USDT is a single asset, but it lives on more than a dozen blockchains — and the network you choose can change the cost of a transfer by 100x or more. For a one-off payment that's a rounding error. For a business sending thousands of payouts a month, picking the wrong chain quietly burns thousands of dollars.

This is a practical breakdown of the cheapest network to send USDT in 2026, what drives the fee on each chain, and how to match the network to the payout.

Why USDT fees vary so much

The fee to move USDT has nothing to do with Tether itself. It's the network's gas fee — paid in the chain's native token — that varies:

On Ethereum (ERC-20) you pay ETH gas, which is priced by network congestion and can spike sharply.

On Tron (TRC-20) you pay in TRX energy/bandwidth, which is low and stable.

On Solana, TON, and BNB Chain, base fees are engineered to be very small.

So "how much does it cost to send USDT" is really "which network did you send it on."

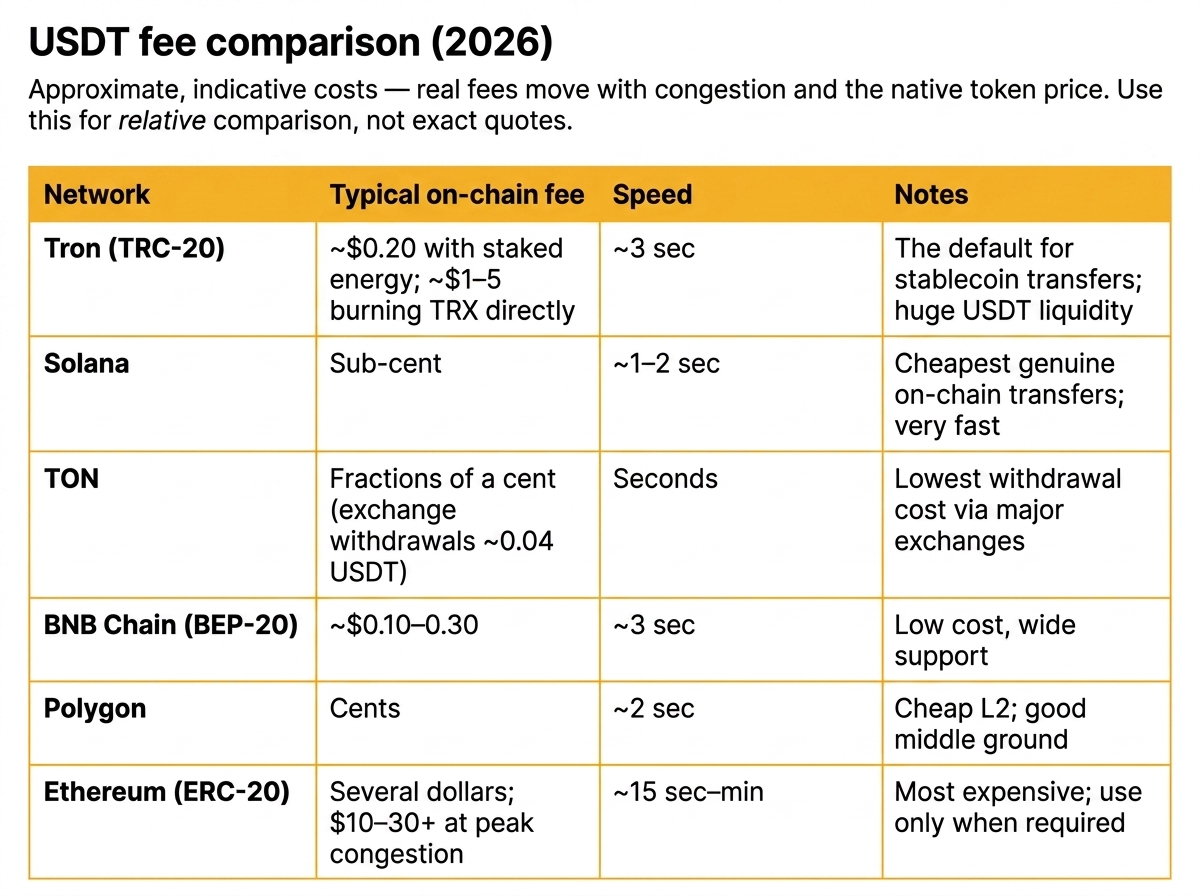

USDT fee comparison (2026)

Approximate, indicative costs — real fees move with congestion and the native token price. Use this for relative comparison, not exact quotes.

