The institutionalization of the digital asset economy within the European Union has reached a definitive stage. As the financial sector navigates the complexities of the mid-2020s, regulatory compliance and operational excellence are no longer optional for businesses seeking to leverage blockchain-based financial rails.

For crypto payment gateways based in the EU, such as INXY Payments, the verification workflow represents the first and most critical touchpoint in establishing a secure, bank-grade relationship with professional partners. This report provides an exhaustive analysis of the merchant verification process, grounded in the primary directives of the Markets in Crypto-Assets (MiCA) Regulation and the practical requirements of the Know Your Business (KYB) standards.

The Regulatory Landscape: MiCA, TFR, and DAC8

The "Regulatory Rubicon" has been crossed, shifting the focus of European authorities from drafting policy to aggressive enforcement. Central to this environment is the Markets in Crypto-Assets Regulation (MiCA), which has successfully harmonized the rules for digital assets across all 27 EU member states.

The verification process is now governed by three key frameworks:

MiCA Authorization: Eliminates the "Wild West" era, ensuring only fully authorized providers operate within the EEA.

Transfer of Funds Regulation (TFR): Enforces a "Zero Threshold" policy for the "Travel Rule," requiring detailed data on the originator and beneficiary for every transaction.

DAC8: Mandates strict tax reporting and the collection of Tax Identification Numbers (TINs) to ensure fiscal transparency.

Architecture of the Know Your Business (KYB) Process

Know Your Business (KYB) is the primary defensive mechanism used by fintech gateways. Unlike Know Your Customer (KYC), which focuses on individuals, KYB requires a deeper exploration of corporate hierarchies.

The Verification Objectives:

Legal Existence: Proving the business is a real, registered entity.

Control Disclosure: Identifying the Ultimate Beneficial Owners (UBOs) to prevent the use of shell companies for illicit activities.

Risk Scoring: Evaluating the industry, geography, and transaction profile of the merchant.

The INXY Payments Verification Workflow: A Step-by-Step Guide

The verification process is designed to be rigorous yet streamlined, ensuring all participants meet EU compliance standards. This is a unified process applicable to all merchants, regardless of their industry or integration method.

