Navigating Crypto Compliance for Fintechs: How to Offer Stablecoins Safely

Imagine launching a killer feature that multiplies your transaction volume overnight, only to have regulators freeze your operations a week later. Welcome to the high-stakes reality of integrating stablecoins into your platform. Right now, digital dollars are powering the global economy, moving billions across borders daily. Your users are demanding it, and the business case for instant settlements is undeniable.

But there is a catch. Financial watchdogs globally are circling. Offering stablecoins is a massive growth lever for ambitious fintechs, but stepping into the crypto arena without an airtight compliance strategy is like walking a tightrope without a net. The ultimate challenge is navigating this regulatory minefield without sacrificing the seamless user experience your customers expect.

The Top Three: USDT, USDC, and DAI

Before diving into regulatory complexities, it is crucial to understand the stablecoin hierarchy and why diversifying your asset offerings is mandatory for compliance.

Tether (USDT): While it currently holds the number one spot for global trading volume, USDT faces severe regulatory headwinds. Notably, the European Union has implemented strict restrictions and effective bans on USDT exchanges under new frameworks, forcing fintechs to rethink relying on a single asset.

USD Coin (USDC): Sitting comfortably as the second most popular stablecoin, USDC is the gold standard for institutional compliance. It is a fully collateralized asset, genuinely backed 1:1 by actual US dollars and short-term assets, providing unparalleled transparency for strict regulators.

DAI: Holding the third position globally, DAI offers a robust, decentralized alternative that maintains its peg through smart contracts and over-collateralization, rounding out the essential stablecoins for any modern financial platform.

Key Regulatory Challenges in the Crypto Landscape

Offering stablecoins is not as simple as plugging into an API. Financial authorities are rapidly tightening their grip to prevent money laundering and systemic economic risks. First, stringent Know Your Customer (KYC) and Anti-Money Laundering (AML) directives require dynamic, ongoing monitoring. Second, the FATF Travel Rule mandates that institutions must securely share originator and beneficiary data for crypto transfers exceeding specific thresholds.

Finally, jurisdictional fragmentation creates a massive headache. The EU’s Markets in Crypto-Assets (MiCA) regulation perfectly exemplifies this, creating strict new rulebooks that directly restrict non-compliant stablecoins like USDT. This makes offering fully backed, transparent assets like USDC an absolute necessity for European operations.

Proven Strategies to Offer Stablecoins Compliantly

To protect your business from crippling fines while maximizing the incredible benefits of digital assets, you must follow these proven operational strategies:

Diversify Your Assets: Do not rely solely on USDT. Offer USDC to satisfy strict regulatory requirements in the EU, and provide DAI for users seeking decentralized options.

Implement Bank-Grade KYC/AML: Utilize automated identity verification systems that check users against global sanctions watchlists in real-time.

Integrate Transaction Monitoring: Deploy sophisticated blockchain analytics tools to trace wallets, ensuring incoming funds are not linked to illicit activities.

Geofence Restricted Jurisdictions: Utilize precise IP tracking to block specific stablecoin features in regions where they are explicitly banned or heavily restricted.

INXY as the Premier Crypto Payment Gateway Partner

Navigating this tangled web of regulations demands the right underlying technological infrastructure. This is where INXY steps in as the premier partner for fintech companies looking to integrate digital assets securely.

As a dedicated cryptocurrency payment gateway, INXY understands the exact pain points fintechs face. Most importantly, INXY natively supports all three of the top stablecoins: USDT, USDC, and DAI. Whether you need a reliable gateway to process fully backed USDC deposits in the heavily regulated EU market or high-speed APIs for global USDT and DAI transfers, INXY provides the robust backbone your application needs to scale while maintaining strict operational compliance.

Conclusion

The future of global payments is strictly digital, and stablecoins are leading the charge. While the fragmented regulatory environment is complex, it should not deter your business from innovating. By prioritizing proactive compliance, diversifying your asset offerings, and choosing the right technological allies, you can confidently offer secure stablecoin services to your users.

Ready to future-proof your financial platform? Discover how we can help you scale your operations compliantly by visiting https://www.inxy.io/fintech today.