The short version: for pure on-chain cost, Solana and TRC-20 lead, with TON unbeatable for exchange withdrawals. ERC-20 is the most expensive and should be reserved for recipients who specifically need it.

Match the network to the payout amount

Cheapest isn't always "correct." The right network depends on the size of the transfer and where the recipient wants the funds.

Micro-payouts (under ~$50): TRC-20, Solana, or TON. Fees would otherwise eat a meaningful slice of the payment.

Standard payouts ($50–$5,000): Solana, Polygon, or TRC-20 keep costs to pennies while settling fast.

Large transfers (over ~$5,000): Cost matters less relative to the amount. ERC-20 is acceptable if the counterparty requires it — the $10–20 fee is small against the principal, and Ethereum's liquidity and integrations are unmatched.

Beyond the headline fee

Fee-per-transfer is the obvious number. Three others matter just as much at scale:

1. Recipient acceptance. The cheapest network is useless if the recipient's wallet or exchange doesn't support it. Always confirm the network before sending — cross-network mistakes are irreversible.

2. Native-token overhead. Every network needs its gas token in your wallet. Running payouts across five chains means monitoring and topping up five different balances — an operational cost that doesn't show up in the per-transfer fee.

3. Failed and stuck transfers. Underpriced gas on congested networks means stuck transactions and support tickets. Reliability has a cost, too.

How platforms cut costs further

When you run payouts through a fiat-native platform instead of manually, network fees stop being your problem in two ways:

Automatic routing. The platform sends each payout on a supported low-fee network without you managing gas on every chain.

No native-token juggling. You fund a balance in EUR or USD; the provider handles conversion and gas. Your reporting stays in fiat.

That removes the hidden operational cost of multi-chain payouts, not just the visible per-transfer fee.

Frequently asked questions

What is the cheapest network to send USDT? For on-chain self-custody transfers, Solana and Tron (TRC-20) are cheapest, and TON offers the lowest withdrawal fees on major exchanges. Ethereum (ERC-20) is the most expensive.

Is TRC-20 always the cheapest for USDT? Not always. TRC-20 is very cheap and has the deepest USDT liquidity, but Solana and TON can be cheaper still per transfer. TRC-20 remains the most widely accepted low-fee option.

Why is sending USDT on Ethereum so expensive? ERC-20 transfers pay ETH gas, priced by network demand. During congestion, a single USDT transfer can exceed $30 in gas.

Does the network affect how much USDT the recipient receives? The network sets the fee you pay to send. Choosing a low-fee chain means more of your budget reaches recipients, especially across many small payouts.

Can I send USDT across networks? An address is tied to one network. To move USDT between chains you need a bridge or an exchange — you can't send TRC-20 USDT directly to an ERC-20 address.

Send on the right network, automatically

If you're running regular USDT payouts, you shouldn't be managing gas tokens across five blockchains. INXY's mass USDT payouts route each transfer over low-fee networks and report everything back in EUR or USD — so you get the cheapest path without the multi-chain overhead. New to bulk sending? Start with our step-by-step USDT payout guide.

How to Verify a Merchant Account? Step-by-Step Guide

Navigating the regulatory landscape of 2026 is crucial for any business accepting digital assets. This guide provides a comprehensive, step-by-step walkthrough of the merchant verification process for crypto payment gateways in the European Union. From understanding the Markets in Crypto-Assets (MiCA) regulation to mastering the Know Your Business (KYB) documentation requirements, we detail exactly how to secure a verified, bank-grade account. Whether you are in e-commerce, hosting, or high-risk industries, this unified framework ensures your business is compliant, secure, and ready for the global economy.

The institutionalization of the digital asset economy within the European Union has reached a definitive stage. As the financial sector navigates the complexities of the mid-2020s, regulatory compliance and operational excellence are no longer optional for businesses seeking to leverage blockchain-based financial rails.