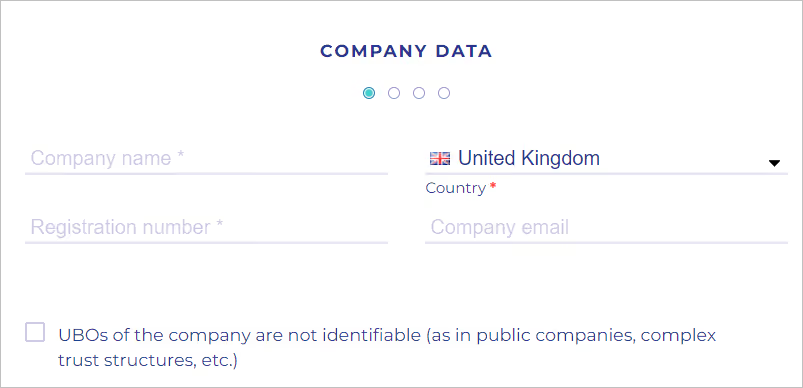

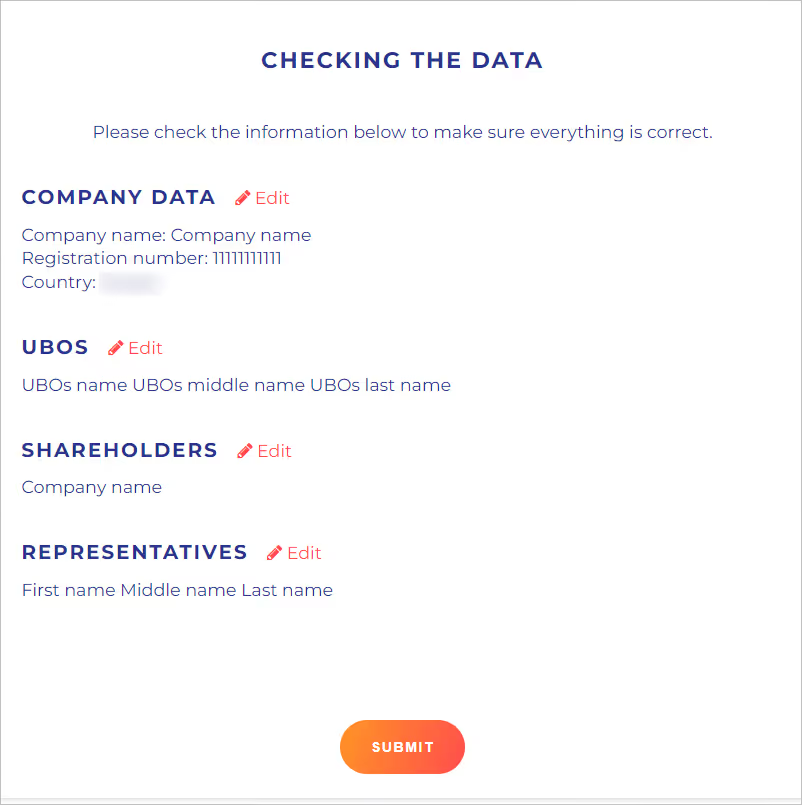

Step 1: Initial Company Data Intake

The process commences with the "Company data form." The merchant must enter fundamental identifying information, including the legal Company Name, official Registration Number, and Country of Registration.

Note: Providing a direct company email is recommended to ensure a clear line of communication with compliance officers.

Step 2: Comprehensive Documentation Upload

Merchants must validate their legal status by uploading a robust evidentiary file. Mandatory documents typically include:

Certificate of Incorporation / Business Registration: Proof that the entity exists in a government registry.

Articles of Association (AOA): Defines the entity's operations and leadership structure.

Operating License: Required only if the merchant operates in a specifically regulated sector (e.g., gambling, forex).

Identifying the natural persons who ultimately control the entity is the cornerstone of EU AML regulations.

The 25% Rule: Merchants must identify any natural person holding more than 25% of ownership shares or voting rights.

Verification: For each UBO, the system requires their full name, date of birth, and contact details. Identity verification can be performed live or via a secure link sent to the stakeholder.

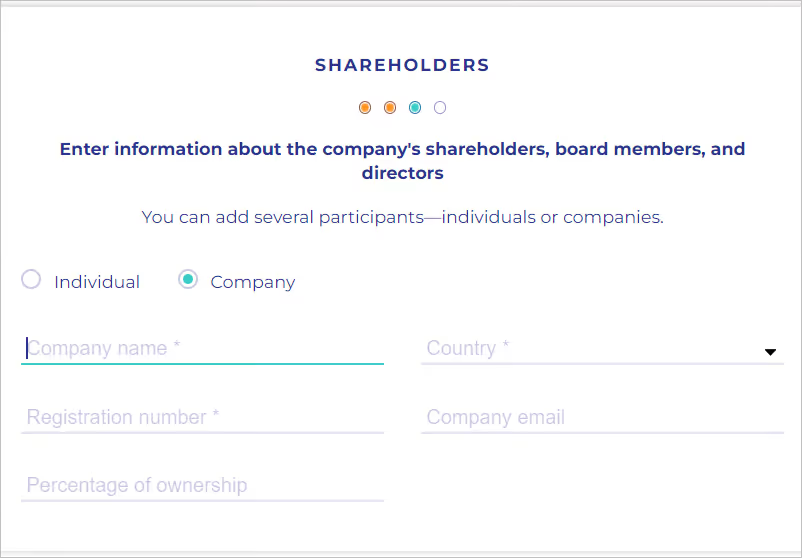

Step 4: Shareholder and Representative Verification

Corporate Shareholders: If a shareholder is another company, the merchant must provide that entity's Articles of Association and trace the ownership chain back to a natural person.