Why gaming platforms are switching to crypto paygates

Traditional payment processors expose gaming studios to crippling chargeback fraud and high fees on micro-transactions. This guide explores why top developers are rapidly switching to cryptocurrency payment gateways to secure irreversible transactions, completely eliminate "friendly fraud," and unlock a massive global market of unbanked players.

What if you are pouring years of development into a highly anticipated multiplayer game. Launch day arrives, your cosmetic shop is generating thousands of micro-transactions, and your dashboard shows record-breaking revenue. But thirty days later, the reality check hits: a massive wave of credit card chargebacks. Players who bought digital skins are falsely claiming the transactions were unauthorized. Suddenly, your payment processor hits you with steep penalty fees, turning your profitable launch into a financial sinkhole. Welcome to the dark side of traditional gaming monetization.

For modern studios, relying exclusively on legacy fiat networks means accepting an uncontrollable financial risk. To protect revenue, eliminate fraud, and unlock a truly global player base, the gaming industry is rapidly pivoting. Integrating a cryptocurrency payment gateway is no longer just a Web3 novelty; it is the ultimate cheat code for secure, unstoppable game monetization.

The Nightmare of friendly fraud in gaming

Unlike physical e-commerce, digital goods exist in a complex regulatory gray area. When a gamer issues a chargeback through their bank, the studio faces an incredibly steep uphill battle. Proving a specific user legitimately consumed virtual currency or activated a battle pass is difficult, and traditional banks almost universally side with the consumer.

This phenomenon, known as "friendly fraud," forces developers to suffer a double loss: the digital asset is gone, the original revenue is reversed, and the payment processor slaps the studio with a heavy penalty fee. If your chargeback ratio exceeds a strict threshold, processors will classify your game as high-risk, leading to frozen funds or suspended accounts.

Unlocking the global unbanked market

Beyond fraud protection, traditional banking rails actively restrict your total addressable market. Some of the most explosive growth in the gaming sector is happening in emerging regions like Southeast Asia and Latin America. However, millions of passionate gamers in these areas lack access to standard international credit cards or are burdened by exorbitant foreign exchange fees.

By restricting in-game purchases to fiat currencies, studios are leaving massive amounts of money on the table. Cryptocurrency transcends physical borders. It allows anyone with an internet connection to participate in your game's digital economy, transforming previously unbanked players into high-value, paying customers.

The core advantages of a crypto checkout

Transitioning your game's monetization model to include digital assets provides immediate, measurable benefits for your bottom line. Top studios are making the switch to crypto gateways for several critical reasons:

Zero Chargeback Risk: Blockchain transactions are mathematically irreversible. Once a player pays with crypto, the funds are permanently secured, completely neutralizing the threat of friendly fraud.

Profitable Micro-Transactions: Selling a $2 skin via credit card results in the processor taking a massive percentage. High-speed networks like Tron reduce transaction fees to mere pennies, preserving your margins.

Instant Financial Settlement: Instead of waiting weeks for international bank payouts to clear, crypto gateways settle funds instantly, providing studios with immediate liquidity for ongoing development.

Enhanced Player Privacy: Cryptocurrency allows gamers to purchase items without surrendering sensitive credit card details, reducing the risk of data breaches.

Game developer's gateway partner

Building robust Web3 infrastructure is complex, and your engineering team should be focused on crafting incredible gameplay, not managing blockchain nodes. This is where INXY steps in as the premier payment integration partner for the gaming industry.

INXY provides a developer-friendly, enterprise-grade gateway designed specifically to handle the high volume and instant execution required by online games. By integrating the INXY API into your game client, you instantly enable secure, irreversible crypto checkouts. INXY handles the complex routing, real-time price conversions, and instant network confirmations, ensuring your studio receives its revenue safely and automatically.

Conclusion

The gaming industry evolves rapidly, and clinging to expensive, easily manipulated credit card networks is a massive liability. By adopting cryptocurrency payments, you fortify your revenue streams, permanently eliminate chargeback fraud, and provide a frictionless payment option globally.

Ready to level up your monetization strategy? Discover how our robust API solutions can protect your studio by visiting https://www.inxy.io/gaming today.

