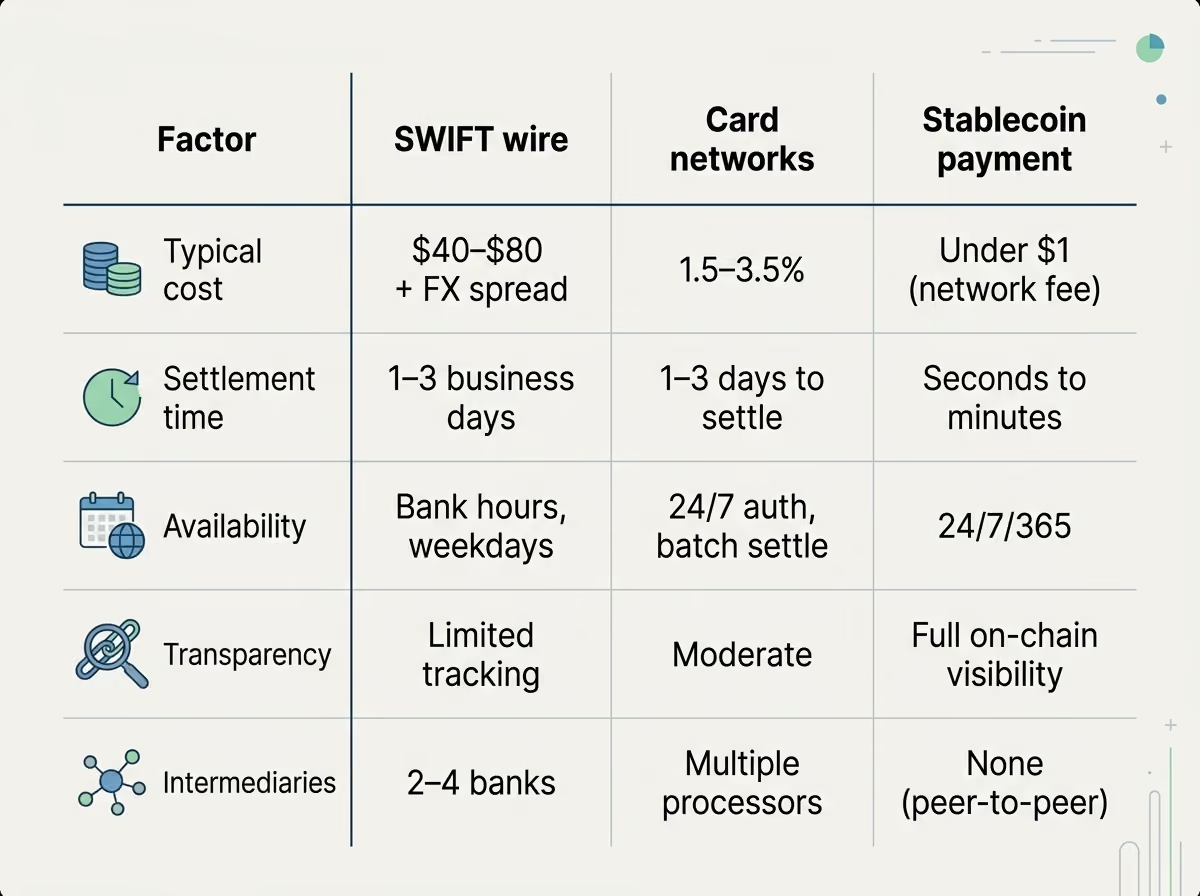

A typical international wire passes through two to four intermediary banks before it reaches the recipient. Each one takes a cut and adds a delay. The result is well known to any finance team: wire fees of roughly $40–$80 per transaction, settlement times of one to three business days (longer across exotic corridors), and almost no visibility into where the money is at any given moment. Add unfavorable FX spreads and the all-in cost of moving money internationally can quietly erode margins on every cross-border deal.

For a company paying dozens or hundreds of overseas suppliers, contractors, or partners each month, that friction compounds fast.

What changed in 2026

Stablecoins — blockchain tokens pegged 1:1 to a fiat currency such as the US dollar — turned out to be an almost perfect fit for this problem. They hold a stable value, move on open networks 24/7, and settle without a banking intermediary.