Legal Representative: Data must be provided for the person acting on behalf of the company, ensuring they have the legal authority (e.g., Director status or Power of Attorney) to open financial accounts.

Step 5: Final Validation and Submission

The penultimate step is a thorough review of all provided data. Once confirmed, the application enters the compliance review queue. Thanks to automated systems, merchants can track their status in real-time via their dashboard.

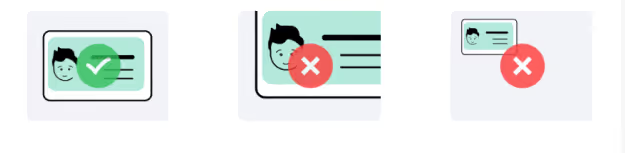

Document Requirements and Authentication Standards

The integrity of the verification process relies entirely on the quality of the documentation. The European fintech environment maintains a high bar for validity.

Mandatory Conditions for Approval:

Language: All documents must be in English. If the original is in another language, a notarized translation is required.

Authentication: Documents must be "official," bearing the necessary stamps, signatures, or qualified electronic seals as per local laws.

Recency: Extracts from commercial registries generally should not be older than 3 months to ensure the data is current.

Common Reasons for Rejection:

Typos: Mismatches between the input form and the uploaded PDF.

Missing Pages: Uploading incomplete Articles of Association.

Low Quality: Blurry scans or photos where text is illegible.

Security and Data Protection (GDPR & DORA)

The sensitive nature of KYB data requires the highest levels of protection.

GDPR Compliance: Data is used solely for client identification and activity justification, adhering to the principle of "Purpose Limitation."

DORA (Digital Operational Resilience Act): Mandates that payment gateways demonstrate resilience against cyber threats. Data is encrypted at rest and in transit, with role-based access ensuring only authorized compliance personnel can view identity files.

Conclusion: Compliance as a Competitive Advantage

Completing the merchant verification process is more than a regulatory hurdle; it is a strategic move that positions a business as a credible player in the global economy. By adhering to this standardized verification workflow, merchants—whether they are hosting providers, e-commerce stores, or digital service agencies—secure a stable, bank-grade foundation for their financial operations.

In the mature crypto economy of 2026, a verified account is the key to unlocking global markets, ensuring seamless settlements, and protecting business capital from regulatory friction.

In recent years, cryptocurrency has taken center stage in the world of finance. Back in the day, only tech enthusiasts and a few daring investors dabbled in it. Fast forward to 2026, and getting paid in crypto has become a norm for many. With the rise of Bitcoin (BTC), Tether (USDT), and USD Coin (USDC), businesses and freelancers have more options than ever.

Why this shift? Traditional banks can be slow and expensive for international transactions. Crypto payments solve this by being faster and often cheaper. Imagine a freelancer in India working for a company in the US. With crypto, they can receive their payment in minutes rather than days.

Platforms that support crypto payments have also grown. These platforms help businesses pay employees in digital currencies, making the process smooth. More companies see the potential in crypto payroll, offering it as a payment option. As this trend continues, getting paid in crypto could become as common as using a credit card.

Understanding USDT, USDC, and BTC

Let's dive into the world of crypto, especially USDT, USDC, and BTC. These three are top players in the cryptocurrency arena. USDT and USDC are what's known as stablecoins. This means their value is tied to the dollar. So, if you're dealing with USDT or USDC, you're looking at a stable value, usually one dollar. This makes them great for transactions, as you avoid big price swings.

BTC, or Bitcoin, is a bit different. It’s the first and most famous cryptocurrency. Unlike stablecoins, Bitcoin's value can change a lot. It’s often seen as digital gold. Why? Because people use it to store value over time.

