If you’ve spent any time navigating the fintech landscape in 2026, you’ve likely noticed that "crypto payment gateway" and "crypto payment processor" are thrown around like synonyms. In casual conversation, that’s fine. But if you’re a business owner in the EU trying to optimize your checkout or manage a complex treasury, the distinction matters. It’s the difference between a sleek front-end interface and the heavy-duty engine room that actually moves the money.

Let’s break down the technicalities of these two components and see how they work together to modernize your business.

The Crypto Payment Gateway: Your Digital Storefront

Think of the Crypto Payment Gateway as the "front-end" layer. It is the bridge between your website and the blockchain. Its primary job is to handle the customer-facing part of the transaction.

When a customer clicks "Pay with Crypto," the gateway jumps into action:

Checkout UI: It displays the QR code or wallet address.

Real-time Rate Locking: It calculates the exact exchange rate between, say, Bitcoin and the Euro, and freezes it for a few minutes so the customer knows exactly what they’re paying.

Data Transmission: It securely passes the transaction details to the processor.

Essentially, the gateway is the digital equivalent of a Point-of-Sale (POS) terminal. It’s all about user experience and making sure the "handshake" between the customer and the merchant is secure and seamless.

The Crypto Payment Processor: The Engine Room

While the gateway handles the "hello," the Crypto Payment Processor handles the "settlement." This is the back-end infrastructure that manages the lifecycle of the funds after the customer hits send.

The processor’s responsibilities are significantly broader:

Blockchain Validation: It monitors the network to confirm the transaction has reached the required number of blocks.

Settlement & Conversion: This is the big one. If you invoiced for €1,000 but the customer paid in Bitcoin, the processor handles the conversion and ensures those funds are ready for your bank account.

Compliance (KYC/AML): It runs the necessary checks to ensure the transaction isn't linked to illicit activity—a non-negotiable for EU-based businesses under current regulations.

Payouts: It manages the transfer of funds from the crypto ecosystem into your corporate SEPA or SWIFT account.

Comparison at a Glance

Feature

Crypto Payment Gateway

Crypto Payment Processor

Primary Role

Front-end UI / Communication

Back-end settlement / Logistics

Focus

User Experience (UX)

Compliance & Fund Movement

Key Output

QR Codes, API Callbacks

Fiat Payouts, Tax Reporting

Analogy

The Card Reader on the counter

The Bank/Clearing House

Why the Distinction Matters for EU Businesses

In the European fintech market, precision is everything. If you only use a "gateway" without a robust processing layer, you might find yourself with a wallet full of crypto but no easy way to pay your local taxes or suppliers in fiat.

Conversely, a processor without a good gateway might provide great liquidity, but your customers will struggle with a clunky, manual checkout process that kills your conversion rate.

This is where integrated solutions come in. Platforms like INXY bridge this gap by functioning as a unified ecosystem. By combining an EU-licensed gateway (the part your customers see) with a powerful processing engine (the part your accountant loves), it removes the friction of managing two separate services.

Why "All-in-One" is the 2026 Standard

Modern fintech has moved past fragmented tools. For instance, INXY Payments focuses heavily on high-conversion gateways specifically for e-commerce, infrastructure and hosting providers. Because they operate as an EU-authorized VASP (Virtual Asset Service Provider), the processing side is built-in.

For a merchant, this means:

Zero Volatility: The rate is locked at the gateway level and settled instantly at the processor level.

Mass Payouts: You can collect payments via the gateway and immediately use those funds to pay global affiliates or remote teams via the processor’s API.

Legal Clarity: Since the processor handles the KYB (Know Your Business) and AML checks, the funds landing in your bank account are "clean" and fully documented for tax purposes.

Summary

A gateway gets you paid; a processor keeps you in business. While they serve different technical functions, the most successful companies in 2026 are those that don’t make their customers (or their dev teams) choose between the two.

By using an integrated platform like INXY, you get the best of both worlds: a checkout experience that converts and a back-end that settles without the headaches of traditional banking delays.

Gemini said Here is a concise blog summary optimized for readability and engagement, designed to pull readers into the full guide.

Blog Summary: Integrating Crypto via INXY for WHMCS In 2026, cryptocurrency has moved beyond speculation to become a primary "production" currency for global digital services. For hosting providers and agencies using WHMCS, the shift toward stablecoins—the "Internet’s dollar"—is a critical competitive advantage. This guide explores how to integrate the INXY Payment Gateway, a robust solution designed to bridge the gap between traditional billing and the modern crypto economy.

