“Web3 payments” describe a new way to move money in which value travels directly across a blockchain network instead of through banks and card schemes. Unlike traditional online transactions, blockchain payments settle peer-to-peer on a public ledger, are verifiable by anyone, and can run without a central intermediary holding the funds. For businesses, this means faster settlement, lower cross-border costs, and programmable money that can enforce its own rules.

This guide explains what web3 payments are, how they work under the hood, where smart contracts fit in, and how they compare to the crypto checkout flows most merchants already know. It is written for founders, finance teams, and product managers evaluating whether on-chain rails belong in their stack.

What Are Web3 Payments?

Web3 payments are transactions executed on decentralized blockchain networks, where ownership of funds is tied to a cryptographic wallet rather than a bank account. The term “web3” refers to the third era of the internet — one built on open, user-owned protocols. In a payment context, web3 crypto payments let a payer send value (typically stablecoins such as USDC or USDT, or assets like ETH and BTC) straight to a recipient’s wallet, with the network itself confirming and recording the transfer.

Three properties separate web3 payments from conventional digital payments:

- Self-custody. The payer controls the funds via private keys until the moment of transfer — there is no card issuer or bank acting as gatekeeper.

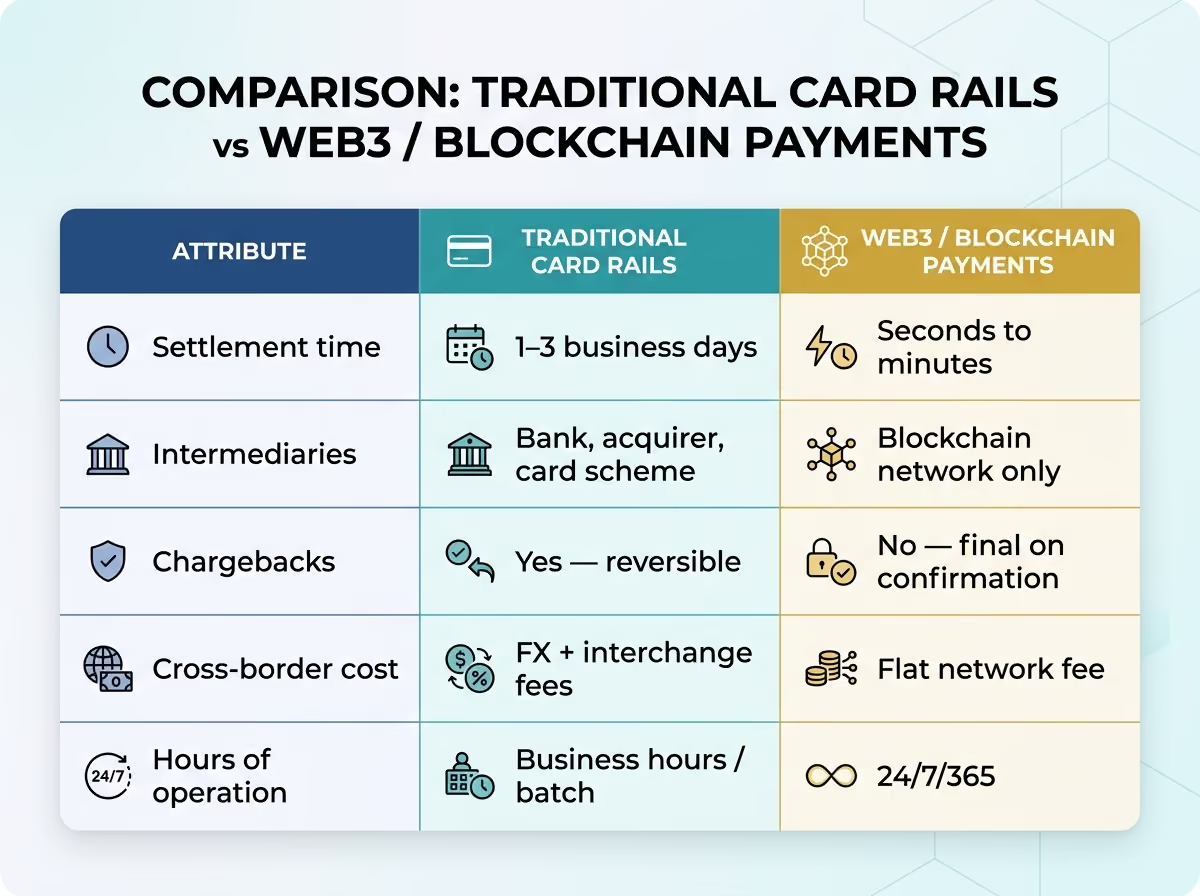

- On-chain settlement. The transaction is final once confirmed by the network, usually in seconds to minutes, with no multi-day clearing cycle.

- Programmability. Logic can be attached to the payment itself, so funds release only when predefined conditions are met.