Adoption has gone vertical. Business-to-business stablecoin payment volume grew roughly 733% year over year heading into 2026, and total stablecoin transaction volume reached about $33 trillion in 2025. Juniper Research projects that cross-border B2B stablecoin payments will hit $5 trillion by 2035, up from an estimated $13.4 billion today, with the large majority of that future value coming specifically from cross-border business use. In short: the rail is being built right now, and businesses that learn it early gain a cost advantage.

How stablecoin cross-border payments actually work

The mechanics are simpler than the technology sounds. Every cross-border stablecoin payment follows the same three-stage path.

On-ramp, settlement, off-ramp

- On-ramp. The sender converts local fiat (USD, EUR, etc.) into a stablecoin such as USDC or USDT, either from existing treasury or through a payment provider.

- Settlement. The stablecoin moves across a blockchain network directly to the recipient's wallet. This is the step that replaces the entire correspondent-banking chain.

- Off-ramp. The recipient either holds the stablecoin or converts it back to their local currency and withdraws to a bank account.

A provider like INXY handles the on-ramp, settlement, and off-ramp as a single flow, so the business never has to touch a crypto exchange directly.

Stablecoins and networks used

Most B2B volume runs on US-dollar stablecoins — USDC, USDT, and increasingly PYUSD — because they remove currency-volatility risk while keeping the speed of crypto. The network matters too, because it determines how fast and how cheaply a payment finalizes:

- Solana — settlement finality in under half a second, with sub-cent fees.

- Tron — finality in roughly one to two seconds; widely used for USDT.

- Ethereum Layer-2s — low fees with fast confirmation, anchored to Ethereum security.

The practical takeaway: a payment that took three days on SWIFT can finalize in seconds on the right chain.

Stablecoins vs SWIFT: cost, speed, and transparency

The clearest way to understand the shift is a side-by-side comparison of low fee crypto payments against the legacy rails.

The economics are most dramatic at scale. Dropping from $40+ per wire to under $1 per transfer changes what is financially viable — micro-payments, frequent payouts, and thin-margin corridors that never made sense on SWIFT suddenly do.

Top use cases for global crypto transactions

Stablecoins are not a fit for every payment, but for global crypto transactions between businesses they solve real, recurring pain.

- Supplier and vendor payments. Pay overseas manufacturers and service providers same-day instead of waiting for a wire to clear, improving supplier relationships and unlocking faster terms.

- Contractor and team payouts. Pay international contractors and remote staff in stablecoins without losing 5–10% to fees and FX on every transfer. (INXY also covers dedicated crypto payroll.)

- Marketplace and platform payouts. Distribute earnings to sellers, affiliates, or creators across many countries in a single batch, at predictable cost.

- Treasury and intercompany transfers. Move funds between entities and regions instantly, holding value in a dollar-pegged asset rather than parking it in slow, fee-heavy banking channels.

These are exactly the corridors where the old system performs worst — many small-to-mid payments, many destinations, tight margins.

Are low fee crypto payments compliant? GENIUS Act and MiCA

A fair question from any finance or legal team: is this allowed? In 2026, the answer is increasingly yes — and the regulatory ground is firmer than it has ever been.

In the United States, the GENIUS Act established the first federal framework for payment stablecoins, requiring issuers to be licensed, to hold 1:1 reserves in high-quality liquid assets, and to honor redemption on demand. In the European Union, MiCA (Markets in Crypto-Assets) provides a parallel framework. Together they have moved stablecoins from a regulatory gray zone into supervised, standardized instruments — which is a large part of why institutional adoption accelerated.

What a regulated provider handles for you

Compliance does not have to live on your team. A regulated payment provider performs KYB (Know Your Business) onboarding, screens transactions against AML requirements, and maintains the audit trail you need for reporting. The business gets the speed and cost benefits of stablecoins while the provider absorbs the regulatory heavy lifting.

How to start accepting cross-border crypto payments

Getting started is closer to onboarding a payment processor than to learning crypto.

- Choose a regulated provider that supports on-ramp, settlement, and off-ramp in your corridors — not a raw exchange.

- Complete KYB onboarding and connect your bank account or treasury.