For crypto payment gateways based in the EU, such as INXY Payments, the verification workflow represents the first and most critical touchpoint in establishing a secure, bank-grade relationship with professional partners. This report provides an exhaustive analysis of the merchant verification process, grounded in the primary directives of the Markets in Crypto-Assets (MiCA) Regulation and the practical requirements of the Know Your Business (KYB) standards.

The Regulatory Landscape: MiCA, TFR, and DAC8

The "Regulatory Rubicon" has been crossed, shifting the focus of European authorities from drafting policy to aggressive enforcement. Central to this environment is the Markets in Crypto-Assets Regulation (MiCA), which has successfully harmonized the rules for digital assets across all 27 EU member states.

The verification process is now governed by three key frameworks:

MiCA Authorization: Eliminates the "Wild West" era, ensuring only fully authorized providers operate within the EEA.

Transfer of Funds Regulation (TFR): Enforces a "Zero Threshold" policy for the "Travel Rule," requiring detailed data on the originator and beneficiary for every transaction.

DAC8: Mandates strict tax reporting and the collection of Tax Identification Numbers (TINs) to ensure fiscal transparency.

Architecture of the Know Your Business (KYB) Process

Know Your Business (KYB) is the primary defensive mechanism used by fintech gateways. Unlike Know Your Customer (KYC), which focuses on individuals, KYB requires a deeper exploration of corporate hierarchies.

The Verification Objectives:

Legal Existence: Proving the business is a real, registered entity.

Control Disclosure: Identifying the Ultimate Beneficial Owners (UBOs) to prevent the use of shell companies for illicit activities.

Risk Scoring: Evaluating the industry, geography, and transaction profile of the merchant.

The INXY Payments Verification Workflow: A Step-by-Step Guide

The verification process is designed to be rigorous yet streamlined, ensuring all participants meet EU compliance standards. This is a unified process applicable to all merchants, regardless of their industry or integration method.

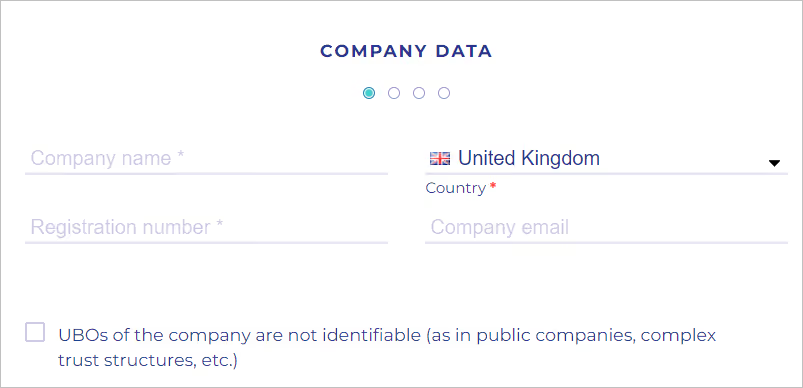

Step 1: Initial Company Data Intake

The process commences with the "Company data form." The merchant must enter fundamental identifying information, including the legal Company Name, official Registration Number, and Country of Registration.

Note: Providing a direct company email is recommended to ensure a clear line of communication with compliance officers.

Step 2: Comprehensive Documentation Upload

Merchants must validate their legal status by uploading a robust evidentiary file. Mandatory documents typically include:

Certificate of Incorporation / Business Registration: Proof that the entity exists in a government registry.

Articles of Association (AOA): Defines the entity's operations and leadership structure.

Operating License: Required only if the merchant operates in a specifically regulated sector (e.g., gambling, forex).

Identifying the natural persons who ultimately control the entity is the cornerstone of EU AML regulations.

The 25% Rule: Merchants must identify any natural person holding more than 25% of ownership shares or voting rights.

Verification: For each UBO, the system requires their full name, date of birth, and contact details. Identity verification can be performed live or via a secure link sent to the stakeholder.