The market context matters. According to recent industry analysis, fiat-backed stablecoins surpassed $300 billion in market capitalization in late 2025, with annualized on-chain settlement volumes in the mid-$20-trillion range — evidence that web3 rails are moving from experiment to real economic activity.

It helps to see where web3 payments sit relative to terms you already use. “Crypto payments” is the umbrella term for paying with digital assets at all. “Web3 payments” is the subset that runs on open, permissionless networks with user-held funds — as opposed to a closed processor that simply accepts coins and settles them to your bank. That difference in architecture is what unlocks the speed, reach, and automation covered below.

How Web3 Payments Work: Blockchain & Wallets

Blockchain payments rely on three components working together: a wallet that holds the keys, a blockchain network that validates transactions, and (for business use) a gateway that translates the on-chain event into something an accounting system can read. Here is the flow in plain terms.

The role of self-custody wallets

A crypto wallet does not “store” coins; it stores the private keys that prove ownership of a balance recorded on-chain. When a customer pays, their wallet signs the transaction with that key, authorizing the network to move the balance to the merchant’s address. Because the key never leaves the user, there is no card number to steal and no chargeback to reverse — a structural difference from card payments.

On-chain settlement vs. traditional rails

In a card transaction, authorization, clearing, and settlement happen across several institutions over one to three business days. With blockchain payments, validators confirm the transfer and write it to an immutable ledger in a single step. The table below summarizes the practical differences.

Smart Contract Payments Explained

Smart contract payments are blockchain transactions governed by self-executing code. A smart contract is a program deployed on-chain that automatically performs an action — release funds, split a payment, issue a refund — when its conditions are satisfied. No human has to intervene, and no party can alter the outcome once the contract is live.

Automated & programmable payments

This is where web3 moves beyond simple transfers. A smart contract can hold funds in escrow and release them only when a delivery is confirmed, automatically distribute revenue among several wallets, or stream a salary continuously over time. For businesses, programmable money reduces manual reconciliation and removes the trust gap in multi-party deals.

Consider a marketplace that owes three parties on every sale: the seller, an affiliate, and the platform itself. With cards, that single payment is captured, then split later through separate payout runs and reconciliation. A smart contract executes the split atomically — the moment funds arrive, each wallet receives its share in the same transaction. The same logic powers milestone-based contractor payments, automated refunds, and subscription renewals, all without a card on file or a manual approval step.

- Escrow: funds lock until both sides meet their obligations.

- Revenue splits: a single incoming payment is divided across partners in one transaction.

- Recurring & usage-based billing: subscriptions and metered charges execute on-chain without a card on file.

Tokenized payment solutions

Tokenized payment solutions represent real-world value — a dollar, an invoice, a loyalty credit — as a transferable token on a blockchain. Stablecoins are the most widely used example: a token pegged 1:1 to fiat that combines the stability of a currency with the speed of crypto. Industry research estimates that B2B flows already account for roughly 40% of real-economy stablecoin payments and are growing about 65% per year, which is why tokenized settlement is becoming the default rail for cross-border business payments.