- Pick your stablecoins and networks (USDC/USDT on a fast, low-fee chain) and set how recipients receive funds — held as stablecoin or auto-converted to local fiat.

- Integrate and pay. Use the dashboard for one-off and batch payments, or the API to automate payouts inside your existing systems.

Once live, a cross-border payment that used to mean a wire form and a three-day wait becomes a few clicks and a few seconds.

The bottom line

Cross-border B2B payments are being rebuilt on stablecoin rails, and the trend lines — 733% volume growth, a projected $5 trillion market, and clear regulation under the GENIUS Act and MiCA — point in one direction. For businesses that move money internationally, stablecoins offer dramatically lower fees, near-instant settlement, and full transparency, without the volatility of traditional crypto. The companies adopting it now are the ones that will spend the next decade paying cents where their competitors pay tens of dollars.

Start accepting cross-border crypto payments with INXY →

FAQ

Are stablecoin payments legal for business? Yes. In 2026, US-dollar stablecoins are regulated under the GENIUS Act in the United States and MiCA in the EU. Using a licensed provider keeps your KYB and AML obligations covered.

How fast is settlement? Depending on the network, a stablecoin payment finalizes anywhere from under a second (Solana) to a couple of minutes — versus one to three business days for a SWIFT wire.

What fees apply? The main cost is a small blockchain network fee, often under $1, plus any provider conversion fee on the on-ramp or off-ramp. This compares to $40–$80 per traditional international wire.

USDC or USDT for cross-border payments? Both are widely accepted dollar-pegged stablecoins. USDC is often preferred for its regulatory transparency; USDT has deeper liquidity in some corridors. A good provider supports both so you can match the recipient's preference.

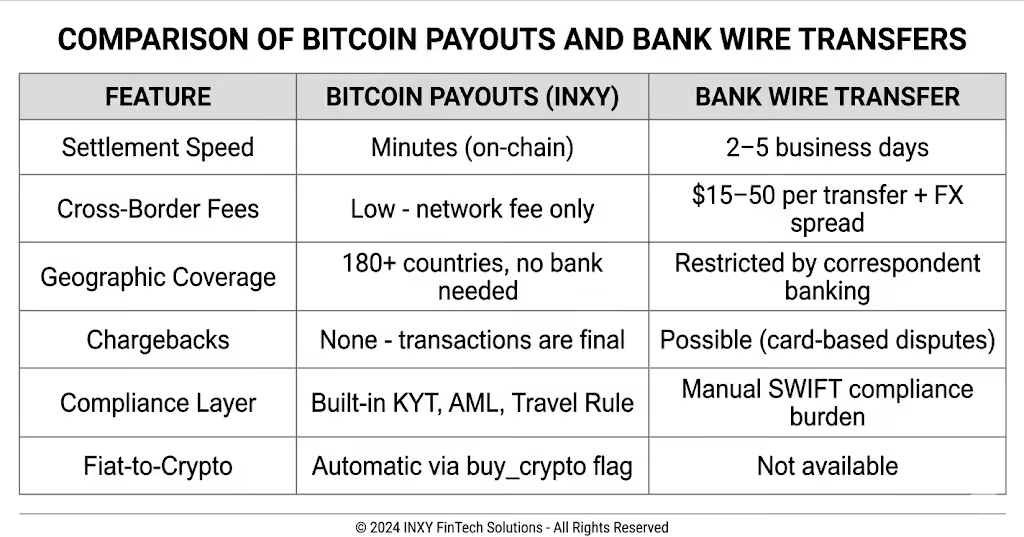

Pay Employees and Contractors in Bitcoin

Automate BTC payouts for global teams with INXY Payments — no crypto infrastructure required. Fast, compliant, and built for business.

Why Businesses Are Choosing Bitcoin for Payroll and Contractor Payments

As remote work becomes the global standard, companies face a common challenge: paying international teams through traditional banking is slow, expensive, and geographically limited. Bitcoin payouts eliminate SWIFT delays, excessive conversion fees, and banking restrictions — letting businesses pay employees and contractors in Bitcoin within minutes, regardless of their location.