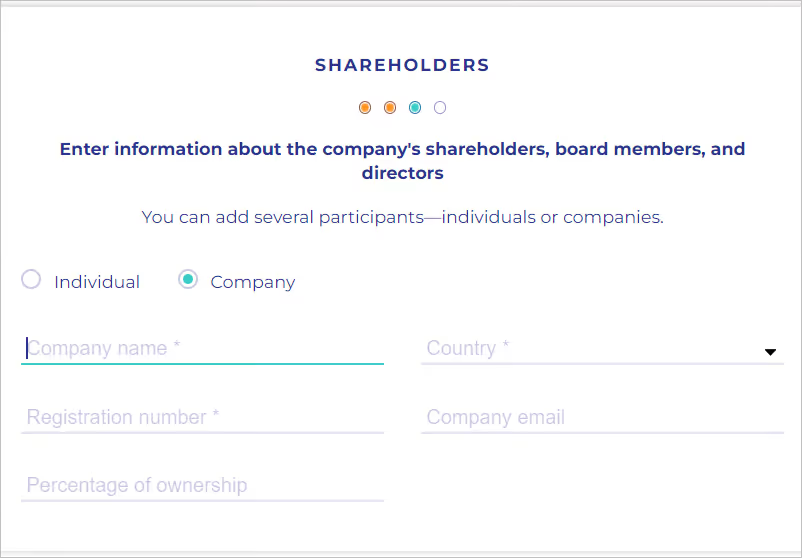

Step 4: Shareholder and Representative Verification

Corporate Shareholders: If a shareholder is another company, the merchant must provide that entity's Articles of Association and trace the ownership chain back to a natural person.

Legal Representative: Data must be provided for the person acting on behalf of the company, ensuring they have the legal authority (e.g., Director status or Power of Attorney) to open financial accounts.

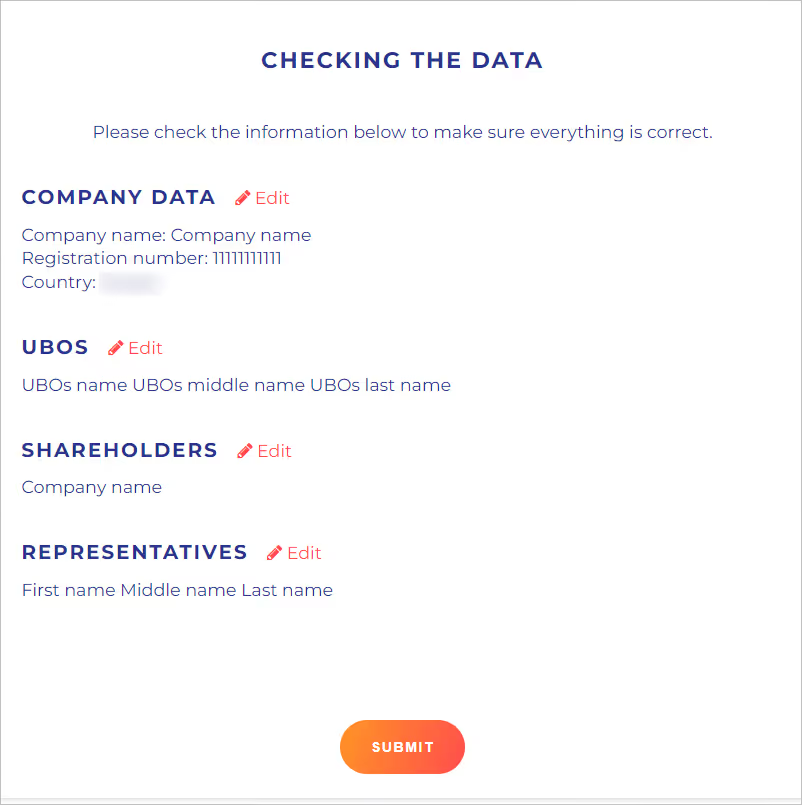

Step 5: Final Validation and Submission

The penultimate step is a thorough review of all provided data. Once confirmed, the application enters the compliance review queue. Thanks to automated systems, merchants can track their status in real-time via their dashboard.

Document Requirements and Authentication Standards

The integrity of the verification process relies entirely on the quality of the documentation. The European fintech environment maintains a high bar for validity.

Mandatory Conditions for Approval:

Language: All documents must be in English. If the original is in another language, a notarized translation is required.

Authentication: Documents must be "official," bearing the necessary stamps, signatures, or qualified electronic seals as per local laws.

Recency: Extracts from commercial registries generally should not be older than 3 months to ensure the data is current.

Common Reasons for Rejection:

Typos: Mismatches between the input form and the uploaded PDF.

