The end of fiat friction: Why strategic merchants are switching to stablecoin payments

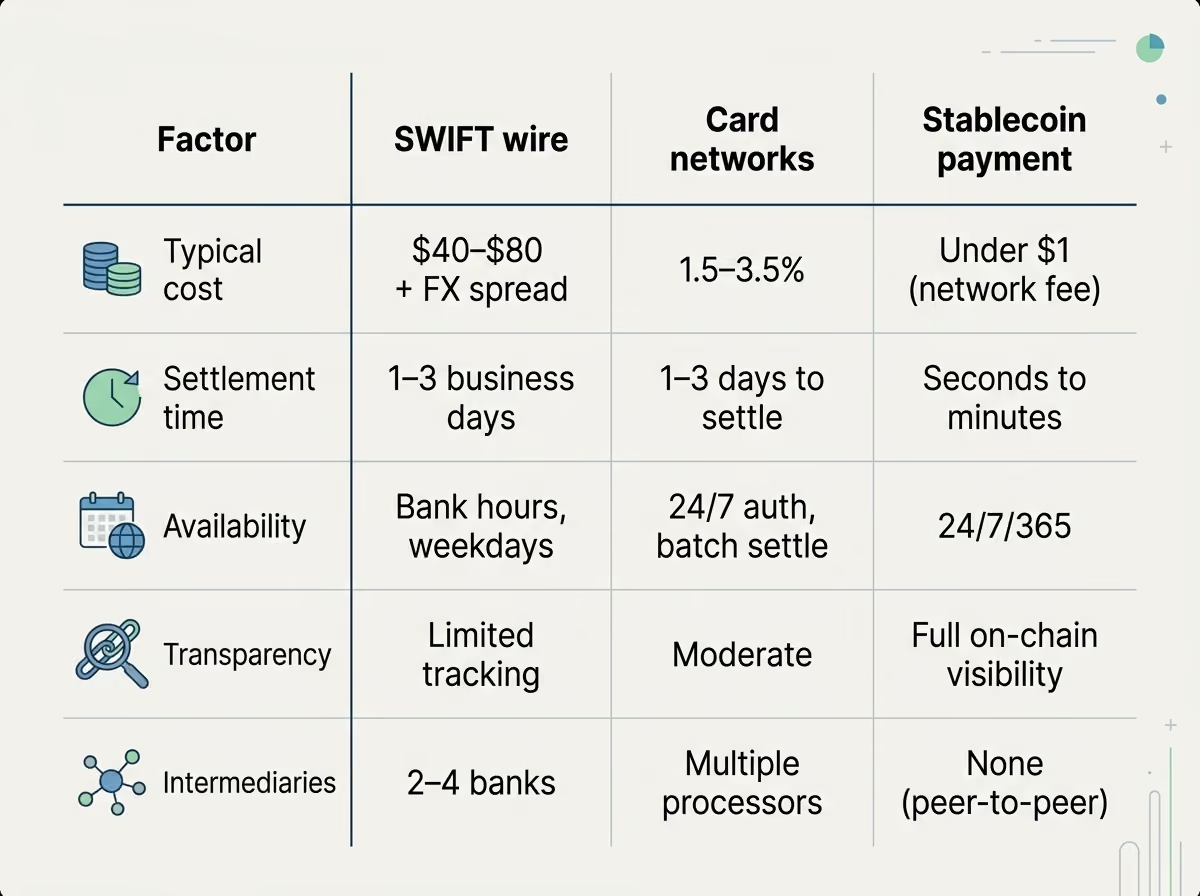

The legacy financial system imposes a structural tax on growth. For decades, merchants have absorbed correspondent banking fees, 3% interchange costs, and chargeback losses that erode margin on every transaction. In a global economy, waiting T+3 or T+5 for settlement is not an inconvenience — it is a liquidity problem.

To accept crypto once meant exposure to price volatility. That is no longer the case. Stablecoins — pegged to the US Dollar or Euro — deliver the settlement efficiency of blockchain without the speculation. For C-level executives, the question is no longer whether to integrate digital assets, but how quickly legacy bottlenecks can be replaced with purpose-built infrastructure.

1. Settlement velocity: From days to seconds

Traditional cross-border settlements move through a chain of intermediate banks, accumulating fees and losing transparency at every hop. SWIFT provides no real-time visibility into where funds are or when they will arrive.