In 2026, the fintech landscape is shifting from speculation to production. For hosting providers, VPN services, and digital agencies using WHMCS, the question is no longer if you should accept cryptocurrency, but how efficiently you can do it. With stablecoins becoming the "Internet’s dollar" for cross-border flows, integrating a robust payment gateway is essential for maintaining a competitive edge in the EU and global markets.

One of the most seamless ways to bridge the gap between traditional billing and the crypto economy is through the INXY Payment Gateway. This guide provides a detailed walkthrough for setting up the INXY module on your WHMCS platform.

1. Why Crypto for WHMCS in 2026?

Integrating crypto payments into your billing system offers several strategic advantages:

Lower Fees: Traditional processors often charge 2–4% for international payments, while gateways like INXY provide more cost-effective alternatives.

Chargeback Protection: Blockchain transactions are immutable; once confirmed, they cannot be reversed by the sender, eliminating the administrative burden of fraudulent chargebacks.

Global Reach: Crypto allows you to accept payments from customers in regions with restrictive banking or unstable local currencies without multi-day delays.

2. System Requirements

Before installation, ensure your environment meets the following criteria for the INXY module (Version 1.0.3):

Location: Go to Merchant settings → API in the INXY dashboard and paste the URL.

5. Advanced Matching and Underpayment Rules

Crypto transactions can sometimes result in minor amount differences due to network fees. INXY handles this through the config.php file:

Amount Deviation: By default, the module accepts payments within 1% of the requested amount. For WHMCS, it is recommended to set 'amount_deviation_percentage' = 49 to reduce unnecessary top-up attempts and align with WHMCS's partial payment flow.

Time Window: Payments must arrive within 2 hours in production (30 minutes in Sandbox) to be automatically matched.

6. Summary of Payment Outcomes

Status

Customer Experience

WHMCS Admin Status

Paid in Full

Invoice shows "Paid".

Order marked as paid.

Overpaid

Extra amount added as credit.

Visible credit in account.

Partially Paid

"Awaiting payment" status.

Balance reduced by amount received.

Expired

"Expired" status on page.

Order remains unpaid.

By implementing INXY, you provide your users with a modern, 24/7 payment rail that settles in seconds, ensuring your hosting or digital business stays ahead of the curve in 2026.

Would you like me to draft a series of social media posts to announce your new crypto payment options to your customers?

The Future of Global Commerce: Cross-Border Crypto Payments vs. Bank Transfers

The Future of Global Commerce: Crypto Payments vs. Traditional Banking The $190 trillion cross-border payment market is undergoing a systemic shift. While traditional SWIFT transfers remain the bedrock of trade, blockchain-based solutions are no longer just an alternative—they are a strategic imperative. Key Takeaways: Settlement Velocity: Moving from 3-5 business days to near-instant, 24/7/365 availability. Cost Optimization: Reducing transaction fees by 60% to 80% by removing intermediary "hops." Risk Mitigation: Eliminating chargeback fraud through blockchain immutability and transparent tracking. As we move toward a hybrid financial ecosystem, understanding these digital rails is essential for any global enterprise. Read our full analysis on how to future-proof your payment stack.

The global cross-border payment market is a staggering financial behemoth, moving approximately $190 trillion annually across the world's economies. For decades, this massive flow of capital has been heavily dominated by traditional financial institutions, operating on infrastructure originally designed in the pre-digital era. However, the legacy correspondent banking system is currently facing unprecedented, systemic disruption from blockchain technology and digital assets. As global commerce accelerates and borders become increasingly blurred in the digital age, the debate between Cross-Border Crypto Payments vs. Bank Transfers has become one of the most critical conversations in the fintech and crypto processing industry.

While traditional bank transfers remain the undisputed bedrock of global trade—largely due to their established regulatory frameworks, institutional trust, and systemic stability—crypto payments are rapidly gaining ground. Driven primarily by the rise of stablecoins and decentralized finance (DeFi) networks, these digital alternatives are emerging as a significantly faster, cheaper, and more inclusive alternative for businesses operating on an international scale.

For Chief Financial Officers, treasury managers, and e-commerce leaders, understanding the nuances of these two fundamentally different financial rails is no longer optional; it is a strategic business imperative. In this comprehensive, deep-dive guide, we will break down exactly how these two systems compare across key operational metrics, the roadblocks that remain, and how you can position your enterprise to leverage automated crypto processing for future growth.