Missing Pages: Uploading incomplete Articles of Association.

Low Quality: Blurry scans or photos where text is illegible.

Security and Data Protection (GDPR & DORA)

The sensitive nature of KYB data requires the highest levels of protection.

GDPR Compliance: Data is used solely for client identification and activity justification, adhering to the principle of "Purpose Limitation."

DORA (Digital Operational Resilience Act): Mandates that payment gateways demonstrate resilience against cyber threats. Data is encrypted at rest and in transit, with role-based access ensuring only authorized compliance personnel can view identity files.

Conclusion: Compliance as a Competitive Advantage

Completing the merchant verification process is more than a regulatory hurdle; it is a strategic move that positions a business as a credible player in the global economy. By adhering to this standardized verification workflow, merchants—whether they are hosting providers, e-commerce stores, or digital service agencies—secure a stable, bank-grade foundation for their financial operations.

In the mature crypto economy of 2026, a verified account is the key to unlocking global markets, ensuring seamless settlements, and protecting business capital from regulatory friction.

Gemini said Here is a concise blog summary optimized for readability and engagement, designed to pull readers into the full guide.

Blog Summary: Integrating Crypto via INXY for WHMCS In 2026, cryptocurrency has moved beyond speculation to become a primary "production" currency for global digital services. For hosting providers and agencies using WHMCS, the shift toward stablecoins—the "Internet’s dollar"—is a critical competitive advantage. This guide explores how to integrate the INXY Payment Gateway, a robust solution designed to bridge the gap between traditional billing and the modern crypto economy.

In 2026, the fintech landscape is shifting from speculation to production. For hosting providers, VPN services, and digital agencies using WHMCS, the question is no longer if you should accept cryptocurrency, but how efficiently you can do it. With stablecoins becoming the "Internet’s dollar" for cross-border flows, integrating a robust payment gateway is essential for maintaining a competitive edge in the EU and global markets.

One of the most seamless ways to bridge the gap between traditional billing and the crypto economy is through the INXY Payment Gateway. This guide provides a detailed walkthrough for setting up the INXY module on your WHMCS platform.

1. Why Crypto for WHMCS in 2026?

Integrating crypto payments into your billing system offers several strategic advantages:

Lower Fees: Traditional processors often charge 2–4% for international payments, while gateways like INXY provide more cost-effective alternatives.

Chargeback Protection: Blockchain transactions are immutable; once confirmed, they cannot be reversed by the sender, eliminating the administrative burden of fraudulent chargebacks.

Global Reach: Crypto allows you to accept payments from customers in regions with restrictive banking or unstable local currencies without multi-day delays.

2. System Requirements

Before installation, ensure your environment meets the following criteria for the INXY module (Version 1.0.3):

Location: Go to Merchant settings → API in the INXY dashboard and paste the URL.

5. Advanced Matching and Underpayment Rules

Crypto transactions can sometimes result in minor amount differences due to network fees. INXY handles this through the config.php file:

Amount Deviation: By default, the module accepts payments within 1% of the requested amount. For WHMCS, it is recommended to set 'amount_deviation_percentage' = 49 to reduce unnecessary top-up attempts and align with WHMCS's partial payment flow.

Time Window: Payments must arrive within 2 hours in production (30 minutes in Sandbox) to be automatically matched.

6. Summary of Payment Outcomes

Status

Customer Experience

WHMCS Admin Status

Paid in Full

Invoice shows "Paid".

Order marked as paid.

Overpaid

Extra amount added as credit.

Visible credit in account.

Partially Paid

"Awaiting payment" status.

Balance reduced by amount received.

Expired

"Expired" status on page.

Order remains unpaid.

By implementing INXY, you provide your users with a modern, 24/7 payment rail that settles in seconds, ensuring your hosting or digital business stays ahead of the curve in 2026.

Would you like me to draft a series of social media posts to announce your new crypto payment options to your customers?

Crypto Checkout That Converts: Reducing Drop-off on Stablecoin Payments

You added crypto checkout to win new buyers — but the payment page is quietly leaking them. This guide breaks down exactly where stablecoin payments lose customers: network confusion, price-lock anxiety, wallet friction, unclear confirmations, and surprise fees. Learn the design and infrastructure fixes that turn a leaky pay page into one that converts — including why a well-built crypto checkout can beat cards, clearing ~99.9% of attempts with no chargebacks.