Imagine you’re sending money to a friend abroad. Using USDT or USDC might be your choice for a stable transaction. But if you're investing for the future, Bitcoin could be more appealing. Each has its own use, and knowing these differences helps you choose the right one.

Choosing the Right Crypto Payment Platform

Picking a crypto payment platform is a bit like choosing a new phone. You want something reliable, easy to use, and packed with features. Let's look at some key things to consider.

First, security is crucial. Look for platforms with strong protection like two-factor authentication. This keeps your funds safe from hackers. Platforms like Coinbase and Binance have solid security measures, making them popular choices.

Next, think about the currencies you need. Some platforms support only a few, while others have a broader range. If you want to get paid in USDT, USDC, or BTC, ensure the platform you choose supports these.

Transaction fees are another point to consider. Some platforms charge more than others. Compare fees to avoid surprises later. Lower fees can mean more money in your pocket.

User experience is important too. A simple and clean interface makes transactions easier. Platforms with good customer support can also be a lifesaver if you encounter problems.

Lastly, check for any extra features. Some platforms offer benefits like staking or lending options. These can give you more ways to earn from your crypto.

Choosing the right platform takes a bit of research, but it's worth it for a smooth experience.

Setting Up Your Crypto Wallet

Getting paid in crypto means you'll need a wallet to store your digital coins. Think of a crypto wallet as your virtual bank account. It's where you keep your crypto earnings safe and sound. Let's break down the process of setting up your own crypto wallet.

First, you'll need to choose the type of wallet that suits your needs. There are two main types: hot wallets and cold wallets. Hot wallets are connected to the internet. They're like the apps on your phone or computer. They're easy to use and perfect for quick transactions. Examples include Trust Wallet or MetaMask. Cold wallets, on the other hand, are offline. They're secure and ideal for storing large amounts of crypto. Picture them as USB sticks that hold your digital currency. Popular cold wallets include Ledger Nano and Trezor.

When choosing a cold wallet, it's exciting to see the latest tech. For example, the new Trezor Safe 7 features a state-of-the-art 7th generation secure chip and even includes protection against future quantum computer threats. Other brands are rethinking the design entirely. Take Tangem—it uses a set of sleek cards with a high-security 6th generation chip. A major plus is that it removes the stressful "seed phrase" you have to write down and keep safe. Instead, you can restore access using your backup cards. (Note: it works with your phone via NFC to make transactions).

Once you've decided on the type, it's time to set it up. If you go with a hot wallet, download the app or software from a trusted source. Be careful of fake sites or apps. They can trick you into giving away your crypto. After downloading, follow the setup instructions. You'll likely be asked to create a username and password. Keep this information safe and private.

In the case of a cold wallet, you'll purchase the device from a reputable store. When it arrives, connect it to your computer and follow the instructions. You'll be guided to set up a PIN and, for most models, a recovery phrase. This recovery phrase is crucial. It's a set of random words that help you recover your wallet if it's lost or stolen. Write them down on paper and store them in a secure place. (Remember, wallets like Tangem offer a different, card-based recovery method).

Next, you need to fund your wallet. To get paid in crypto, share your wallet address with your employer or client. This address is like your bank account number. It's a long string of letters and numbers. Ensure you share the correct address for the specific crypto you're using, like USDT, USDC, or BTC.

Finally, always keep your wallet updated. Developers often release updates to improve security and add features. Regularly backing up your wallet (whether it's your seed phrase or backup cards) is a good habit too. It protects your funds against potential losses.

Setting up a crypto wallet might seem tricky. But with careful steps and modern options that boost both security and convenience, you can have a secure place for your crypto payments.

Integrating Crypto Payroll for Businesses

In 2026, more businesses are looking at crypto payroll as a smart move. Paying employees with digital currencies like BTC, USDT, and USDC is no longer a novelty. It's becoming common. But how does one actually integrate crypto payroll into a business? Let's break it down.