Exploring the Great Divide: Cross-Border Crypto Payments vs. Bank Transfers

To truly understand the shifting paradigm in global finance, business leaders must look under the hood of how money actually moves across borders. The differences between legacy fiat rails and decentralized blockchain ledgers fundamentally alter how businesses manage cash flow, mitigate risk, and scale their operations globally. Let us examine the core operational differences.

1. The Mechanics of Speed and Settlement

Time is money, and in international trade, settlement delays can create cascading cash-flow bottlenecks that stifle growth, frustrate suppliers, and complicate supply chain management.

Traditional Bank Transfers: Traditional cross-border payments rely heavily on the SWIFT (Society for Worldwide Interbank Financial Telecommunication) messaging network and a highly complex "correspondent banking" model. Because it is logistically impossible for every bank in the world to hold direct, bilateral relationships with every other bank globally, a single international payment cannot simply travel from Point A to Point B. Instead, it often "hops" through multiple intermediary banks before reaching its final destination.

Timeframe: Because of these necessary intermediary hops, and the manual reconciliation required at each step, settlements typically take anywhere from 2 to 5 business days to clear.

Limitations: Traditional transactions are strictly bound by localized banking cut-off times, weekends, and regional bank holidays. If a company in London sends a payment to a supplier in Tokyo on a Friday afternoon, that payment will sit in limbo until the following Monday—or longer, if there is a local holiday. This creates highly unpredictable cash-flow gaps.

Crypto & Blockchain Payments: Blockchain networks operate on a fundamentally different, modern architecture: a decentralized, single-ledger system. This technology allows for direct, peer-to-peer (P2P) transfers that bypass traditional intermediary banks entirely.

Timeframe: Settlements on blockchain networks occur in a matter of seconds or minutes, regardless of the geographic distance between the sender and the receiver. For example, enterprise-grade networks like Ripple (XRP) or major fiat-backed stablecoins settle almost instantly.

Limitations (or lack thereof): Cryptocurrencies and blockchain networks operate 24/7/365. They do not sleep, they do not observe weekends, and they do not pause for national holidays. This effectively eliminates the delays caused by traditional operating hours, allowing businesses to execute just-in-time cross-border settlements.

Professional Takeaway: If your business relies on rapid inventory turnover or immediate supplier payments, integrating a crypto payment gateway to facilitate stablecoin settlements can drastically improve your working capital cycles.

2. Cost Efficiency and the Death of Intermediaries

Profit margins on international sales and B2B vendor payments are frequently eroded by the opaque and compounding costs associated with moving money across borders.

Traditional Bank Transfers: The multi-hop nature of correspondent banking means that each intermediary institution involved in the transfer process extracts its own toll. This can come in the form of a flat processing fee, an unfavorable foreign exchange (FX) spread, or a network messaging fee.

Impact: Transaction costs can be prohibitively high, especially for smaller retail payments, B2B micro-transactions, and remittances. According to recent data from the World Bank and the International Monetary Fund (IMF) [source: worldbank.org], high legacy banking fees remain one of the most significant barriers to global financial inclusion and frictionless international trade.

Crypto & Blockchain Payments: By systematically removing the middlemen from the transaction lifecycle, blockchain payments drastically reduce the costs associated with moving capital. The network validates the transaction programmatically, requiring only a small fraction of the fee traditionally charged by banks.

Impact: Comprehensive market research indicates that utilizing crypto or stablecoin rails can reduce cross-border transaction fees by a staggering 60% to 80%. This reduction is particularly transformative for the global remittance market and for small-to-medium enterprises (SMEs) that were previously priced out of efficient global trade due to prohibitive SWIFT fees. For businesses processing thousands of international transactions monthly, these savings directly, and heavily, impact the bottom line.

Professional Takeaway: Audit your current cross-border payment flows. Calculate the total annual cost of FX spreads and wire fees. For many e-commerce and SaaS platforms, migrating even 20% of cross-border volume to a crypto processing solution yields immediate, measurable ROI.

3. Security, Transparency, and Finality

How businesses track their funds in transit, and how they protect themselves from fraud, differs wildly between traditional banking and blockchain processing.

Traditional Bank Transfers: While the legacy banking system is highly secure, stringently regulated, and heavily insured, traditional transfers can be notoriously opaque for the end-user. Businesses often experience high levels of uncertainty regarding the exact status of a payment mid-transit. Furthermore, they frequently lack visibility into the final fees that will be deducted by intermediary banks before the funds arrive.