From affiliate networks and iGaming platforms to SaaS companies and freelancer marketplaces, paying in Bitcoin is no longer a niche practice. Paying employees in Bitcoin and contractors in BTC is no longer reserved for crypto-native startups — it is a competitive edge in global talent acquisition that reduces operational costs across the board. INXY Payments makes this straightforward: no need to buy Bitcoin in advance, no separate exchange accounts, no manual compliance work — everything runs through a single B2B platform built for exactly this use case.

How to Pay Employees in Bitcoin with INXY: 3 Simple Steps

- Create an INXY Account & Complete KYB — Sign up as a business, submit your company documents, and pass KYB verification through the INXY dashboard. Your organisation is reviewed and activated within 1–3 business days — no crypto expertise required.

- Add Recipients or Connect the Payouts API — Upload a CSV file with recipient BTC addresses via the INXY dashboard, or integrate the Payouts API directly into your platform for fully automated workflows. The API is built to handle payouts at scale — no hard limit on the number of recipients per cycle. Real-time webhook notifications keep your system updated on each payout status.

- Send BTC Payouts — from Crypto or Fiat — Trigger single or mass BTC payouts from your balance. If you hold EUR or USD, INXY's buy_crypto flag auto-converts your fiat to Bitcoin at the moment of each payout — no pre-purchased BTC required, no exchange accounts to manage.

Benefits of Bitcoin Payouts for Business

Global Reach Without Banking Limits

Bitcoin payouts via INXY work for recipients in any country, with or without a bank account. No correspondent bank fees, no SWIFT delays, no rejected transfers due to local banking restrictions. Your payroll operates globally, on your schedule.

No Chargebacks

Crypto transactions are final and immutable. Once a BTC payout is broadcast to the network, it cannot be reversed or disputed — a critical advantage for high-volume affiliate and iGaming payouts where chargeback fraud is a constant risk.

Instant Settlement

BTC payouts initiated through INXY are broadcast on-chain within minutes. Compared to international wire transfers that take 2–5 business days, Bitcoin delivers settlement speed that matches the pace of modern business operations.

Pay from Fiat, Send in Bitcoin

If your treasury operates in EUR or USD, there is no need to pre-purchase Bitcoin on an exchange. INXY's buy_crypto feature handles the fiat-to-BTC conversion automatically at the moment each payout is triggered — the exchange rate is locked at execution time, and the full flow is recorded in your transaction history.

Built-In Compliance — KYT, AML, Travel Rule

Every BTC payout processed through INXY goes through KYT (Know Your Transaction) screening before broadcast. High-risk addresses are blocked automatically. For recipients in your Contact List, Travel Rule data exchange via Notabene is handled by the platform — no manual compliance burden on your team.

Who Uses Bitcoin Payouts?

Affiliate Networks & CPA Platforms

Affiliate networks need to pay hundreds or thousands of publishers worldwide, often weekly or bi-weekly. INXY supports batch processing of up to hundreds of recipients per API call, with full webhook notifications on payout status. Mass payouts that previously took 5 banking days now complete in minutes — and companies that pay employees and contractors in Bitcoin report significantly lower operational overhead.

iGaming & Online Gaming Platforms

Gaming and gambling platforms regularly pay out winnings and contractor fees in crypto. Bitcoin is the preferred payout currency for many players and partners due to its universal recognition and broad wallet support. INXY's compliance layer — KYT screening, AML review, Travel Rule — ensures platforms stay clean without building their own infrastructure.

Remote-First Companies & Tech Teams

Companies with globally distributed engineering, design, or operations teams use INXY to offer Bitcoin as an alternative compensation option. Contractors who prefer crypto over bank transfers get paid faster, while the company avoids currency conversion overhead and cross-border banking fees.

Freelancer Marketplaces & Gig Economy Platforms

For platforms managing large pools of independent contractors, mass Bitcoin payouts through INXY reduce the operational cost of international payroll significantly. One file upload or one API call pays thousands of contractors in a single batch — with per-recipient status tracking and exportable CSV reports.

Frequently Asked Questions

Is it legal to pay employees in Bitcoin?

In most jurisdictions, paying contractors in Bitcoin is fully legal. For full-time employees, regulations vary: many countries — including the US, UK, and EU member states — allow crypto salary supplements or contractor payments in crypto, but typically require that the minimum statutory wage be paid in local fiat currency. Consult local labour law before switching your primary payroll to Bitcoin.