First, you need a solid crypto payment platform. These platforms act as the backbone for crypto payroll. They manage transactions and convert fiat to crypto or vice versa. Popular platforms offer easy setup and user-friendly interfaces. They let you automate payments, ensuring timely salaries in digital currency. Crucially, the right platform handles the complex "blockchain plumbing" for you:

Gas Management: Gas fees vary by network and can cause payments to fail. Your platform should automatically calculate optimal fees and adjust during network congestion so transactions go through without manual intervention.

Error Handling: Don't rely on systems that fail silently. Choose a provider that actively monitors transactions and automatically retries failed payments, offering features like gas refunds for failures to reduce payout issues.

Auto-Conversion: Accepting crypto is only half the solution. Look for infrastructure that supports automatic conversion of received crypto into your preferred settlement currency (like fiat or a stablecoin) at the point of receipt. This ensures operational efficiency and minimizes FX risk for your business.

Legal compliance is crucial. It's important to check local laws regarding crypto payroll. Some regions have specific regulations. For instance, tax implications might differ from traditional payroll systems. Consulting a financial advisor who understands crypto can be a wise step.

Choosing the right digital wallet is vital. A secure wallet ensures your funds are safe. There are software wallets for ease of access and hardware wallets for added security. Businesses often use multiple wallets for different purposes, like one for daily transactions and another for savings.

Employee education is the next step. Not all employees may be familiar with crypto. Offering training sessions can help them understand how to use digital wallets and the benefits of receiving crypto payments. This can increase their confidence and acceptance of this new payment method.

Lastly, consider transaction fees. Crypto transactions can incur fees, which vary between currencies and platforms. It's smart to compare rates and choose the most cost-effective option for your business. This helps in maintaining a budget-friendly payroll system while embracing the future of finance. A robust platform simplifies this by providing clear fee structures and handling the variable costs of gas and conversions automatically.

Tax Implications of Getting Paid in Crypto

Getting paid in crypto might sound exciting, but it's important to think about taxes. Just like regular money, crypto is subject to tax rules. These rules can change based on where you live, so it's good to check with local tax authorities.

When you receive crypto as payment, it's often seen as income. This means you'll pay tax on the value of the crypto at the time you get it. If your employer pays you in crypto, they might report this to tax authorities just like they would with regular salaries.

If you sell your crypto later, you might have to pay more taxes. This is called capital gains tax. The gain is the difference between what you sold it for and what it was worth when you got it. For example, if you receive Bitcoin worth $500 today and sell it later for $700, you might pay tax on the $200 gain.

Countries have different rules for crypto taxes. In the U.S., for example, the IRS treats crypto as property. This means you might need to keep records of transactions to report during tax season. Some countries might have more relaxed rules, while others could be stricter.

Modern payment platforms help solve these complexities by offering the ability to legally accept, send, and exchange cryptocurrencies just like regular money, while minimizing your tax and accounting burden. For example, you can use a system where you receive fiat directly—with no need to personally hold crypto assets. This approach significantly reduces volatility risk, compliance complexity, and operational friction.

There are tools to help you manage crypto taxes. Some platforms track transactions and provide reports. This can make it easier to understand what you owe. It's also useful to consult with a tax professional who knows about crypto to avoid mistakes.

Crypto taxes can seem tricky, but understanding the basics can help you stay on track. Keep records of your transactions and check local laws to ensure you're complying with tax requirements.

The Future of Crypto Payments

The world of crypto payments is evolving rapidly. By 2026, we can expect to see more businesses and individuals using cryptocurrencies like USDT, USDC, and BTC for everyday transactions. One reason for this growth is the increasing trust in blockchain technology. As more people understand how it works, they feel more comfortable using it. This trust is a big factor in making crypto payments more popular.

Many companies are already exploring how to make crypto payments easier. Some are developing platforms that allow users to pay with crypto just as easily as with cash or credit cards. These platforms are designed to be user-friendly, so even those new to crypto can use them without any trouble. For instance, some platforms are focusing on seamless integration with existing payment systems. This means you can use your favorite crypto wallet to make payments at stores that accept crypto.