Additionally, traditional systems allow for chargebacks and settlement reversals. While designed to protect consumers, chargebacks pose significant administrative burdens and financial risks for online merchants who fall victim to "friendly fraud."

Crypto & Blockchain Payments: Blockchain ledgers are mathematically immutable. Once a transaction is algorithmically verified and recorded on the chain, it is permanent and cannot be altered, spoofed, or deleted.

Pros: This immutability provides total, unprecedented transparency. Anyone with the transaction hash can track the payment on the public ledger in real-time, eliminating the "where is my money?" anxiety. Furthermore, the irreversible nature of blockchain transactions entirely eliminates chargeback fraud—a massive relief for merchants, protecting businesses from unexpected revenue losses and malicious consumer behavior.

Cons: The absolute finality of the blockchain is a double-edged sword. If funds are mistakenly sent to the wrong wallet address due to human error, they are generally unrecoverable. Unlike a bank, there is no centralized customer service hotline to reverse an erroneous blockchain transaction.

Professional Takeaway: To mitigate the risk of lost funds via human error, utilize automated crypto payment gateways that generate dynamic, single-use QR codes and exact-amount payment links, removing the need for manual address entry by your clients.

Key Risks and Roadblocks to Mainstream Adoption

While crypto payments offer operational superiority in speed and cost, they face significant hurdles that prevent total mainstream displacement of traditional banking. A balanced fintech strategy must acknowledge and navigate these challenges.

1. The Volatility Dilemma Legacy cryptocurrencies like Bitcoin (BTC) or Ethereum (ETH) are highly speculative assets. A 10% price swing during a brief transaction window makes them highly impractical for standard corporate functions, such as payroll distribution or invoice settlements. This is exactly why the market is pivoting heavily toward stablecoins—digital assets pegged 1:1 to fiat currencies like the US Dollar, combining the technological speed of crypto with the economic stability of traditional money.

2. Regulatory Uncertainty & Compliance Protocols Traditional banks have spent decades building robust, globally recognized Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance frameworks. The pseudonymous nature of foundational cryptocurrencies complicates these essential compliance measures. Inconsistent, fragmented regulatory frameworks across different global jurisdictions make enterprise-level adoption risky for heavily audited corporations. Processing platforms must provide built-in compliance tools to bridge this gap safely.

3. Wholesale Dominance and Institutional Inertia Traditional financial systems are purpose-built to safely handle massive, multi-billion-dollar wholesale transactions between sovereign nations and multinational conglomerates. Currently, crypto payments represent only a small fraction of total global volume, primarily capturing retail, SME, and remittance flows. Unseating a $190 trillion entrenched system takes time.

The Future: Convergence Over Replacement

The consensus among top economic researchers and fintech analysts is that blockchain will not immediately replace traditional bank transfers; rather, the two systems are destined to integrate. We are moving toward a hybrid financial ecosystem.

Major financial institutions are already adopting blockchain infrastructure to modernize their own rails. For instance, J.P. Morgan has developed its own blockchain networks to facilitate 24/7 cross-border settlements for institutional clients. Additionally, global authorities and central banks are heavily researching and piloting Central Bank Digital Currencies (CBDCs). These sovereign digital assets aim to combine the speed, transparency, and efficiency of blockchain technology with the absolute trust, stability, and regulatory backing of traditional fiat money.

The future of the fintech processing industry lies in interoperability—systems that allow a business to accept a payment in a stablecoin from a client in Brazil, and have it instantly settled as fiat in a corporate bank account in Europe, entirely seamlessly.

Automating Business Processes with INXY

Navigating the transition from legacy finance to digital assets doesn't have to be a logistical nightmare. To stay competitive, modern businesses need payment infrastructure that is as dynamic and global as their customer base.

At INXY, we understand that navigating the complexities of Cross-Border Crypto Payments vs. Bank Transfers requires robust, reliable, and secure technology. Our cutting-edge payment gateway solutions are designed specifically to help forward-thinking enterprises automate their business processes, effortlessly bridging the gap between traditional fiat banking and the emerging crypto economy.

Whether you are looking to eliminate exorbitant SWIFT fees, accept cross-border stablecoin payments with zero volatility risk, or implement comprehensive cross-domain tracking for your payment flows, INXY provides the enterprise-grade infrastructure to make it happen seamlessly.