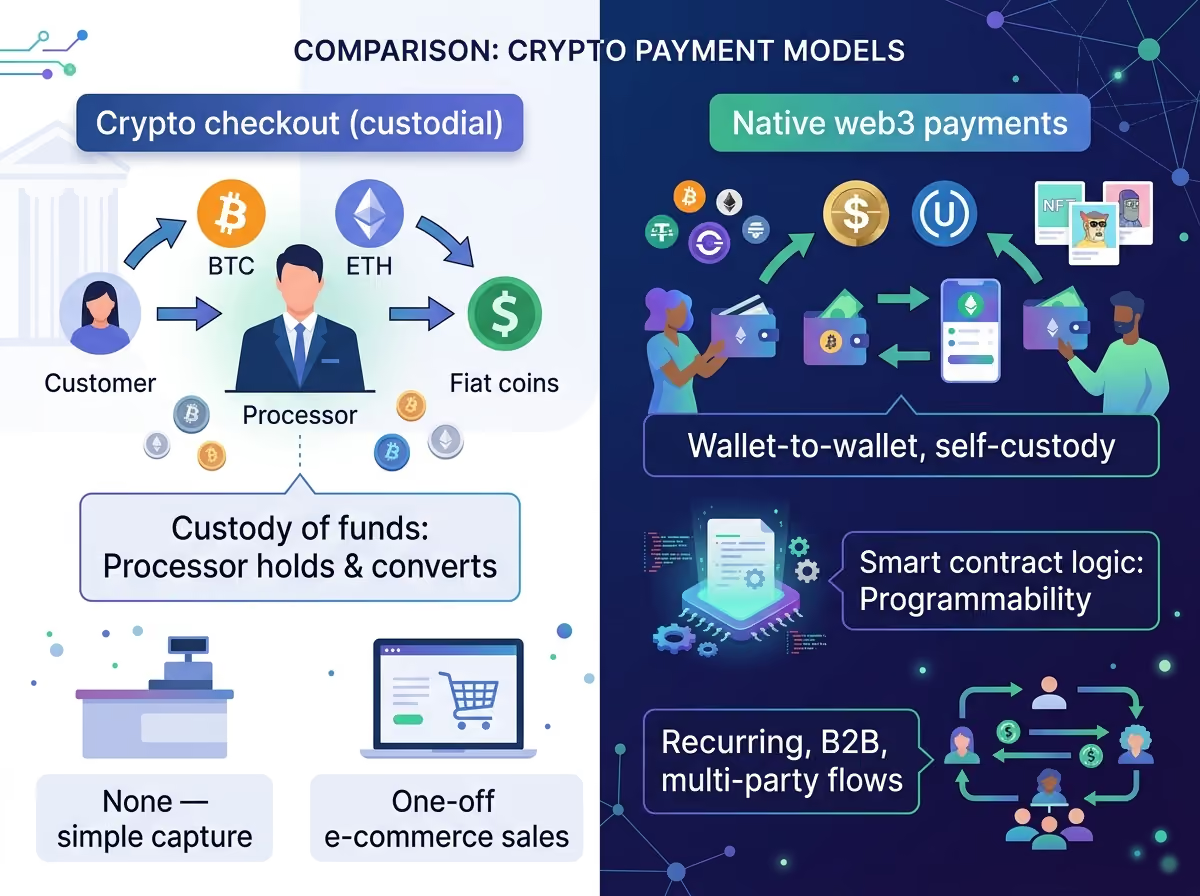

Web3 Payments vs. Traditional Crypto Checkout

Many merchants already “accept crypto” through a hosted checkout that converts coins to fiat. That is a useful on-ramp, but it is not the same as a full web3 payment model. The distinction is about who controls the funds and whether the payment carries logic.

In practice the two coexist. A business might use a custodial checkout for retail customers while using native, programmable rails for supplier payouts and partner settlements. For a deeper breakdown of provider roles, see our guide on the difference between a crypto payment gateway and a processor.

Benefits & Risks for Businesses

Web3 payments — and the broader category of blockchain smart contracts for business — offer clear operational upside, but they come with trade-offs that finance and compliance teams should weigh.

Key benefits:

- Near-instant, 24/7 settlement that frees up working capital.

- Lower cross-border fees by removing correspondent-banking layers.

- No chargebacks, reducing fraud exposure for digital goods.

- Automation of escrow, splits, and recurring billing through smart contracts.

Risks to manage:

- Price volatility on non-stablecoin assets — most businesses settle in stablecoins to neutralize this.

- Irreversibility means errors and misdirected payments are hard to recover.

- Regulatory obligations: under frameworks like the EU’s MiCA, you must work with a licensed VASP/CASP and apply KYC/AML and Travel Rule checks.

- Smart-contract risk: poorly audited code can be exploited, so use vetted, audited contracts.

For most companies the practical answer is not to choose between safety and innovation, but to adopt web3 payments through a partner that has already solved custody, compliance, and key management. That keeps the operational benefits — speed, automation, global reach — while shifting the hardest security and regulatory work to infrastructure built for it.

How to Start Accepting Web3 Payments

You do not need to build blockchain infrastructure in-house. A compliant gateway abstracts the wallet, network, and conversion layers so you can accept on-chain payments with a standard integration. A practical path:

- Choose your settlement asset. Stablecoins (USDC, USDT, DAI) are the standard for business to avoid volatility.

- Select a regulated provider. Confirm licensing, multi-chain support, and KYC/AML coverage for your regions.

- Integrate via API or plugin. Add the checkout or payout flow and connect webhooks to your back office.

- Decide what to automate. Map which payments — escrow, splits, recurring — benefit from smart-contract logic.

INXY provides a regulated, EU-compliant gateway for exactly this. Explore the web3 payments solution and our smart-contract payment infrastructure, or read how to accept crypto payments in 2026 for the full setup walkthrough.

FAQ

What are web3 payments in simple terms? They are payments sent directly between crypto wallets over a blockchain, without a bank or card network in the middle. The network verifies and records the transfer.

Are web3 payments safe? The underlying blockchain settlement is highly secure and tamper-resistant. The main risks are user error, asset volatility, and smart-contract bugs — all manageable by using stablecoins, audited contracts, and a regulated gateway.

What is a smart contract payment? A payment controlled by on-chain code that executes automatically when set conditions are met — for example, releasing escrowed funds once delivery is confirmed.

How are web3 payments different from accepting Bitcoin at checkout? A standard crypto checkout is custodial and converts coins to fiat. Native web3 payments keep funds in self-custody and can carry programmable logic, making them better suited to recurring, B2B, and multi-party flows.