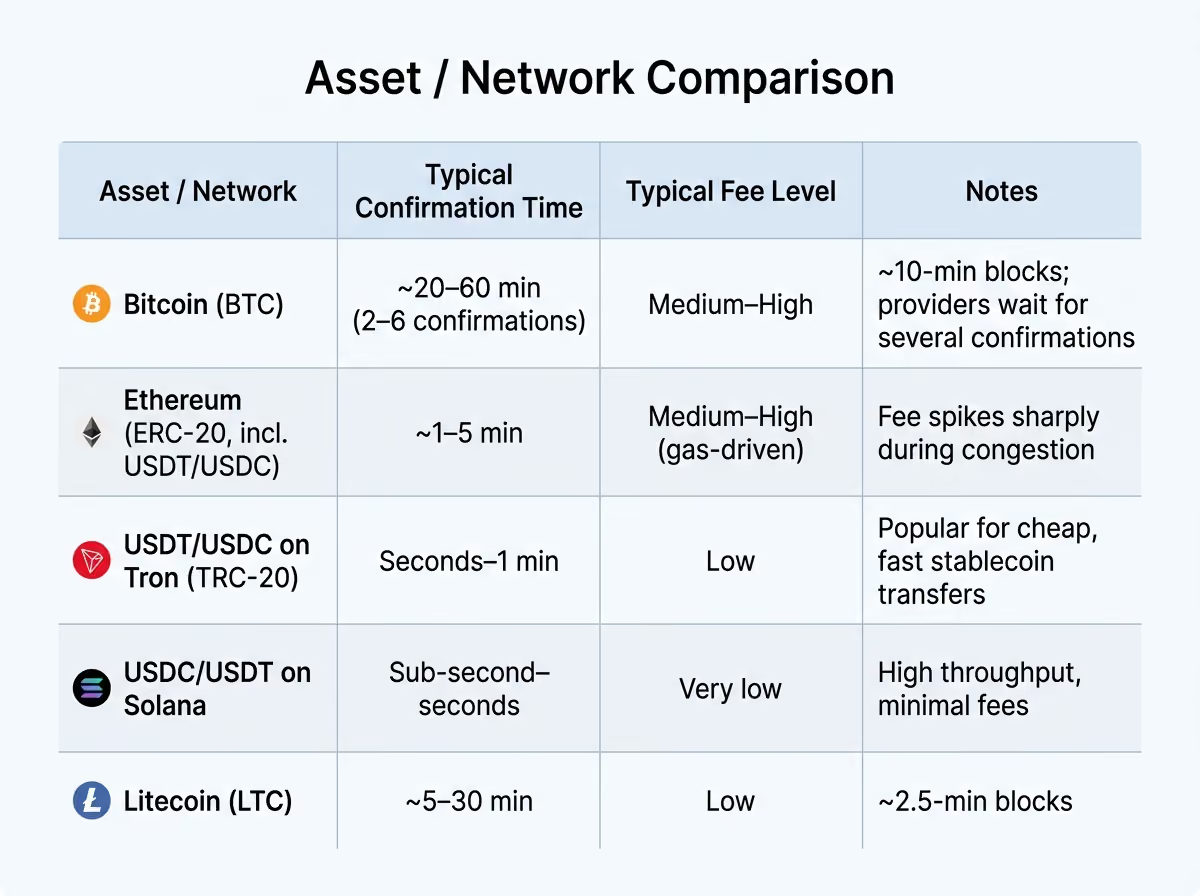

Stablecoins operate on a 24/7/365 ledger with near-instant finality. Settling on Ethereum, Polygon, or TRON, merchants are no longer bound by banking hours or cut-off windows. Capital lands, clears, and is available for redeployment immediately — not in a pending queue.

inxy.io integrates directly into this settlement layer, giving merchants the operational continuity that traditional finance structurally cannot offer.

2. Eliminating the chargeback tax

Chargeback fraud costs merchants billions annually. Credit card networks are centralised by design, which means any transaction can be reversed — often at the merchant's expense, with little recourse.

Blockchain transactions are push-based and immutable. When a business chooses to accept crypto in the form of stablecoins, payment finality is guaranteed by the protocol, not by a bank's dispute resolution team.

- No chargebacks: Once confirmed on-chain, a transaction cannot be reversed by a third party.

- Reduced fraud overhead: No need for aggressive fraud filters that block legitimate customers.

- Revenue sovereignty: You control your income stream without intermediary intervention.

3. Technical infrastructure: Beyond the hype

A payment gateway needs to be a piece of production-grade fintech infrastructure, not just a wallet interface. High-volume merchants require an API that abstracts blockchain complexity without sacrificing control.

What inxy.io provides:

- 1. No crypto management overhead: Merchants do not handle tokens or gas fees. That layer is abstracted entirely.

- 2. Volatility protection: Pay-ins convert to stablecoins or fiat instantly, locking in value at the moment of transaction.

- 3. Multi-chain support: USDT, USDC, DAI, EURC, TON, BTC, ETH, LTC, TRX, BNB, DOGE across ERC-20, TRC-20, Polygon, and BSC — customers transact on the network that works best for them.

- 4. Real-time webhooks: Instant payment status notifications to your backend, enabling automated fulfilment or shipping triggers without polling.

- 5. Compliance stack: EU VASP (Poland), Canadian MSB, MiCA-ready, AML/KYT/KYC, sanctions screening via Elliptic and Sumsub, Big-4-friendly fiat reporting.

4. Drastic reduction in operational costs

Managing global payments typically means maintaining multiple local currency accounts and navigating FX spreads on every cross-border transfer. Stablecoins provide a single settlement layer that works across jurisdictions without currency conversion overhead.

Consolidating payment rails through inxy.io can reduce payment processing Opex by up to 80%. Instead of paying a chain of intermediaries for the movement of value, you pay for efficient infrastructure. That margin stays in the business.

FAQ: Navigating the stablecoin shift

Is it difficult to integrate a stablecoin gateway into an existing platform?

No. inxy.io integrates via a REST API or pre-built plugins for major e-commerce engines. Documentation and technical support are included, and most teams go live faster than a standard merchant bank account setup.

How do we handle gas fee volatility?

inxy.io routes transactions through high-throughput networks to keep fees minimal. Customers can select the most cost-effective network for their transaction — the infrastructure handles the routing logic.

How does accepting stablecoins affect our accounting?

USDT and USDC are pegged 1:1 to the dollar, which makes them materially simpler to account for than traditional cryptocurrencies. inxy.io provides detailed reporting and CSV exports compatible with standard accounting software and ERP systems.

What about regulatory compliance?

inxy.io is built with compliance as a core component, not an afterthought — EU VASP registration, MiCA readiness, AML/KYT screening, and Big-4-auditable reporting. Your business stays within the regulatory framework while operating at full velocity.

Scalability Without Compromise

The merchant of 2026 cannot run on 1970s banking rails. The competitive advantage belongs to businesses that eliminate payment friction and capture the full value of their transactions across borders.

inxy.io is the infrastructure layer for that transition — robust APIs, multi-chain settlement, and a compliance stack built for global scale.

Partner with INXY — secure your payment infrastructure and lead the market.