The Future of Global Commerce: Cross-Border Crypto Payments vs. Bank Transfers

The Future of Global Commerce: Crypto Payments vs. Traditional Banking The $190 trillion cross-border payment market is undergoing a systemic shift. While traditional SWIFT transfers remain the bedrock of trade, blockchain-based solutions are no longer just an alternative—they are a strategic imperative. Key Takeaways: Settlement Velocity: Moving from 3-5 business days to near-instant, 24/7/365 availability. Cost Optimization: Reducing transaction fees by 60% to 80% by removing intermediary "hops." Risk Mitigation: Eliminating chargeback fraud through blockchain immutability and transparent tracking. As we move toward a hybrid financial ecosystem, understanding these digital rails is essential for any global enterprise. Read our full analysis on how to future-proof your payment stack.

The global cross-border payment market is a staggering financial behemoth, moving approximately $190 trillion annually across the world's economies. For decades, this massive flow of capital has been heavily dominated by traditional financial institutions, operating on infrastructure originally designed in the pre-digital era. However, the legacy correspondent banking system is currently facing unprecedented, systemic disruption from blockchain technology and digital assets. As global commerce accelerates and borders become increasingly blurred in the digital age, the debate between Cross-Border Crypto Payments vs. Bank Transfers has become one of the most critical conversations in the fintech and crypto processing industry.

While traditional bank transfers remain the undisputed bedrock of global trade—largely due to their established regulatory frameworks, institutional trust, and systemic stability—crypto payments are rapidly gaining ground. Driven primarily by the rise of stablecoins and decentralized finance (DeFi) networks, these digital alternatives are emerging as a significantly faster, cheaper, and more inclusive alternative for businesses operating on an international scale.

For Chief Financial Officers, treasury managers, and e-commerce leaders, understanding the nuances of these two fundamentally different financial rails is no longer optional; it is a strategic business imperative. In this comprehensive, deep-dive guide, we will break down exactly how these two systems compare across key operational metrics, the roadblocks that remain, and how you can position your enterprise to leverage automated crypto processing for future growth.

Exploring the Great Divide: Cross-Border Crypto Payments vs. Bank Transfers

To truly understand the shifting paradigm in global finance, business leaders must look under the hood of how money actually moves across borders. The differences between legacy fiat rails and decentralized blockchain ledgers fundamentally alter how businesses manage cash flow, mitigate risk, and scale their operations globally. Let us examine the core operational differences.

1. The Mechanics of Speed and Settlement

Time is money, and in international trade, settlement delays can create cascading cash-flow bottlenecks that stifle growth, frustrate suppliers, and complicate supply chain management.

Traditional Bank Transfers: Traditional cross-border payments rely heavily on the SWIFT (Society for Worldwide Interbank Financial Telecommunication) messaging network and a highly complex "correspondent banking" model. Because it is logistically impossible for every bank in the world to hold direct, bilateral relationships with every other bank globally, a single international payment cannot simply travel from Point A to Point B. Instead, it often "hops" through multiple intermediary banks before reaching its final destination.

Timeframe: Because of these necessary intermediary hops, and the manual reconciliation required at each step, settlements typically take anywhere from 2 to 5 business days to clear.

Limitations: Traditional transactions are strictly bound by localized banking cut-off times, weekends, and regional bank holidays. If a company in London sends a payment to a supplier in Tokyo on a Friday afternoon, that payment will sit in limbo until the following Monday—or longer, if there is a local holiday. This creates highly unpredictable cash-flow gaps.

Crypto & Blockchain Payments: Blockchain networks operate on a fundamentally different, modern architecture: a decentralized, single-ledger system. This technology allows for direct, peer-to-peer (P2P) transfers that bypass traditional intermediary banks entirely.

Timeframe: Settlements on blockchain networks occur in a matter of seconds or minutes, regardless of the geographic distance between the sender and the receiver. For example, enterprise-grade networks like Ripple (XRP) or major fiat-backed stablecoins settle almost instantly.

Limitations (or lack thereof): Cryptocurrencies and blockchain networks operate 24/7/365. They do not sleep, they do not observe weekends, and they do not pause for national holidays. This effectively eliminates the delays caused by traditional operating hours, allowing businesses to execute just-in-time cross-border settlements.

Professional Takeaway: If your business relies on rapid inventory turnover or immediate supplier payments, integrating a crypto payment gateway to facilitate stablecoin settlements can drastically improve your working capital cycles.

2. Cost Efficiency and the Death of Intermediaries

Profit margins on international sales and B2B vendor payments are frequently eroded by the opaque and compounding costs associated with moving money across borders.

