How to Integrate a Crypto Payment API: A Developer’s Guide for 2026

In the fast-moving world of fintech, the question is no longer if a business should accept cryptocurrency, but how seamlessly it can be integrated. As we move through 2026, the European market has reached a point of high maturity. With the full enforcement of MiCA (Markets in Crypto-Assets) regulations, crypto payments have transitioned from a niche experiment to a standardized financial tool for EU-based enterprises.

For developers and product managers, integrating a crypto payment API is now as streamlined as traditional fiat gateways, provided you follow the right architectural patterns.

1. Understanding the 2026 Integration Workflow

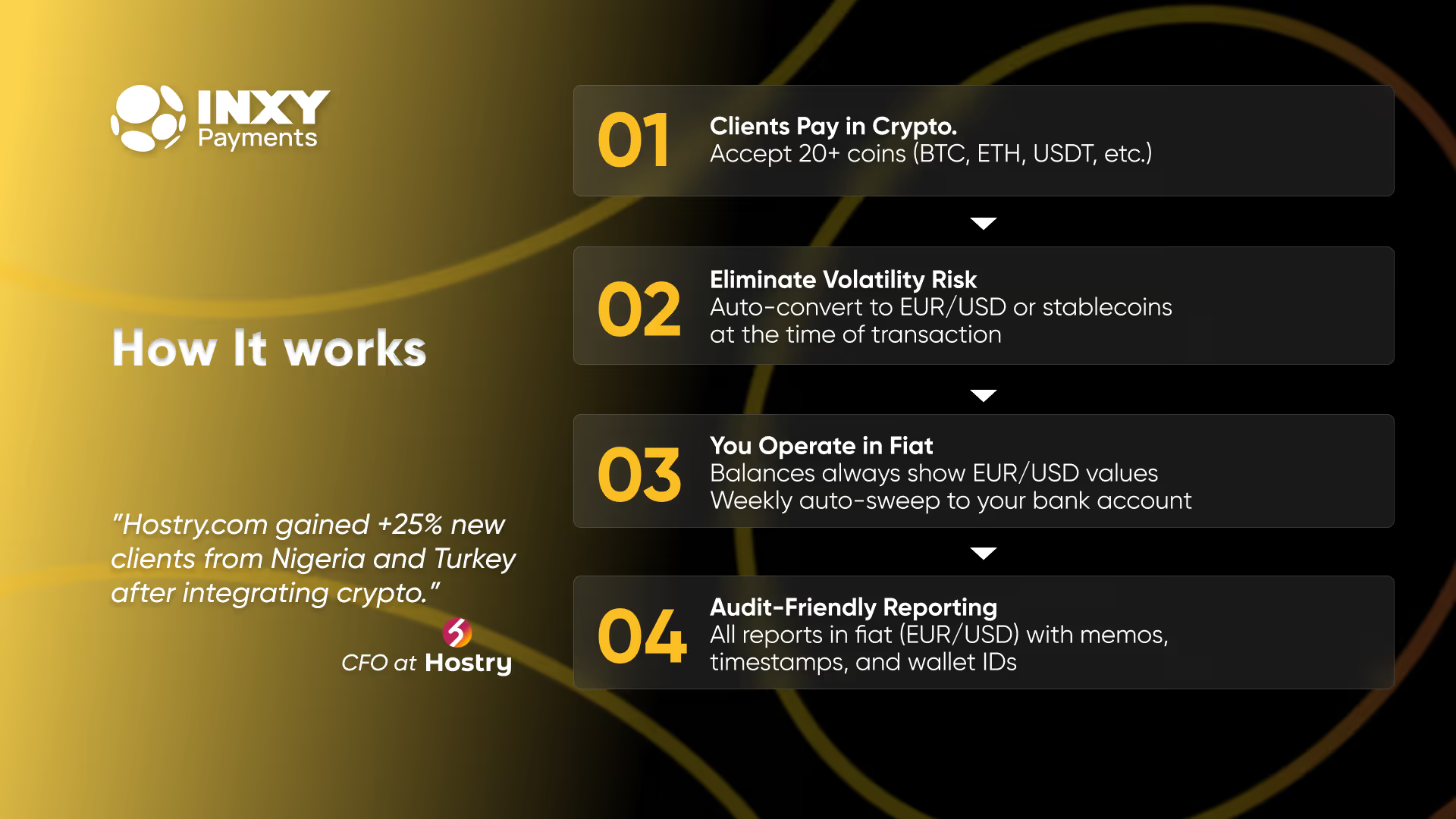

Modern crypto integration follows a predictable RESTful pattern. Unlike the early days of manual wallet monitoring, today’s gateways handle the blockchain's complexity, allowing your backend to interact with simple JSON payloads.

