Best Payment Gateways for SaaS in 2026: From Traditional Fiat to Web3

Stop letting legacy payment bottlenecks kill your SaaS growth. 🚀 In 2026, relying solely on traditional credit card processing is a risk to your cash flow. High fees and chargebacks are outdated. Our latest guide breaks down the best payment gateways for B2B SaaS—from the reliability of Stripe to the borderless power of INXY Paygate. Inside this guide: Why crypto users have a 2x higher LTV and prefer annual plans. How the Auto-Convert Engine eliminates volatility risks for CFOs. The secret to Zero Chargebacks and instant global settlements. Future-proof your billing stack and tap into a global market of 800M+ digital asset users. Read more at INXY.io.

When closing high-ticket B2B SaaS deals or enterprise annual plans, traditional credit card processing often becomes a bottleneck rather than a solution. High cross-border fees and unexpected fund holds can paralyze your cash flow. In 2026, relying solely on legacy fiat processors is a risk. Your billing infrastructure needs to be as borderless and scalable as your software.

As we move deeper into 2026, SaaS billing has fundamentally evolved. While traditional fiat processors remain standard, the explosive demand for borderless, low-fee digital transactions makes cryptocurrency and stablecoin gateways a mandatory addition to any modern B2B tech stack. This guide breaks down the best payment gateways for SaaS businesses, comparing legacy providers with next-generation Web3 infrastructure to help you optimize your upfront revenue.

Key Features to Look for in a SaaS Payment Gateway

Before diving into the top providers, it is essential to define what makes a payment gateway effective for a SaaS and annual licensing model:

- Global Reach & Multi-Currency: Support for international clients without exorbitant cross-border foreign exchange (FX) fees.

- API & Native Integrations: Developer-friendly REST APIs and plugins for standard platforms (like WooCommerce, Shopify, or WHMCS).

- Chargeback Protection: Mechanisms to protect your business from fraudulent chargebacks that persistently plague the digital goods industry.

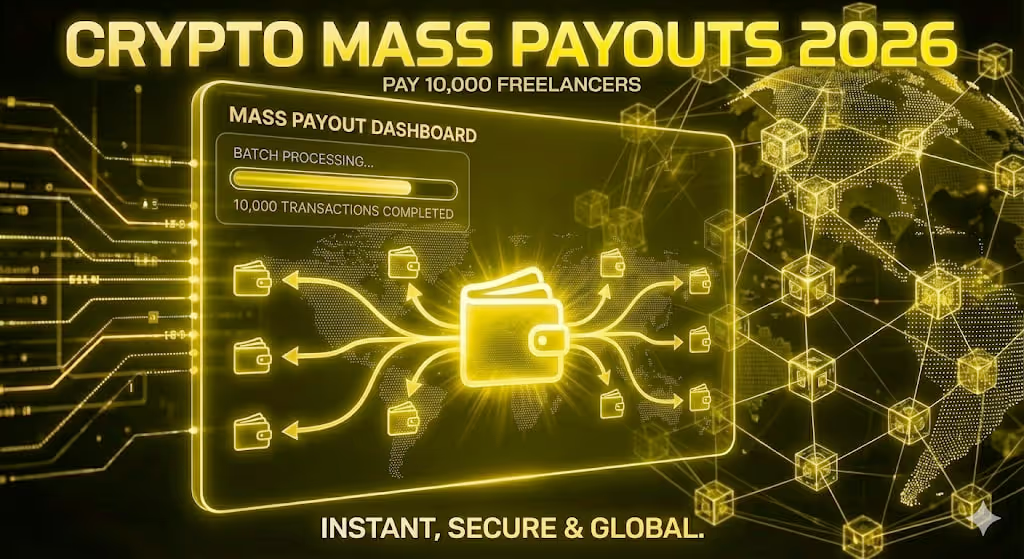

- Mass Payout Capabilities: Built-in tools to easily distribute affiliate commissions or international contractor payouts.

The Top Payment Gateways for SaaS in 2026

1. Stripe: The Traditional Fiat Giant

Stripe remains a dominant force in the SaaS ecosystem. Its robust API, advanced invoicing tools, and seamless checkout flows make it a default choice for many domestic startups.

- Pros: Incredible developer tools, widespread consumer trust, and deep analytics.

- Cons: High cross-border transaction fees and persistent vulnerability to chargeback fraud.

2. PayPal / Braintree: The Consumer Favorite

Braintree (owned by PayPal) offers extensive global brand recognition. It is an excellent choice for B2C software products looking for high conversion rates at checkout from everyday consumers.

- Pros: High consumer trust, easy integration, supports Venmo and Apple Pay.

- Cons: Strict compliance algorithms that can freeze funds without warning, high processing fees for international clients.