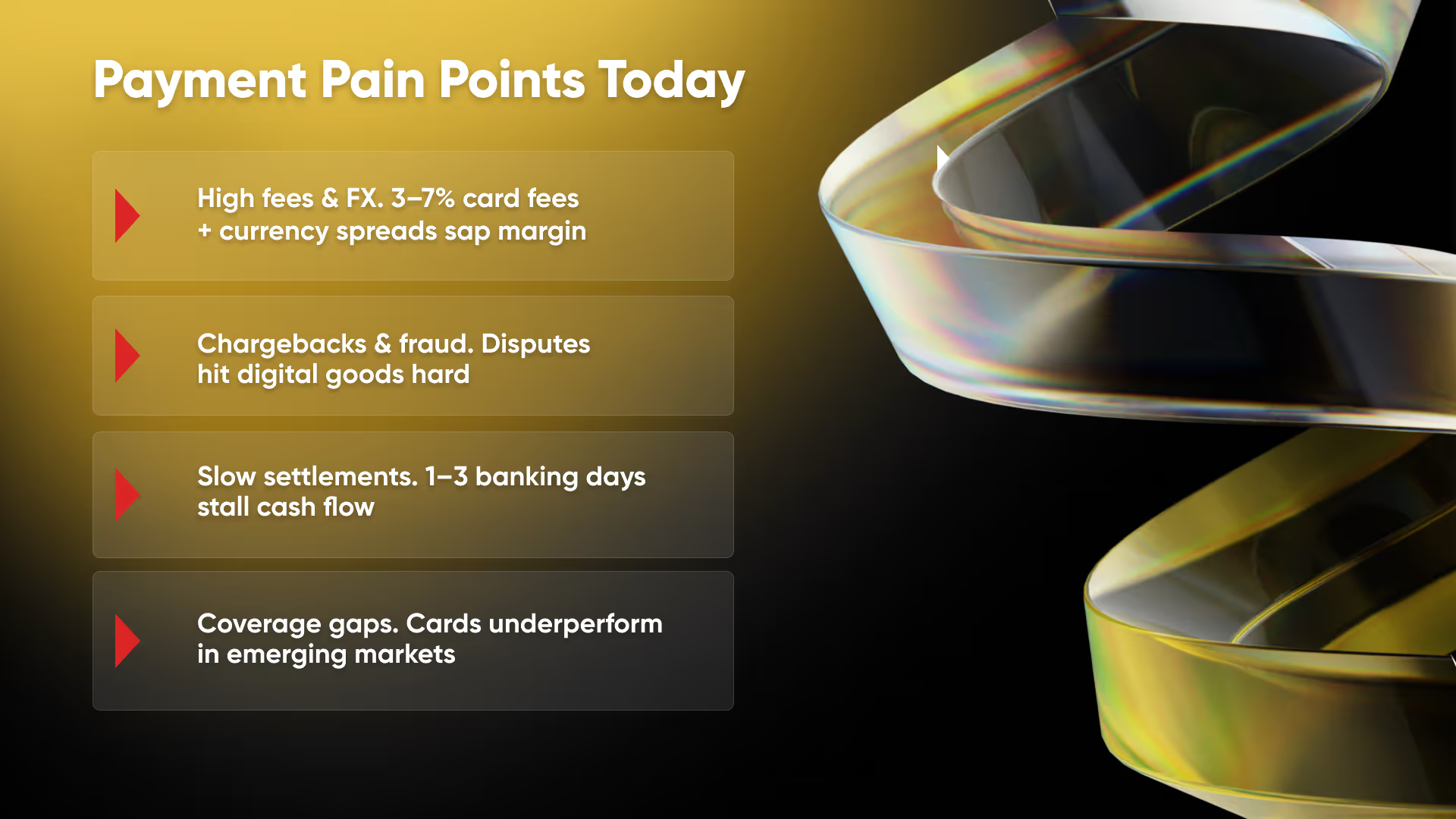

Traditional Bank Transfers: The multi-hop nature of correspondent banking means that each intermediary institution involved in the transfer process extracts its own toll. This can come in the form of a flat processing fee, an unfavorable foreign exchange (FX) spread, or a network messaging fee.