Can you pay employees in Bitcoin in the US?

Yes. The Fair Labor Standards Act (FLSA) requires that the federal minimum wage be paid in US dollars, but additional compensation — including contractor payments and performance bonuses — can be made in Bitcoin. Many US-based companies and DAOs already pay freelancers and contractors in BTC without legal issues.

Which companies pay employees in Bitcoin?

A growing number of global businesses pay employees and contractors in Bitcoin, particularly in tech, gaming, and affiliate marketing industries. Remote-first companies, crypto-native startups, and platforms with large contractor networks were early adopters. With infrastructure like INXY, any B2B business can now add BTC payouts without building crypto capabilities in-house.

How does INXY's buy_crypto flag work for BTC payouts?

If your INXY balance is in EUR or USD, the buy_crypto: true flag triggers an automatic fiat-to-BTC exchange at the moment each payout is initiated. The exchange rate is locked at execution time, and the network fee is deducted from the payout amount. You do not need to hold Bitcoin in advance — INXY handles the conversion in the same transaction flow.

What happens if a BTC address is flagged as high-risk?

Before any payout is created, INXY screens the recipient's BTC address through KYT. If the address is flagged as high-risk, the payout is blocked automatically and you receive an error notification via webhook and dashboard. You can review the case and contact the INXY compliance team if needed.

What is the maximum number of Bitcoin payouts per batch?

INXY's infrastructure handles payout cycles of any size — from small partner networks to programs with hundreds of recipients — all processed in minutes, with full webhook notifications on each transaction.

Start Sending Bitcoin Payouts with INXY

Ready to pay your global team in Bitcoin? Join hundreds of businesses that use INXY Payments to run fast, compliant BTC payouts — from a single contractor to thousands of recipients. No crypto expertise required, no pre-purchased Bitcoin needed, no separate exchange accounts.

Get Started with INXY — Free Setup

Already have an account? Go to Send Crypto → Payouts in your INXY dashboard.

How to Automate Mass Crypto Payouts for International Freelancers

Wire transfers are draining freelance platform margins with high fees, opaque FX spreads, and week-long settlement delays. Automated mass crypto payouts via stablecoins like USDT and USDC eliminate these bottlenecks — processing thousands of global transactions in seconds through a single API call. This guide walks through the full transition: choosing the right digital assets, integrating a payout API, and automating reconciliation at scale.