The standard lifecycle of a crypto payment includes:

- Initialization: Your server requests a unique payment address for a specific order.

- Monitoring: The gateway monitors the blockchain (Bitcoin, Ethereum, Tron, etc.) for incoming transactions.

- Confirmation: The gateway verifies the transaction depth (number of block confirmations).

- Webhook Notification: Your system receives an asynchronous callback to update the order status.

2. Step-by-Step API Integration

Phase A: Environment Setup

Before hitting production, high-quality gateways provide a Sandbox environment. This allows you to simulate successful payments, timeouts, and underpayments without risking real capital. You’ll typically need two headers for every request:

- X-API-KEY: Your unique identifier.

- X-PAY-SIGNATURE: A HMAC-SHA512 hash to ensure data integrity.

Phase B: Creating the Payment

To start a checkout, your backend sends a POST request to the /invoices or /payments endpoint.

JSON

{

"amount": 150.00,

"currency": "EUR",

"order_id": "ORDER-9921",

"callback_url": "https://yourstore.com/api/webhooks/crypto"

}

The gateway responds with a destination address and a QR code URL. In 2026, the best UX practice is to offer "Invisible Crypto"—where the user sees a familiar interface, and the gateway handles the real-time conversion behind the scenes.

Phase C: Handling the Webhook

This is the most critical part of the integration. Since blockchain transactions are asynchronous, your server must be ready to receive a POST callback.

Pro Tip: Always verify the webhook signature. Never update an order status based solely on the incoming payload without checking that the request actually originated from your provider.