Another trend we're seeing is the rise of stablecoins like USDT and USDC. These coins are tied to traditional currencies, so their value remains stable. This stability makes them attractive for everyday use, as people don't have to worry about sudden price changes. As a result, more businesses and consumers are choosing stablecoins for transactions.

Regulations are also playing a crucial role in shaping the future of crypto payments. Governments around the world are working to create laws that protect users and encourage innovation. These regulations help create a safe environment for people to use crypto without fear of scams or fraud.

Finally, the future of crypto payments will likely involve new technologies. Innovations like smart contracts and decentralized finance are already changing the way payments are processed. These technologies make transactions faster, cheaper, and more secure. As they become more widespread, they will make crypto payments even more appealing.

The future of crypto payments looks bright. With trust in blockchain growing, user-friendly platforms emerging, stablecoins gaining popularity, supportive regulations, and new technologies on the horizon, it's clear that cryptocurrencies will play an important role in the global economy.

FAQ

What are the benefits of getting paid in cryptocurrencies like USDT, USDC, and BTC?

Cryptocurrencies like USDT, USDC, and BTC offer benefits such as faster transaction times, lower fees, and increased global access. They also provide a hedge against local currency inflation and can be easily converted into other assets.

How do USDT, USDC, and BTC differ in terms of payment?

USDT and USDC are stablecoins, meaning they are pegged to the US dollar, making them less volatile and ideal for stable transactions. BTC is more volatile, which can be a benefit for potential gains but also carries more risk.

What should I consider when choosing a crypto payment platform?

When choosing a crypto payment platform, consider factors like security features, transaction fees, supported cryptocurrencies, user interface, and customer support. Research and compare reviews to find a platform that aligns with your needs.

How do I set up a crypto wallet to receive payments?

To set up a crypto wallet, choose a wallet type (hardware, software, or web-based), download the app or software, create an account, and securely store your private keys and recovery phrase. Follow the wallet’s specific setup instructions to ensure security.

Can businesses easily integrate crypto payroll systems?

Yes, businesses can integrate crypto payroll systems by partnering with specialized service providers that offer seamless integration with existing payroll systems. These services handle the conversion and distribution of fiat to cryptocurrency.

Are there tax implications for receiving income in crypto?

Yes, receiving income in crypto is subject to tax regulations in most jurisdictions. You must report crypto earnings as income, and it may be treated as capital gains when converted to fiat currency. Consult a tax professional for specific guidance.

What does the future hold for crypto payments by 2026?

By 2026, crypto payments are expected to become more mainstream, with increased adoption by businesses and individuals. Advances in blockchain technology and regulatory clarity may lead to more secure and efficient payment systems, further integrating cryptocurrencies into the global economy.

The end of fiat friction: Why strategic merchants are switching to stablecoin payments

To accept crypto once meant exposure to price volatility. That is no longer the case. Stablecoins — pegged to the US Dollar or Euro — deliver the settlement efficiency of blockchain without the speculation. For C-level executives, the question is no longer whether to integrate digital assets, but how quickly legacy bottlenecks can be replaced with purpose-built infrastructure.

The legacy financial system imposes a structural tax on growth. For decades, merchants have absorbed correspondent banking fees, 3% interchange costs, and chargeback losses that erode margin on every transaction. In a global economy, waiting T+3 or T+5 for settlement is not an inconvenience — it is a liquidity problem.

To accept crypto once meant exposure to price volatility. That is no longer the case. Stablecoins — pegged to the US Dollar or Euro — deliver the settlement efficiency of blockchain without the speculation. For C-level executives, the question is no longer whether to integrate digital assets, but how quickly legacy bottlenecks can be replaced with purpose-built infrastructure.