How to Automate Mass Crypto Payouts for International Freelancers

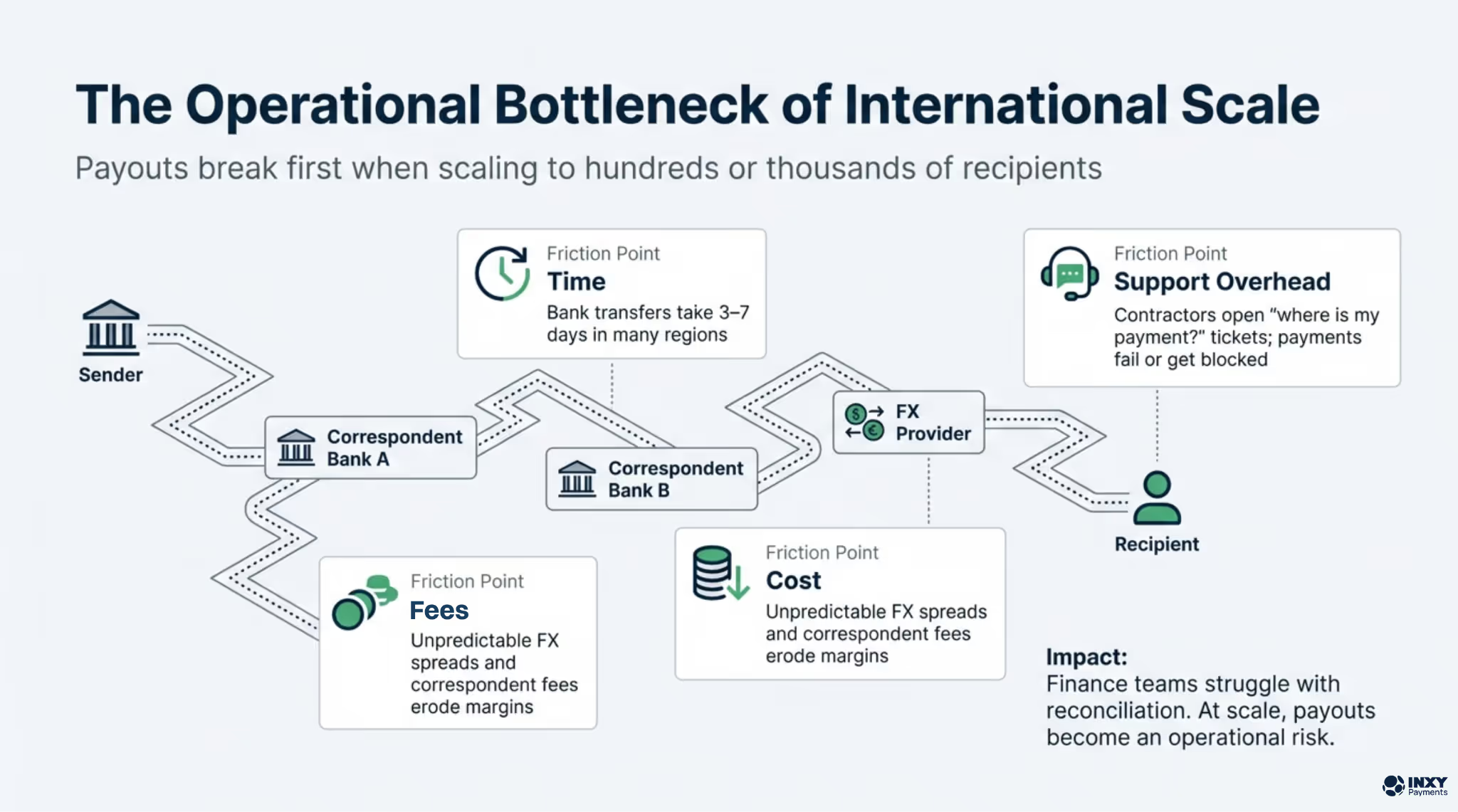

It is payday, and your finance department is drowning in a massive spreadsheet filled with SWIFT codes, routing numbers, and fluctuating exchange rates. A few days later, your support channels are flooded with frustrated messages from international developers who still have not received their money because a correspondent bank mysteriously held the funds. If you operate a global freelance platform, a talent marketplace, or a remote agency, this logistical nightmare is likely your recurring reality. While hiring elite talent across borders is frictionless, compensating them remains stuck in the 1990s.

Legacy banking rails actively erode your profit margins with exorbitant fees and damage your reputation among top professionals. It is time to stop burning cash and developer hours on slow wire transfers. By transitioning to automated mass cryptocurrency payouts – specifically leveraging stablecoins you can execute thousands of global transactions simultaneously, settling payments in seconds rather than unpredictable weeks.

The Bottleneck of Traditional Global Payroll

Processing international payroll through fiat channels involves a convoluted chain of intermediary banks, each extracting a cut and adding days to the settlement timeline. The traditional system is plagued by critical operational pain points for freelance platforms:

- Exorbitant Transaction Fees: Standard wire transfers cost $15 to $50 per transaction. This makes frequent micro-payouts to temporary contractors or gig workers entirely unfeasible.

- Unpredictable Settlement Delays: Cross-border payments routinely take three to seven business days to clear, causing immense anxiety for freelancers relying on timely income.

- Hidden FX Markups: Banks apply highly unfavorable foreign exchange spreads, directly reducing the contractor's purchasing power and causing disputes over missing funds.

- Severe Financial Exclusion: Talented professionals in emerging markets are often completely locked out of standard, legacy payment methods like PayPal or Stripe.

The Mechanics of Crypto Payout Automation

Shifting platform operations to cryptocurrency, particularly utilizing stablecoins like USDT or USDC, neutralizes these flaws. Because they are securely pegged to the US Dollar, they eliminate the price volatility of digital assets like Bitcoin.