You added a crypto checkout to capture a new segment of buyers, and the demand is real — but the payment page is leaking customers. A shopper picks crypto, lands on the pay screen, hesitates, and disappears. That gap between intent and completed payment is checkout drop-off, and on crypto rails it has its own specific causes that most teams never diagnose.

This guide breaks down where stablecoin payments lose customers, the friction points that drive abandonment, and the concrete design and infrastructure choices that turn a leaky pay page into one that converts. The goal is simple: every shopper who chooses crypto should finish paying.

Why crypto checkouts lose customers

A crypto checkout is not just a card form with different logos. It introduces steps a Web2 buyer has never seen — choosing a network, copying an address, waiting for confirmations — and every unfamiliar step is a place to quit. Unlike a card decline, which the customer understands, a stalled or confusing crypto payment feels risky, and risk kills conversion.

Where drop-off actually happens

Most teams treat the checkout as a single event. It isn't. Crypto payment drop-off clusters at four distinct stages:

Method selection — the customer considers crypto but doesn't trust it on your site, so they bounce before starting.

Network and asset choice — faced with "ERC20 / TRC20 / BEP20" they don't recognize, they freeze.

Wallet action — copying an address or scanning a QR code, switching apps, and fearing a mistake.

Confirmation wait — the payment is sent but the page gives no clear signal it worked.

You cannot fix abandonment you can't see. Instrument each of these stages separately before changing anything.

Why a one-point conversion gain is worth chasing

Checkout is the highest-leverage surface you own. Traffic, ads, and product pages all exist to deliver a customer to this screen. Recovering even a few percentage points of crypto payment conversion rate here costs nothing in additional traffic — it simply stops you paying for visitors you then lose at the last step. For a business processing meaningful volume, a high-conversion gateway is not a nice-to-have; it is the difference between crypto being a growth channel and a vanity feature.

The main causes of stablecoin payment drop-off

Network and asset confusion

The single biggest source of friction is choice the customer can't evaluate. Asking a non-technical buyer to select between Tron, Ethereum, BNB Chain, and Polygon — each with different fees and speeds — is asking them to make a decision they're unqualified to make. Hesitation becomes abandonment.

Volatility and price-lock anxiety

If the amount due appears to move while the customer reads it, they assume they'll overpay or underpay. Even with stablecoin payments, buyers worry the quote will expire or shift. Without a visibly locked rate, the page feels unsafe.

Wallet friction and manual errors

Copy the address. Switch to the wallet app. Paste. Check the network matches. Confirm the gas. Send. Switch back. Each handoff is a chance to abandon — and the fear of sending funds to the wrong address or wrong chain is enough to make cautious buyers stop entirely.

Slow or unclear confirmation

A customer who has paid but sees a spinning loader with no explanation assumes the worst. On-chain confirmation times vary by network, and a checkout that doesn't explain the wait — or sets no expectation for it — converts the final, already-committed moment into a drop-off. (For the underlying mechanics, see our guide on how long crypto withdrawals and confirmations take.)

Fees, minimums, and surprise costs

A network fee that appears only at the final step, or a minimum the customer trips over, reads as a bait-and-switch. Surprise costs at the moment of payment are one of the most reliable abandonment triggers in any checkout — crypto included.

Missing trust and compliance signals

Crypto still carries a perception of risk for mainstream buyers. A pay page with no licensing, security, or brand reassurance gives a nervous customer every reason to close the tab. Trust is not decoration here; it is a conversion input.

How to design a crypto checkout that converts

Invoice in fiat, settle in stablecoins

Let the customer see the price in the currency they think in — EUR or USD — and pay in crypto behind the scenes, with automatic conversion to stablecoins or fiat on your side. This removes mental math, neutralizes volatility, and lets a Web2 buyer treat the transaction like any other payment. It is the foundation of a converting crypto checkout.

Reduce choices and default to the right network

Don't make the customer a blockchain expert. Pre-select a fast, low-fee network as the default and present asset options in plain language ("Pay with USDT" rather than "TRC20"). Fewer decisions mean fewer exit points. Every option you remove from the critical path is a conversion you keep.