1. Settlement velocity: From days to seconds

Traditional cross-border settlements move through a chain of intermediate banks, accumulating fees and losing transparency at every hop. SWIFT provides no real-time visibility into where funds are or when they will arrive.

Stablecoins operate on a 24/7/365 ledger with near-instant finality. Settling on Ethereum, Polygon, or TRON, merchants are no longer bound by banking hours or cut-off windows. Capital lands, clears, and is available for redeployment immediately — not in a pending queue.

inxy.io integrates directly into this settlement layer, giving merchants the operational continuity that traditional finance structurally cannot offer.

2. Eliminating the chargeback tax

Chargeback fraud costs merchants billions annually. Credit card networks are centralised by design, which means any transaction can be reversed — often at the merchant's expense, with little recourse.

Blockchain transactions are push-based and immutable. When a business chooses to accept crypto in the form of stablecoins, payment finality is guaranteed by the protocol, not by a bank's dispute resolution team.

No chargebacks: Once confirmed on-chain, a transaction cannot be reversed by a third party.

Reduced fraud overhead: No need for aggressive fraud filters that block legitimate customers.

Revenue sovereignty: You control your income stream without intermediary intervention.

3. Technical infrastructure: Beyond the hype

A payment gateway needs to be a piece of production-grade fintech infrastructure, not just a wallet interface. High-volume merchants require an API that abstracts blockchain complexity without sacrificing control.

What inxy.io provides:

No crypto management overhead: Merchants do not handle tokens or gas fees. That layer is abstracted entirely.

Volatility protection: Pay-ins convert to stablecoins or fiat instantly, locking in value at the moment of transaction.

Multi-chain support: USDT, USDC, DAI, EURC, TON, BTC, ETH, LTC, TRX, BNB, DOGE across ERC-20, TRC-20, Polygon, and BSC — customers transact on the network that works best for them.

Real-time webhooks: Instant payment status notifications to your backend, enabling automated fulfilment or shipping triggers without polling.

Compliance stack: EU VASP (Poland), Canadian MSB, MiCA-ready, AML/KYT/KYC, sanctions screening via Elliptic and Sumsub, Big-4-friendly fiat reporting.

4. Drastic reduction in operational costs

Managing global payments typically means maintaining multiple local currency accounts and navigating FX spreads on every cross-border transfer. Stablecoins provide a single settlement layer that works across jurisdictions without currency conversion overhead.

Consolidating payment rails through inxy.io can reduce payment processing Opex by up to 80%. Instead of paying a chain of intermediaries for the movement of value, you pay for efficient infrastructure. That margin stays in the business.

FAQ: Navigating the stablecoin shift

Is it difficult to integrate a stablecoin gateway into an existing platform?

No. inxy.io integrates via a REST API or pre-built plugins for major e-commerce engines. Documentation and technical support are included, and most teams go live faster than a standard merchant bank account setup.

How do we handle gas fee volatility?

inxy.io routes transactions through high-throughput networks to keep fees minimal. Customers can select the most cost-effective network for their transaction — the infrastructure handles the routing logic.

How does accepting stablecoins affect our accounting?

USDT and USDC are pegged 1:1 to the dollar, which makes them materially simpler to account for than traditional cryptocurrencies. inxy.io provides detailed reporting and CSV exports compatible with standard accounting software and ERP systems.

What about regulatory compliance?

inxy.io is built with compliance as a core component, not an afterthought — EU VASP registration, MiCA readiness, AML/KYT screening, and Big-4-auditable reporting. Your business stays within the regulatory framework while operating at full velocity.

Scalability Without Compromise

The merchant of 2026 cannot run on 1970s banking rails. The competitive advantage belongs to businesses that eliminate payment friction and capture the full value of their transactions across borders.

inxy.io is the infrastructure layer for that transition — robust APIs, multi-chain settlement, and a compliance stack built for global scale.

Partner with INXY — secure your payment infrastructure and lead the market.