Impact: Transaction costs can be prohibitively high, especially for smaller retail payments, B2B micro-transactions, and remittances. According to recent data from the World Bank and the International Monetary Fund (IMF) [source: worldbank.org], high legacy banking fees remain one of the most significant barriers to global financial inclusion and frictionless international trade.

Crypto & Blockchain Payments: By systematically removing the middlemen from the transaction lifecycle, blockchain payments drastically reduce the costs associated with moving capital. The network validates the transaction programmatically, requiring only a small fraction of the fee traditionally charged by banks.

Impact: Comprehensive market research indicates that utilizing crypto or stablecoin rails can reduce cross-border transaction fees by a staggering 60% to 80%. This reduction is particularly transformative for the global remittance market and for small-to-medium enterprises (SMEs) that were previously priced out of efficient global trade due to prohibitive SWIFT fees. For businesses processing thousands of international transactions monthly, these savings directly, and heavily, impact the bottom line.

Professional Takeaway: Audit your current cross-border payment flows. Calculate the total annual cost of FX spreads and wire fees. For many e-commerce and SaaS platforms, migrating even 20% of cross-border volume to a crypto processing solution yields immediate, measurable ROI.

3. Security, Transparency, and Finality

How businesses track their funds in transit, and how they protect themselves from fraud, differs wildly between traditional banking and blockchain processing.

Traditional Bank Transfers: While the legacy banking system is highly secure, stringently regulated, and heavily insured, traditional transfers can be notoriously opaque for the end-user. Businesses often experience high levels of uncertainty regarding the exact status of a payment mid-transit. Furthermore, they frequently lack visibility into the final fees that will be deducted by intermediary banks before the funds arrive.

Additionally, traditional systems allow for chargebacks and settlement reversals. While designed to protect consumers, chargebacks pose significant administrative burdens and financial risks for online merchants who fall victim to "friendly fraud."

Crypto & Blockchain Payments: Blockchain ledgers are mathematically immutable. Once a transaction is algorithmically verified and recorded on the chain, it is permanent and cannot be altered, spoofed, or deleted.

Pros: This immutability provides total, unprecedented transparency. Anyone with the transaction hash can track the payment on the public ledger in real-time, eliminating the "where is my money?" anxiety. Furthermore, the irreversible nature of blockchain transactions entirely eliminates chargeback fraud—a massive relief for merchants, protecting businesses from unexpected revenue losses and malicious consumer behavior.

Cons: The absolute finality of the blockchain is a double-edged sword. If funds are mistakenly sent to the wrong wallet address due to human error, they are generally unrecoverable. Unlike a bank, there is no centralized customer service hotline to reverse an erroneous blockchain transaction.

Professional Takeaway: To mitigate the risk of lost funds via human error, utilize automated crypto payment gateways that generate dynamic, single-use QR codes and exact-amount payment links, removing the need for manual address entry by your clients.

Key Risks and Roadblocks to Mainstream Adoption

While crypto payments offer operational superiority in speed and cost, they face significant hurdles that prevent total mainstream displacement of traditional banking. A balanced fintech strategy must acknowledge and navigate these challenges.

1. The Volatility Dilemma Legacy cryptocurrencies like Bitcoin (BTC) or Ethereum (ETH) are highly speculative assets. A 10% price swing during a brief transaction window makes them highly impractical for standard corporate functions, such as payroll distribution or invoice settlements. This is exactly why the market is pivoting heavily toward stablecoins—digital assets pegged 1:1 to fiat currencies like the US Dollar, combining the technological speed of crypto with the economic stability of traditional money.

2. Regulatory Uncertainty & Compliance Protocols Traditional banks have spent decades building robust, globally recognized Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance frameworks. The pseudonymous nature of foundational cryptocurrencies complicates these essential compliance measures. Inconsistent, fragmented regulatory frameworks across different global jurisdictions make enterprise-level adoption risky for heavily audited corporations. Processing platforms must provide built-in compliance tools to bridge this gap safely.

3. Wholesale Dominance and Institutional Inertia Traditional financial systems are purpose-built to safely handle massive, multi-billion-dollar wholesale transactions between sovereign nations and multinational conglomerates. Currently, crypto payments represent only a small fraction of total global volume, primarily capturing retail, SME, and remittance flows. Unseating a $190 trillion entrenched system takes time.