Ready to modernize your financial stack and expand your global reach without the friction of traditional banking? Explore our comprehensive suite of payment gateway solutions atINXY.io and discover how we can tailor an automated crypto processing strategy for your specific business needs. Contact our integration team today to future-proof your payment operations.

Why Businesses Are Choosing Bitcoin for Payroll and Contractor Payments

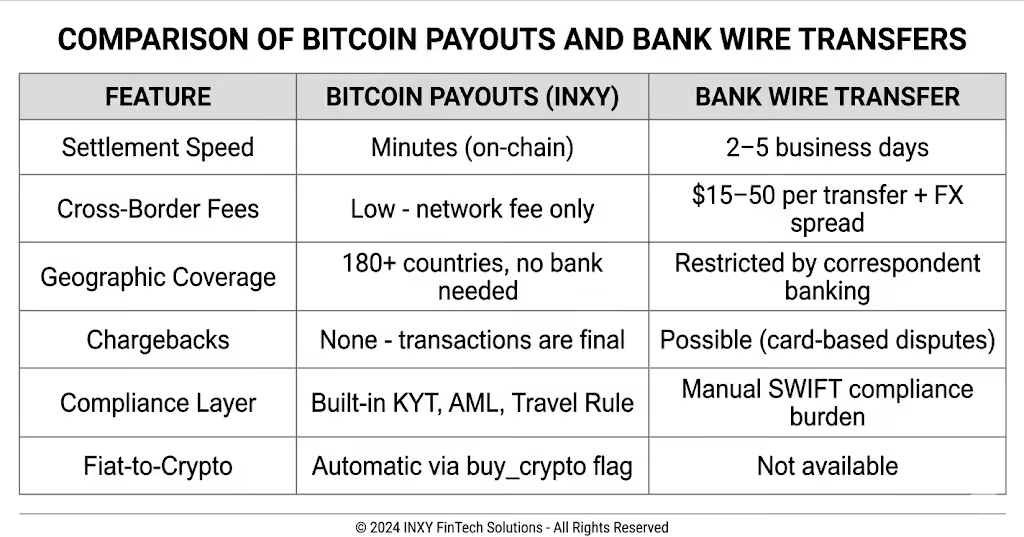

As remote work becomes the global standard, companies face a common challenge: paying international teams through traditional banking is slow, expensive, and geographically limited. Bitcoin payouts eliminate SWIFT delays, excessive conversion fees, and banking restrictions — letting businesses pay employees and contractors in Bitcoin within minutes, regardless of their location.

From affiliate networks and iGaming platforms to SaaS companies and freelancer marketplaces, paying in Bitcoin is no longer a niche practice. Paying employees in Bitcoin and contractors in BTC is no longer reserved for crypto-native startups — it is a competitive edge in global talent acquisition that reduces operational costs across the board. INXY Payments makes this straightforward: no need to buy Bitcoin in advance, no separate exchange accounts, no manual compliance work — everything runs through a single B2B platform built for exactly this use case.

How to Pay Employees in Bitcoin with INXY: 3 Simple Steps

Create an INXY Account & Complete KYB — Sign up as a business, submit your company documents, and pass KYB verification through the INXY dashboard. Your organisation is reviewed and activated within 1–3 business days — no crypto expertise required.

Add Recipients or Connect the Payouts API — Upload a CSV file with recipient BTC addresses via the INXY dashboard, or integrate the Payouts API directly into your platform for fully automated workflows. The API is built to handle payouts at scale — no hard limit on the number of recipients per cycle. Real-time webhook notifications keep your system updated on each payout status.

Send BTC Payouts — from Crypto or Fiat — Trigger single or mass BTC payouts from your balance. If you hold EUR or USD, INXY's buy_crypto flag auto-converts your fiat to Bitcoin at the moment of each payout — no pre-purchased BTC required, no exchange accounts to manage.

Benefits of Bitcoin Payouts for Business

Global Reach Without Banking Limits

Bitcoin payouts via INXY work for recipients in any country, with or without a bank account. No correspondent bank fees, no SWIFT delays, no rejected transfers due to local banking restrictions. Your payroll operates globally, on your schedule.

No Chargebacks

Crypto transactions are final and immutable. Once a BTC payout is broadcast to the network, it cannot be reversed or disputed — a critical advantage for high-volume affiliate and iGaming payouts where chargeback fraud is a constant risk.