The true transformative power for your platform lies in API automation. Instead of a finance manager manually processing invoices one by one, a mass payout system allows your backend infrastructure to trigger hundreds of transactions simultaneously through a single API call. Executed via automated batch processing on high-speed blockchains like Tron or Polygon, network fees drop to mere pennies.

Step-by-Step Guide to Automating Global Payouts (тут нужна помощь Артем в правильности шагов)

Transitioning to a crypto-first compensation model requires a strategic technical approach to ensure smooth onboarding for your contractors:

- Select the Right Digital Assets: Default to stablecoins (USDT/USDC) on fast networks to ensure negligible gas fees and zero price volatility for the receiving party.

- Integrate a Payout API: Connect your backend directly to a dedicated crypto gateway supporting mass payout endpoints instead of trying to build and maintain complex nodes from scratch.

- Map Contractor Wallets: Update your platform onboarding flow to allow freelancers to securely save and verify their digital wallet addresses alongside their traditional profile data.

- Automate Trigger Events: Configure your platform's internal logic so that approved timesheets, completed milestones, or specific calendar dates automatically trigger the API payout calls.

- Streamline Reconciliation: Utilize a gateway that provides detailed transaction hashes and automated ledger updates so your accounting team can track successful disbursements in real-time.

INXY: The Premier Payout Gateway for Freelance Platforms

Implementing automated financial infrastructure requires an enterprise-grade technological backbone. For global talent marketplaces, remote agencies, and HR platforms modernizing their compensation systems, INXY stands out as the ultimate strategic partner.

INXY provides a powerful cryptocurrency payment gateway designed specifically for the high-volume, automated disbursement needs of the gig economy. By integrating the INXY API, your platform can automate mass crypto payroll effortlessly, completely removing the heavy lifting of blockchain node management. We act as the secure bridge between your administrative dashboard and the blockchain, ensuring rapid global settlement, automated transaction reconciliation, and flawless execution for every single contractor payout. Our infrastructure scales perfectly alongside your growing international workforce.

Conclusion

The future of global work is undeniably decentralized, and platform compensation methods must evolve to keep pace. Automating mass crypto payouts is not just an operational upgrade; it is a profound competitive advantage that attracts and retains top global talent who demand fast, transparent payments. Do not let outdated banking rails hold your platform's growth hostage.

Ready to revolutionize your payroll system and automate your global disbursements? Discover how our robust API solutions can scale your platform securely by visiting https://www.inxy.io/ today.

How does Crypto Exchange work?

Explore the mechanics behind cryptocurrency exchanges, from matching engines and liquidity pools to the differences between CEXs and DEXs. While exchanges power the digital economy for traders, discover why forward-thinking businesses are turning to specialized crypto payment gateways to safely accept digital assets and drive revenue.

In May 2010, a hungry programmer made financial history by trading 10,000 Bitcoins for two Papa John’s pizzas. At the time, there were no global marketplaces, no flashing price tickers, and absolutely no liquidity—just a simple forum post and a massive leap of faith. Today, the landscape has transformed beyond recognition. Those same pizzas would now be worth hundreds of millions of dollars, and the digital asset market has evolved into a trillion-dollar ecosystem.

At the beating heart of this financial revolution is the cryptocurrency exchange. Whether you are a retail investor looking to buy your first fraction of a Bitcoin, a professional trader executing high-frequency strategies, or a modern business owner trying to tap into a global, borderless customer base, understanding what a crypto exchange is and how it functions is the crucial first step to entering the digital economy.

The Engine of the Digital Economy

On any given day, top cryptocurrency exchanges process combined trading volumes exceeding $100 billion. They are the bustling, hyper-active metropolises of the digital age.

At its core, a cryptocurrency exchange is a highly secure digital marketplace that allows users to buy, sell, or trade cryptocurrencies for other assets. These assets can include conventional fiat money (like US Dollars or Euros) or other digital tokens. Exchanges act as the vital intermediary, providing the infrastructure, security, and liquidity necessary for the global crypto market to operate 24/7 without interruption.

Under the Hood: How an Exchange Functions

How does a platform handle millions of transactions per second without collapsing? Buying crypto might look like a simple tap on a smartphone screen, but the magic happens under the hood through several interconnected, highly advanced systems: