How to Verify a Merchant Account? Step-by-Step Guide

Navigating the regulatory landscape of 2026 is crucial for any business accepting digital assets. This guide provides a comprehensive, step-by-step walkthrough of the merchant verification process for crypto payment gateways in the European Union. From understanding the Markets in Crypto-Assets (MiCA) regulation to mastering the Know Your Business (KYB) documentation requirements, we detail exactly how to secure a verified, bank-grade account. Whether you are in e-commerce, hosting, or high-risk industries, this unified framework ensures your business is compliant, secure, and ready for the global economy.

The institutionalization of the digital asset economy within the European Union has reached a definitive stage. As the financial sector navigates the complexities of the mid-2020s, regulatory compliance and operational excellence are no longer optional for businesses seeking to leverage blockchain-based financial rails.

For crypto payment gateways based in the EU, such as INXY Payments, the verification workflow represents the first and most critical touchpoint in establishing a secure, bank-grade relationship with professional partners. This report provides an exhaustive analysis of the merchant verification process, grounded in the primary directives of the Markets in Crypto-Assets (MiCA) Regulation and the practical requirements of the Know Your Business (KYB) standards.

The Regulatory Landscape: MiCA, TFR, and DAC8

The "Regulatory Rubicon" has been crossed, shifting the focus of European authorities from drafting policy to aggressive enforcement. Central to this environment is the Markets in Crypto-Assets Regulation (MiCA), which has successfully harmonized the rules for digital assets across all 27 EU member states.

The verification process is now governed by three key frameworks:

- MiCA Authorization: Eliminates the "Wild West" era, ensuring only fully authorized providers operate within the EEA.

- Transfer of Funds Regulation (TFR): Enforces a "Zero Threshold" policy for the "Travel Rule," requiring detailed data on the originator and beneficiary for every transaction.

- DAC8: Mandates strict tax reporting and the collection of Tax Identification Numbers (TINs) to ensure fiscal transparency.

Architecture of the Know Your Business (KYB) Process

Know Your Business (KYB) is the primary defensive mechanism used by fintech gateways. Unlike Know Your Customer (KYC), which focuses on individuals, KYB requires a deeper exploration of corporate hierarchies.

The Verification Objectives:

- Legal Existence: Proving the business is a real, registered entity.

- Control Disclosure: Identifying the Ultimate Beneficial Owners (UBOs) to prevent the use of shell companies for illicit activities.

- Risk Scoring: Evaluating the industry, geography, and transaction profile of the merchant.

The INXY Payments Verification Workflow: A Step-by-Step Guide

The verification process is designed to be rigorous yet streamlined, ensuring all participants meet EU compliance standards. This is a unified process applicable to all merchants, regardless of their industry or integration method.

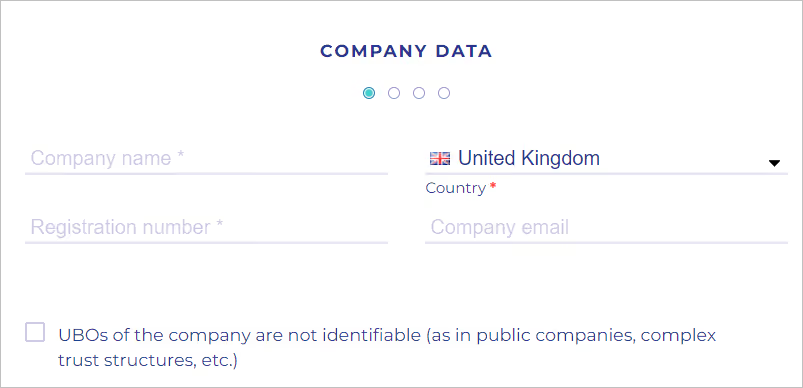

Step 1: Initial Company Data Intake

The process commences with the "Company data form." The merchant must enter fundamental identifying information, including the legal Company Name, official Registration Number, and Country of Registration.

Note: Providing a direct company email is recommended to ensure a clear line of communication with compliance officers.

Step 2: Comprehensive Documentation Upload

Merchants must validate their legal status by uploading a robust evidentiary file. Mandatory documents typically include:

- Certificate of Incorporation / Business Registration: Proof that the entity exists in a government registry.

- Articles of Association (AOA): Defines the entity's operations and leadership structure.

- Operating License: Required only if the merchant operates in a specifically regulated sector (e.g., gambling, forex).

Step 3: Ultimate Beneficial Owner (UBO) Identification

Identifying the natural persons who ultimately control the entity is the cornerstone of EU AML regulations.

- The 25% Rule: Merchants must identify any natural person holding more than 25% of ownership shares or voting rights.

- Verification: For each UBO, the system requires their full name, date of birth, and contact details. Identity verification can be performed live or via a secure link sent to the stakeholder.