3. INXY Paygate: The Premier Web2 to Web3 Bridge

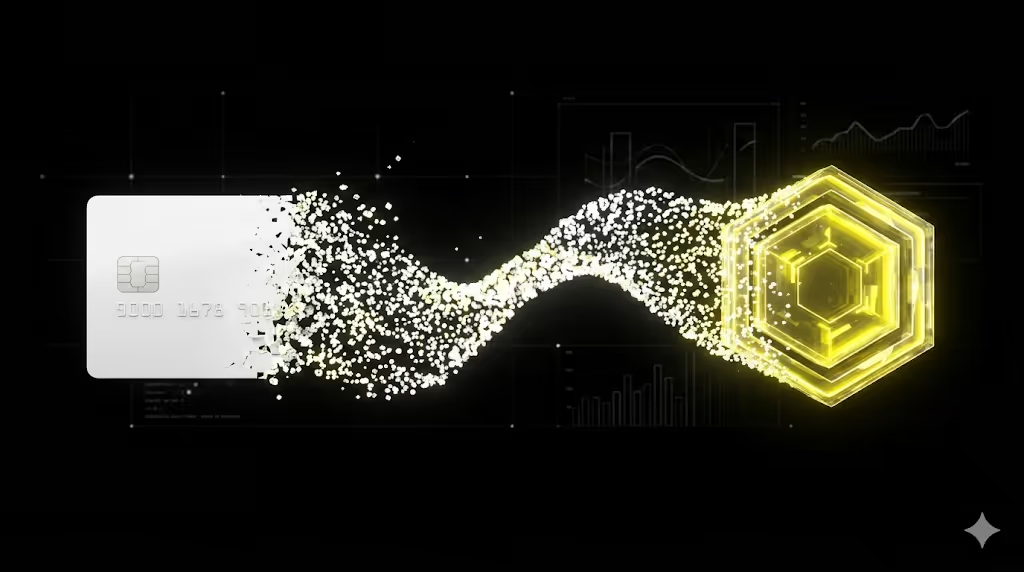

For modern SaaS companies, relying solely on traditional banking is a massive bottleneck. Enter INXY, a regulated, VC-backed cryptocurrency payment gateway that recently secured $3M from Flashpoint VC. INXY is specifically engineered for B2B enterprises and SaaS platforms looking to accept global payments without the friction of legacy banks. INXY acts as a seamless bridge, allowing you to offer a "Pay with Crypto" option while completely eliminating the technical risks normally associated with digital assets.

Boost Your Annual Payments: INXY Paygate strategically bypasses standard auto-billing. This is a massive advantage designed to boost your upfront cash flow. When dealing with high-ticket B2B software and large sums, utilizing stablecoins makes annual tariff plans the absolute most profitable option for both your business and your clients. You get the full yearly value immediately without the risk of monthly drop-offs.

- The Auto-Convert Engine: The biggest fear for SaaS CFOs is crypto volatility. With INXY, if a client pays a $1,000 or $10,000 annual software license in Ethereum, the gateway's Auto-Convert feature instantly converts the incoming volatile asset into stablecoins (USDT/USDC) or fiat (EUR/USD). You get exact, predictable revenue.

- Native SaaS Integrations: Instead of writing complex smart contracts, SaaS companies can use INXY’s robust APIs or ready-made plugins, including a native WHMCS module perfectly tailored for hosting, cloud services, and digital agencies.

- Zero Chargebacks: Blockchain transactions are irreversible, meaning your business is completely protected from friendly fraud.

- Built-in Mass Payouts: If you rely on an affiliate network, INXY allows you to automate global mass payouts via CSV uploads or API.

Feature Comparison Matrix

Choosing the right platform depends entirely on your target audience. Here is a high-level comparison of how these gateways stack up:

Why SaaS Businesses Are Adopting Crypto Invoicing

The shift toward stablecoin billing is not a temporary trend; it is a fundamental upgrade to global financial infrastructure. With over 824 million people globally owning crypto—representing more than 10% of the world's population—this is a massive, highly lucrative demographic ready to spend.

By integrating a Web3 gateway alongside your traditional fiat processors, you unlock several strategic advantages:

- Massive Upfront Cash Flow: 60% of crypto users prefer to pay upfront for 12–36 month plans, compared to only 20% of credit card users.

- Higher Spend & Unmatched LTV: Crypto buyers spend 2x more than traditional users. In fact, 43% of users spend more simply because crypto is offered as an option. Clients who pay in crypto consistently become the highest Lifetime Value (LTV) users—paying more and staying longer.

- New Customer Acquisition: 40% of crypto clients are entirely new to the merchant, and 56% of users actively choose to shop more frequently at crypto-friendly businesses.

- Lower Transaction Costs: Traditional gateways charge 2.9% + $0.30 per transaction, plus heavy cross-border fees. Crypto payments settle for fractions of a percent, saving high-volume companies thousands of dollars on annual contracts.

- Instant Global Settlement: Instead of waiting 3 to 5 business days for an international wire transfer to clear, stablecoin payments settle in minutes.

Conclusion: Future-Proof Your SaaS Billing

In an increasingly borderless digital economy, restricting your customers to legacy credit card processing is a critical mistake. While platforms like Stripe and Braintree excel in their respective domestic markets, the future of global SaaS billing relies on secure, instant, and borderless transactions.

By implementing a specialized gateway, you can bypass the traditional hurdles of international finance. You gain the ability to tap into a high-spending demographic, automate your affiliate mass payouts, and completely eliminate chargeback fraud—all while receiving predictable, auto-converted fiat or stablecoin settlements. It is time to expand your checkout options and embrace the next generation of digital payments.

.avif)