Lock the rate and show a countdown

Display a fixed amount due with a clear, time-boxed quote ("This price is locked for 15:00"). A visible countdown does two things at once: it removes price anxiety and creates gentle urgency that pulls the customer through. Certainty converts.

Make the confirmation state legible

Tell the customer exactly what's happening: "Payment detected — confirming on-chain. This usually takes under a minute." Replace ambiguous spinners with a status that names the step and sets a time expectation. The moment after a customer pays is the worst possible time to leave them guessing.

Add fallback paths

Some customers will start a crypto payment and stall. Offer a clean way to switch methods or retry without losing the cart. A dead-end on a failed or abandoned crypto payment is a guaranteed loss; a graceful fallback recovers a share of it.

Build trust into the page

Show licensing and security signals where the customer makes the decision. INXY operates as licensed and regulated payment infrastructure with AML/KYB controls and partners including Sumsub, Elliptic, and Crystal — the kind of compliance signal that reassures a cautious buyer at exactly the right moment. Surface it; don't bury it in a footer.

Conversion benchmarks: crypto vs cards

When the checkout is built well, crypto doesn't just match card conversion — it can beat it. The structural advantages are real:

Cards fail far more often than most merchants realize — declines, 3-D Secure friction, and cross-border blocks routinely cost 5–30% of attempts. Crypto settlement is final and irreversible, which removes chargebacks entirely and lets a well-designed gateway clear close to every legitimate attempt. For merchants serving Europe, Asia, and LatAm, that reliability is a direct conversion uplift — INXY reports helping customers increase conversion rates by up to 40%. (For a wider comparison of providers and rails, see best payment gateways for SaaS in 2026.)

A pre-launch checklist

Before you ship a crypto checkout, confirm it does all of the following:

Prices in the customer's fiat currency, with conversion handled automatically.

Defaults to a fast, low-fee network instead of forcing a choice.

Locks the rate with a visible countdown.

Shows total cost up front, including any network fee — no surprises at the last step.

Names the confirmation step and sets a time expectation.

Offers a retry or fallback for stalled payments.

Displays trust and compliance signals on the pay page itself.

Tracks drop-off by stage, not just overall completion.

How INXY reduces crypto checkout drop-off

INXY's high-conversion API paygate is built around the principles above. Customers are invoiced in fiat and pay in crypto, with automatic conversion to stablecoins or fiat to remove volatility risk. You get settled in your bank account — in EUR or USD — as soon as the next day, with full reporting and an accounting-friendly setup for Web2 companies. The gateway supports 20+ cryptocurrencies across major networks (ERC20, TRC20, BEP20, Polygon, Tron, TON, and more), charges below 1% per transaction with no setup or hidden fees, and is engineered for a ~99.9% success rate.

The result is a checkout your customers finish — built to convert, not just to accept. Add it to your checkout page, webstore, platform, or app via API integration, or book a demo to see the conversion data for your business model.

FAQ

What causes drop-off on crypto checkouts? The most common causes are network and asset confusion, price-lock anxiety, manual wallet friction, unclear confirmation states, surprise fees, and missing trust signals. Each maps to a specific stage of the checkout, so the fix starts with measuring drop-off stage by stage rather than as a single number.

How do stablecoin payments improve checkout conversion? Stablecoins remove volatility from the transaction, so the amount due stays fixed while the customer pays. Pairing that with fiat-denominated pricing and automatic conversion lets a mainstream buyer complete a crypto payment as easily as a card payment — without exposure to price swings.

Is crypto checkout conversion really higher than cards? It can be. Crypto payments have no chargebacks and final settlement, and a well-built gateway can clear close to 99.9% of legitimate attempts versus 70–95% typical card success. The advantage is largest for cross-border and emerging-market customers, where cards are frequently declined or restricted.

Which network should a crypto checkout default to? Default to a fast, low-fee network so customers don't have to choose. Stablecoins on high-throughput networks settle in seconds for a fraction of the cost of slower chains, which both speeds confirmation and reduces the fee shown at checkout.

How do I add a high-conversion crypto checkout to my site? Use a payment gateway with API integration that handles fiat pricing, network selection, rate locking, and conversion for you. INXY integrates with your existing checkout, webstore, or app, and settles to your bank in EUR or USD — see get started.