The Future: Convergence Over Replacement

The consensus among top economic researchers and fintech analysts is that blockchain will not immediately replace traditional bank transfers; rather, the two systems are destined to integrate. We are moving toward a hybrid financial ecosystem.

Major financial institutions are already adopting blockchain infrastructure to modernize their own rails. For instance, J.P. Morgan has developed its own blockchain networks to facilitate 24/7 cross-border settlements for institutional clients. Additionally, global authorities and central banks are heavily researching and piloting Central Bank Digital Currencies (CBDCs). These sovereign digital assets aim to combine the speed, transparency, and efficiency of blockchain technology with the absolute trust, stability, and regulatory backing of traditional fiat money.

The future of the fintech processing industry lies in interoperability—systems that allow a business to accept a payment in a stablecoin from a client in Brazil, and have it instantly settled as fiat in a corporate bank account in Europe, entirely seamlessly.

Automating Business Processes with INXY

Navigating the transition from legacy finance to digital assets doesn't have to be a logistical nightmare. To stay competitive, modern businesses need payment infrastructure that is as dynamic and global as their customer base.

At INXY, we understand that navigating the complexities of Cross-Border Crypto Payments vs. Bank Transfers requires robust, reliable, and secure technology. Our cutting-edge payment gateway solutions are designed specifically to help forward-thinking enterprises automate their business processes, effortlessly bridging the gap between traditional fiat banking and the emerging crypto economy.

Whether you are looking to eliminate exorbitant SWIFT fees, accept cross-border stablecoin payments with zero volatility risk, or implement comprehensive cross-domain tracking for your payment flows, INXY provides the enterprise-grade infrastructure to make it happen seamlessly.

Ready to modernize your financial stack and expand your global reach without the friction of traditional banking? Explore our comprehensive suite of payment gateway solutions atINXY.io and discover how we can tailor an automated crypto processing strategy for your specific business needs. Contact our integration team today to future-proof your payment operations.

Cross-Border B2B Payments With Stablecoins: The 2026 Guide to Faster, Cheaper Settlement

This guide explains how cross-border stablecoin payments actually work, how they compare to SWIFT, where they make the most sense, and what it takes to start accepting them.

For most businesses, sending money across borders still feels like it did a decade ago: slow, opaque, and expensive. Cross-border crypto payments built on stablecoins are changing that. Instead of routing an international crypto payment through a chain of correspondent banks, a stablecoin transfer settles directly on a blockchain in seconds, for a fraction of the cost. In 2026 this is no longer a fringe experiment — it is one of the fastest-growing segments in business payments, and the data behind it is hard to ignore.

This guide explains how cross-border stablecoin payments actually work, how they compare to SWIFT, where they make the most sense, and what it takes to start accepting them.

Why cross-border crypto payments are replacing the old rails

The traditional system was never designed for the speed of modern commerce. It was designed for banks talking to banks.