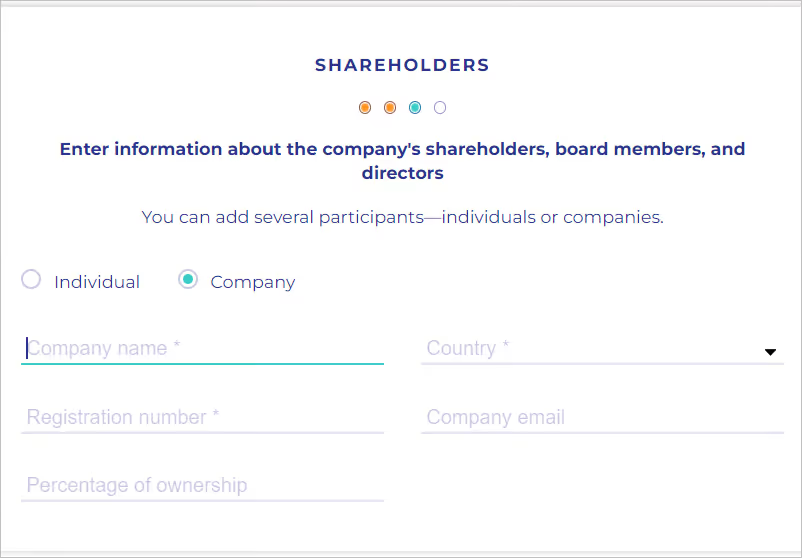

Step 4: Shareholder and Representative Verification

- Corporate Shareholders: If a shareholder is another company, the merchant must provide that entity's Articles of Association and trace the ownership chain back to a natural person.

- Legal Representative: Data must be provided for the person acting on behalf of the company, ensuring they have the legal authority (e.g., Director status or Power of Attorney) to open financial accounts.

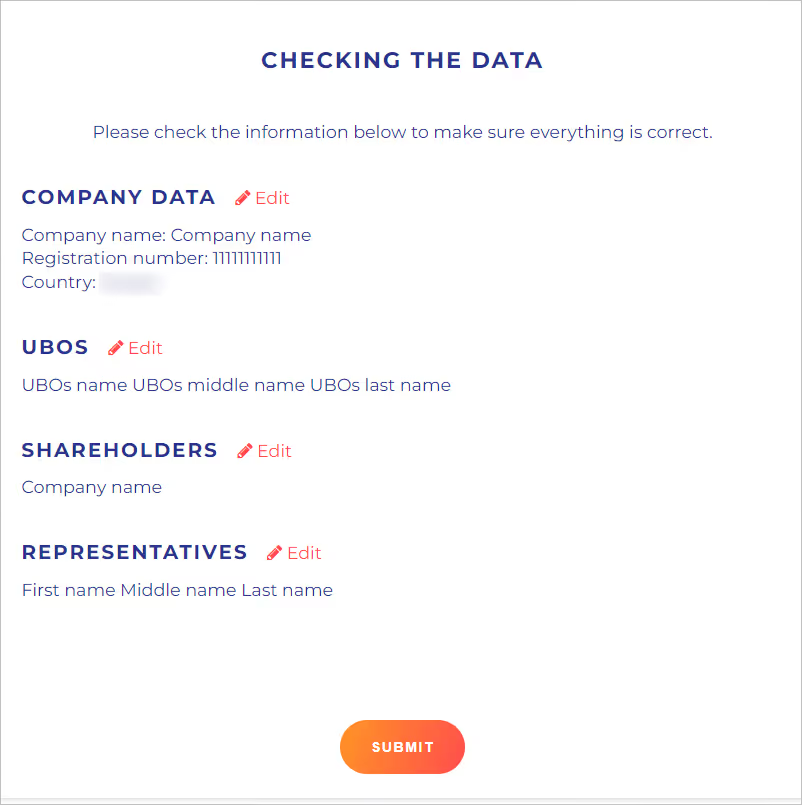

Step 5: Final Validation and Submission

The penultimate step is a thorough review of all provided data. Once confirmed, the application enters the compliance review queue. Thanks to automated systems, merchants can track their status in real-time via their dashboard.

Document Requirements and Authentication Standards

The integrity of the verification process relies entirely on the quality of the documentation. The European fintech environment maintains a high bar for validity.

Mandatory Conditions for Approval:

- Language: All documents must be in English. If the original is in another language, a notarized translation is required.

- Authentication: Documents must be "official," bearing the necessary stamps, signatures, or qualified electronic seals as per local laws.

- Recency: Extracts from commercial registries generally should not be older than 3 months to ensure the data is current.

Common Reasons for Rejection:

- Typos: Mismatches between the input form and the uploaded PDF.

- Missing Pages: Uploading incomplete Articles of Association.

- Low Quality: Blurry scans or photos where text is illegible.

Security and Data Protection (GDPR & DORA)

The sensitive nature of KYB data requires the highest levels of protection.

- GDPR Compliance: Data is used solely for client identification and activity justification, adhering to the principle of "Purpose Limitation."

- DORA (Digital Operational Resilience Act): Mandates that payment gateways demonstrate resilience against cyber threats. Data is encrypted at rest and in transit, with role-based access ensuring only authorized compliance personnel can view identity files.

Conclusion: Compliance as a Competitive Advantage

Completing the merchant verification process is more than a regulatory hurdle; it is a strategic move that positions a business as a credible player in the global economy. By adhering to this standardized verification workflow, merchants—whether they are hosting providers, e-commerce stores, or digital service agencies—secure a stable, bank-grade foundation for their financial operations.

In the mature crypto economy of 2026, a verified account is the key to unlocking global markets, ensuring seamless settlements, and protecting business capital from regulatory friction.