How to Integrate Crypto Payments into Your Business: A Practical Guide

Adding a crypto payment gateway to your business can open new doors. It lets you accept crypto payments from customers worldwide, bringing faster transactions, lower fees, and no chargebacks. But it’s not as simple as flipping a switch. To truly make crypto work for your business, there’s a list of things you need to get right.

Adding a crypto payment gateway to your business can open new doors. It lets you accept crypto payments from customers worldwide, bringing faster transactions, lower fees, and no chargebacks. But it’s not as simple as flipping a switch. To truly make crypto work for your business, there’s a list of things you need to get right.

Set Up a Digital Wallet

A wallet is where digital assets are stored. For daily operations, software wallets can be enough. But for larger amounts, businesses usually choose hardware wallets for added security.

Choose and Integrate a Payment Solution

You'll need a payment gateway that supports digital currencies. This might be a plugin for your e-commerce platform or a custom API integration. The goal is to make payment easy for customers and seamless for your team.

Handle Pricing and Exchange Rates

Decide how to display prices-directly in digital currency or by converting from your local currency at the moment of purchase. Make sure exchange rates are transparent for your customers.

Manage Volatility

Digital currencies are known for price swings. Have a strategy for dealing with this, such as converting to stablecoins or fiat currency immediately after payment.

Monitor Transaction Fees

Network fees can change depending on demand. Regularly review these costs to ensure they remain acceptable for your business.

Stay Compliant

Digital payments are subject to different rules in different regions. Make sure you understand your obligations around KYC (Know Your Customer), AML (Anti-Money Laundering), and other regulatory requirements.

Educate Your Team

Everyone involved should know how the system works-especially your customer service team, who may need to help customers with payment questions.

Communicate with Customers

Let your customers know that you now accept digital payments. Add clear messaging across your website, marketing materials, and checkout flow.

Test Before Launching

Run test payments to ensure the process is smooth from start to finish. This helps catch any issues before customers experience them.

Strengthen Security

Security is a top priority. Use strong authentication, multi-signature wallets, and cold storage for long-term holdings. Keep your security protocols updated.

Set Up Accounting Processes

Track every transaction carefully. Many tax authorities require detailed reporting of digital currency transactions, and having a solid system in place is essential.

Prepare Customer Support

Expect questions and occasional payment issues. Make it easy for customers to contact you and resolve problems quickly.

Stay Informed

The digital payments landscape evolves rapidly. Keep an eye on regulatory changes, new technologies, and market trends to stay ahead.

Get Tax Advice

Digital currency can create tax liabilities. Consult a tax advisor who understands how digital payments are handled in your jurisdiction.

Review and Optimize

Regularly review how digital payments are working for your business. Gather customer feedback and monitor performance to make improvements as needed.

How INXY Payments Supports These Steps

At INXY Payments, we've built our platform to address all these challenges in one place. Our service is designed for businesses that want to add digital currency payments with minimal friction and maximum compliance. Here's how we help:

Auto-conversion: Incoming payments can be automatically converted to stablecoins or fiat currency to minimize volatility.

Full Compliance: Our platform is fully compliant with MiCA and other EU regulations, with built-in tools for KYC and AML checks.

Seamless Integration: Whether you use the API or our dashboard, setup is simple and fast.

No Wallet Management: You don't need to create and maintain wallets on different blockchains or hold extra coins to pay network fees-we handle that for you.

Custom Reports: We provide detailed, customized reports to simplify your accounting and tax filing.

Security First: Advanced security features protect your funds at every step.

Global Reach: We support payments worldwide and work across multiple industries.

Expert Support: Our team offers personalized onboarding and ongoing assistance, including tax consultations and compliance help.

Always Up-to-Date: We stay on top of blockchain updates and new infrastructure developments, so you don't have to worry about keeping up with tech changes.

Whether you want to accept bitcoin payments, send mass payouts in crypto, or add a seamless crypto billing option to your service, we've got you covered.