The hidden cost of SWIFT and correspondent banking

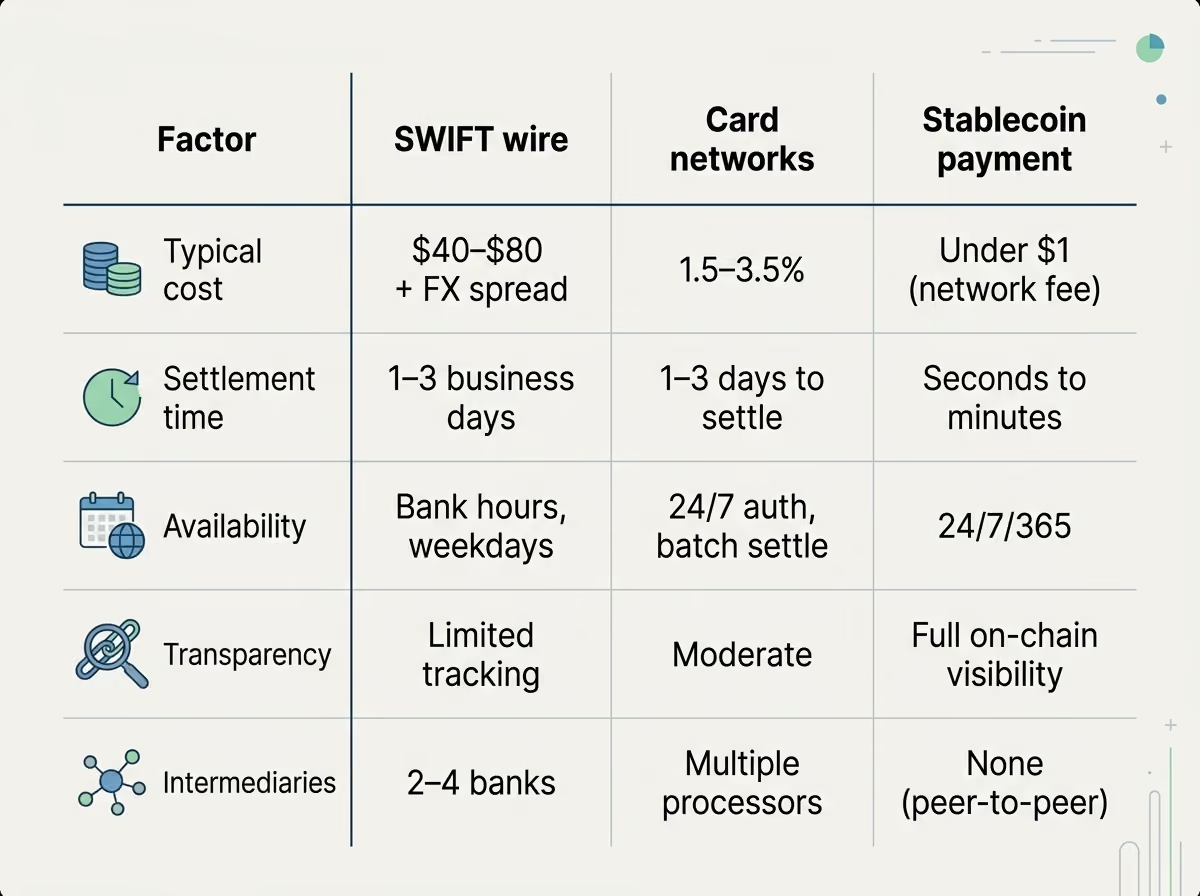

A typical international wire passes through two to four intermediary banks before it reaches the recipient. Each one takes a cut and adds a delay. The result is well known to any finance team: wire fees of roughly $40–$80 per transaction, settlement times of one to three business days (longer across exotic corridors), and almost no visibility into where the money is at any given moment. Add unfavorable FX spreads and the all-in cost of moving money internationally can quietly erode margins on every cross-border deal.

For a company paying dozens or hundreds of overseas suppliers, contractors, or partners each month, that friction compounds fast.

What changed in 2026

Stablecoins — blockchain tokens pegged 1:1 to a fiat currency such as the US dollar — turned out to be an almost perfect fit for this problem. They hold a stable value, move on open networks 24/7, and settle without a banking intermediary.

Adoption has gone vertical. Business-to-business stablecoin payment volume grew roughly 733% year over year heading into 2026, and total stablecoin transaction volume reached about $33 trillion in 2025. Juniper Research projects that cross-border B2B stablecoin payments will hit $5 trillion by 2035, up from an estimated $13.4 billion today, with the large majority of that future value coming specifically from cross-border business use. In short: the rail is being built right now, and businesses that learn it early gain a cost advantage.

How stablecoin cross-border payments actually work

The mechanics are simpler than the technology sounds. Every cross-border stablecoin payment follows the same three-stage path.

On-ramp, settlement, off-ramp

On-ramp. The sender converts local fiat (USD, EUR, etc.) into a stablecoin such as USDC or USDT, either from existing treasury or through a payment provider.

Settlement. The stablecoin moves across a blockchain network directly to the recipient's wallet. This is the step that replaces the entire correspondent-banking chain.

Off-ramp. The recipient either holds the stablecoin or converts it back to their local currency and withdraws to a bank account.

A provider like INXY handles the on-ramp, settlement, and off-ramp as a single flow, so the business never has to touch a crypto exchange directly.

Stablecoins and networks used

Most B2B volume runs on US-dollar stablecoins — USDC, USDT, and increasingly PYUSD — because they remove currency-volatility risk while keeping the speed of crypto. The network matters too, because it determines how fast and how cheaply a payment finalizes:

Solana — settlement finality in under half a second, with sub-cent fees.