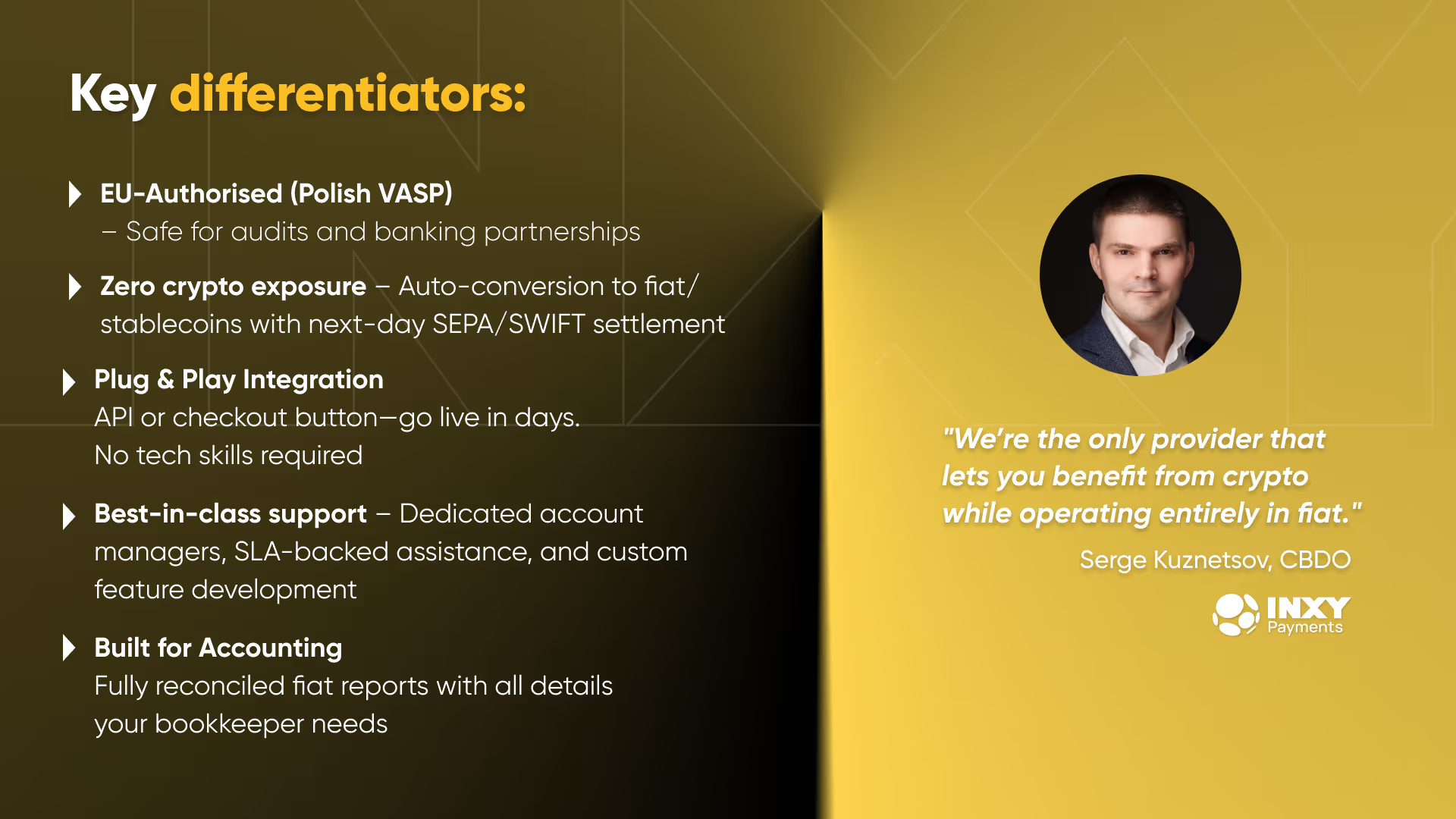

3. Security and Compliance in the EU

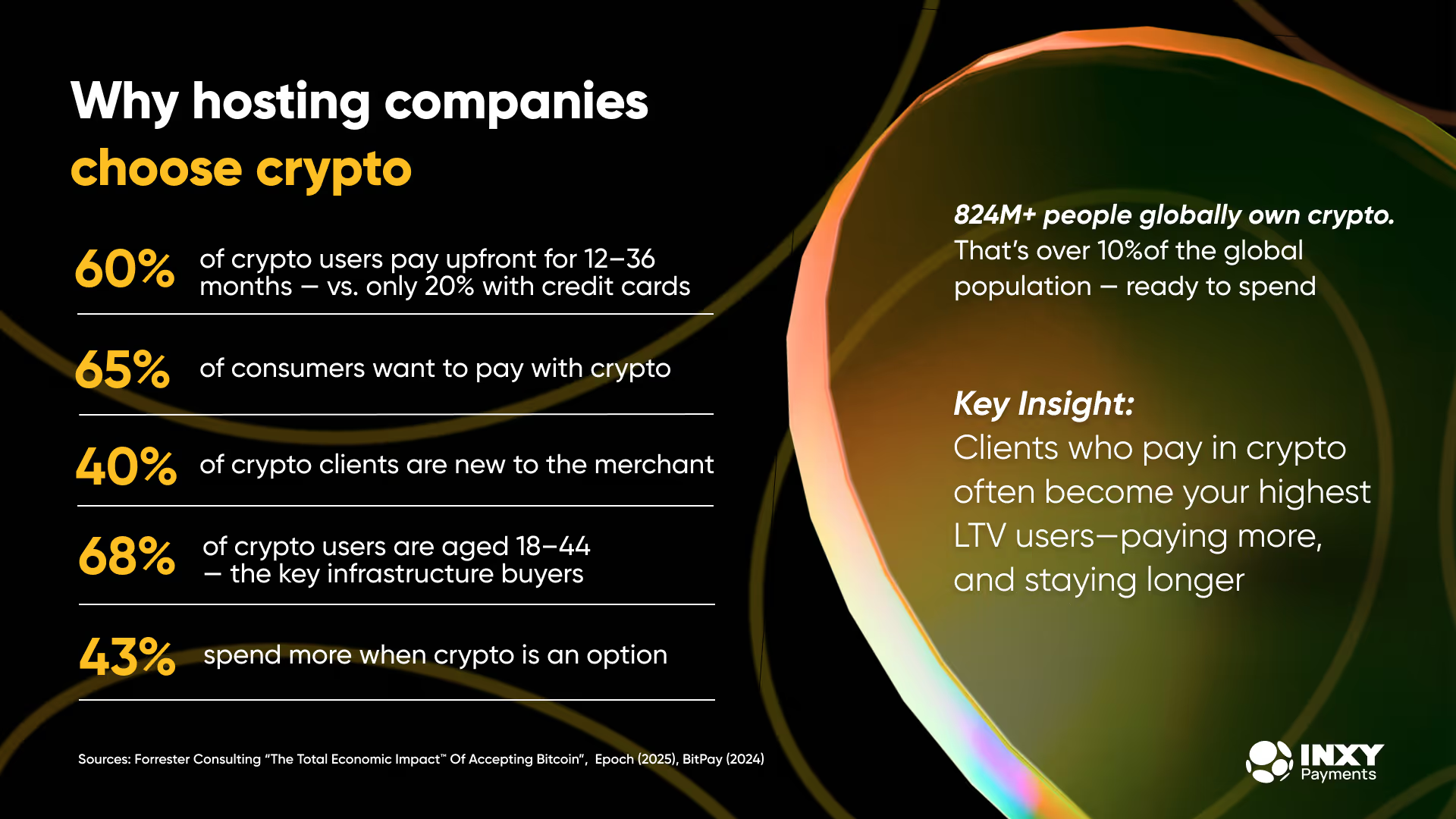

In the 2026 fintech landscape, security isn't just about encryption; it's about regulatory alignment. Within the EU, businesses must ensure their payment partner adheres to Transfer of Funds Regulation (TFR) and AML (Anti-Money Laundering) standards.

When choosing a provider, look for features like:

- Auto-Conversion: Instantly swapping volatile assets into stablecoins or EUR to protect your margins.

- Audit-Ready Reporting: Financial statements that your accounting team can actually use for VAT and tax filings.

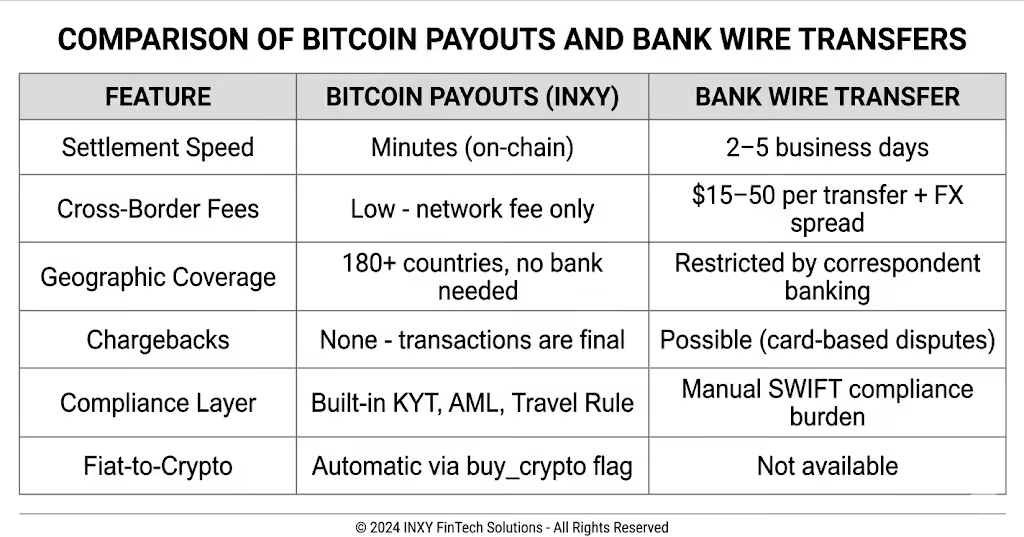

This is where specialized gateways like INXY (inxy.io) excel. Built specifically for the EU market, INXY acts as a regulated bridge. It doesn't just provide an API; it provides a compliant infrastructure that allows Web2 companies to scale into Web3 without the headache of managing private keys or worrying about crypto volatility. By integrating a solution like INXY, businesses can reduce processing fees by up to 70% compared to traditional card networks, while benefiting from instant SEPA settlements.

4. Testing and Optimization

Before going live, run "Chaos Tests" on your integration. What happens if a user sends too little? What if they pay after the 20-minute price-lock window? A robust API should provide clear error codes for these scenarios, allowing your frontend to guide the user toward a resolution—such as a partial refund or a top-up payment.

Conclusion

Integrating a crypto payment API in 2026 is a strategic move that opens your business to a global, tech-savvy audience. By utilizing professional gateways that handle the heavy lifting of compliance and conversion, your team can focus on what matters: the product.

Ready to modernize your payment stack? Would you like me to draft a technical checklist for your dev team to use during the INXY sandbox testing phase?

.avif)