Instant Settlement

BTC payouts initiated through INXY are broadcast on-chain within minutes. Compared to international wire transfers that take 2–5 business days, Bitcoin delivers settlement speed that matches the pace of modern business operations.

Pay from Fiat, Send in Bitcoin

If your treasury operates in EUR or USD, there is no need to pre-purchase Bitcoin on an exchange. INXY's buy_crypto feature handles the fiat-to-BTC conversion automatically at the moment each payout is triggered — the exchange rate is locked at execution time, and the full flow is recorded in your transaction history.

Built-In Compliance — KYT, AML, Travel Rule

Every BTC payout processed through INXY goes through KYT (Know Your Transaction) screening before broadcast. High-risk addresses are blocked automatically. For recipients in your Contact List, Travel Rule data exchange via Notabene is handled by the platform — no manual compliance burden on your team.

Who Uses Bitcoin Payouts?

Affiliate Networks & CPA Platforms

Affiliate networks need to pay hundreds or thousands of publishers worldwide, often weekly or bi-weekly. INXY supports batch processing of up to hundreds of recipients per API call, with full webhook notifications on payout status. Mass payouts that previously took 5 banking days now complete in minutes — and companies that pay employees and contractors in Bitcoin report significantly lower operational overhead.

iGaming & Online Gaming Platforms

Gaming and gambling platforms regularly pay out winnings and contractor fees in crypto. Bitcoin is the preferred payout currency for many players and partners due to its universal recognition and broad wallet support. INXY's compliance layer — KYT screening, AML review, Travel Rule — ensures platforms stay clean without building their own infrastructure.

Remote-First Companies & Tech Teams

Companies with globally distributed engineering, design, or operations teams use INXY to offer Bitcoin as an alternative compensation option. Contractors who prefer crypto over bank transfers get paid faster, while the company avoids currency conversion overhead and cross-border banking fees.

Freelancer Marketplaces & Gig Economy Platforms

For platforms managing large pools of independent contractors, mass Bitcoin payouts through INXY reduce the operational cost of international payroll significantly. One file upload or one API call pays thousands of contractors in a single batch — with per-recipient status tracking and exportable CSV reports.

Frequently Asked Questions

Is it legal to pay employees in Bitcoin?

In most jurisdictions, paying contractors in Bitcoin is fully legal. For full-time employees, regulations vary: many countries — including the US, UK, and EU member states — allow crypto salary supplements or contractor payments in crypto, but typically require that the minimum statutory wage be paid in local fiat currency. Consult local labour law before switching your primary payroll to Bitcoin.

Can you pay employees in Bitcoin in the US?

Yes. The Fair Labor Standards Act (FLSA) requires that the federal minimum wage be paid in US dollars, but additional compensation — including contractor payments and performance bonuses — can be made in Bitcoin. Many US-based companies and DAOs already pay freelancers and contractors in BTC without legal issues.

Which companies pay employees in Bitcoin?

A growing number of global businesses pay employees and contractors in Bitcoin, particularly in tech, gaming, and affiliate marketing industries. Remote-first companies, crypto-native startups, and platforms with large contractor networks were early adopters. With infrastructure like INXY, any B2B business can now add BTC payouts without building crypto capabilities in-house.

How does INXY's buy_crypto flag work for BTC payouts?

If your INXY balance is in EUR or USD, the buy_crypto: true flag triggers an automatic fiat-to-BTC exchange at the moment each payout is initiated. The exchange rate is locked at execution time, and the network fee is deducted from the payout amount. You do not need to hold Bitcoin in advance — INXY handles the conversion in the same transaction flow.

What happens if a BTC address is flagged as high-risk?

Before any payout is created, INXY screens the recipient's BTC address through KYT. If the address is flagged as high-risk, the payout is blocked automatically and you receive an error notification via webhook and dashboard. You can review the case and contact the INXY compliance team if needed.

What is the maximum number of Bitcoin payouts per batch?

INXY's infrastructure handles payout cycles of any size — from small partner networks to programs with hundreds of recipients — all processed in minutes, with full webhook notifications on each transaction.

Start Sending Bitcoin Payouts with INXY

Ready to pay your global team in Bitcoin? Join hundreds of businesses that use INXY Payments to run fast, compliant BTC payouts — from a single contractor to thousands of recipients. No crypto expertise required, no pre-purchased Bitcoin needed, no separate exchange accounts.

Get Started with INXY — Free Setup

Already have an account? Go to Send Crypto → Payouts in your INXY dashboard.