Tron — finality in roughly one to two seconds; widely used for USDT.

Ethereum Layer-2s — low fees with fast confirmation, anchored to Ethereum security.

The practical takeaway: a payment that took three days on SWIFT can finalize in seconds on the right chain.

Stablecoins vs SWIFT: cost, speed, and transparency

The clearest way to understand the shift is a side-by-side comparison of low fee crypto payments against the legacy rails.

The economics are most dramatic at scale. Dropping from $40+ per wire to under $1 per transfer changes what is financially viable — micro-payments, frequent payouts, and thin-margin corridors that never made sense on SWIFT suddenly do.

Top use cases for global crypto transactions

Stablecoins are not a fit for every payment, but for global crypto transactions between businesses they solve real, recurring pain.

Supplier and vendor payments. Pay overseas manufacturers and service providers same-day instead of waiting for a wire to clear, improving supplier relationships and unlocking faster terms.

Contractor and team payouts. Pay international contractors and remote staff in stablecoins without losing 5–10% to fees and FX on every transfer. (INXY also covers dedicated crypto payroll.)

Marketplace and platform payouts. Distribute earnings to sellers, affiliates, or creators across many countries in a single batch, at predictable cost.

Treasury and intercompany transfers. Move funds between entities and regions instantly, holding value in a dollar-pegged asset rather than parking it in slow, fee-heavy banking channels.

These are exactly the corridors where the old system performs worst — many small-to-mid payments, many destinations, tight margins.

Are low fee crypto payments compliant? GENIUS Act and MiCA

A fair question from any finance or legal team: is this allowed? In 2026, the answer is increasingly yes — and the regulatory ground is firmer than it has ever been.

In the United States, the GENIUS Act established the first federal framework for payment stablecoins, requiring issuers to be licensed, to hold 1:1 reserves in high-quality liquid assets, and to honor redemption on demand. In the European Union, MiCA (Markets in Crypto-Assets) provides a parallel framework. Together they have moved stablecoins from a regulatory gray zone into supervised, standardized instruments — which is a large part of why institutional adoption accelerated.

What a regulated provider handles for you

Compliance does not have to live on your team. A regulated payment provider performs KYB (Know Your Business) onboarding, screens transactions against AML requirements, and maintains the audit trail you need for reporting. The business gets the speed and cost benefits of stablecoins while the provider absorbs the regulatory heavy lifting.

How to start accepting cross-border crypto payments

Getting started is closer to onboarding a payment processor than to learning crypto.

Choose a regulated provider that supports on-ramp, settlement, and off-ramp in your corridors — not a raw exchange.

Complete KYB onboarding and connect your bank account or treasury.

Pick your stablecoins and networks (USDC/USDT on a fast, low-fee chain) and set how recipients receive funds — held as stablecoin or auto-converted to local fiat.

Integrate and pay. Use the dashboard for one-off and batch payments, or the API to automate payouts inside your existing systems.

Once live, a cross-border payment that used to mean a wire form and a three-day wait becomes a few clicks and a few seconds.

The bottom line

Cross-border B2B payments are being rebuilt on stablecoin rails, and the trend lines — 733% volume growth, a projected $5 trillion market, and clear regulation under the GENIUS Act and MiCA — point in one direction. For businesses that move money internationally, stablecoins offer dramatically lower fees, near-instant settlement, and full transparency, without the volatility of traditional crypto. The companies adopting it now are the ones that will spend the next decade paying cents where their competitors pay tens of dollars.

Are stablecoin payments legal for business? Yes. In 2026, US-dollar stablecoins are regulated under the GENIUS Act in the United States and MiCA in the EU. Using a licensed provider keeps your KYB and AML obligations covered.

How fast is settlement? Depending on the network, a stablecoin payment finalizes anywhere from under a second (Solana) to a couple of minutes — versus one to three business days for a SWIFT wire.

What fees apply? The main cost is a small blockchain network fee, often under $1, plus any provider conversion fee on the on-ramp or off-ramp. This compares to $40–$80 per traditional international wire.

USDC or USDT for cross-border payments? Both are widely accepted dollar-pegged stablecoins. USDC is often preferred for its regulatory transparency; USDT has deeper liquidity in some corridors. A good provider supports both so you can match the recipient's preference.