Blog

In this dedicated blog page, we invite you to explore a wealth of knowledge, expertise, and inspiration that transcends traditional boundaries.

INXY Raises $7M to Expand Cross-Border Payment Infrastructure

INXY has secured new funding to continue building its global payments platform. The total round reached $7M. The company focuses on stablecoin infrastructure for businesses. Its tools help companies accept crypto and send payouts while keeping accounting in fiat.

INXY has secured new funding to continue building its global payments platform. The total round reached $7M.

The company focuses on stablecoin infrastructure for businesses. Its tools help companies accept crypto and send payouts while keeping accounting in fiat.

This funding comes at a time when global payments are changing. Traditional rails are slow and expensive. Cross-border transfers often take days and include multiple intermediaries.

Stablecoins offer a different path. They move value quickly and directly. They reduce friction in international transactions. Many businesses are starting to explore this model.

INXY builds infrastructure for this shift. The goal is simple. Let companies use crypto without becoming crypto companies.

The platform supports mass payouts, payment acceptance, and automated conversion. Funds can be sent globally and settled in EUR or USD.

The company has already processed over $2B in annual stablecoin volume. This shows growing demand for alternative payment rails.

The new capital will be used to:

– Expand the payments infrastructure.

– Strengthen compliance and regulatory alignment.

– Grow the team and product capabilities.

Regulation is also shaping the market. In Europe, frameworks like MiCA are creating clearer rules for crypto services. This makes it easier for businesses to adopt compliant solutions.

INXY positions itself in this new environment as a regulated infrastructure provider. It operates under EU and Canadian frameworks and focuses on low-risk business use cases.

The company believes the future of payments will be stablecoin-based, compliant, and invisible to the end user.

The work ahead is not about hype. It is about making payments simple, reliable, and global.

Articles

Is USDT Safe for Business Payments? Tether's Reserves, Risks & Regulation in 2026

If your business is about to move real money through USDT, "is USDT safe?" is the right question to ask first. Tether is the largest stablecoin in the world — roughly $188 billion in circulation and ~59% of the entire stablecoin market as of mid-2026 — but scale and safety aren't the same thing.

If your business is about to move real money through USDT, "is USDT safe?" is the right question to ask first. Tether is the largest stablecoin in the world — roughly $188 billion in circulation and ~59% of the entire stablecoin market as of mid-2026 — but scale and safety aren't the same thing.

This is a balanced look at what actually backs USDT, where the real risks sit, and how those risks apply specifically to a company using Tether for payouts rather than trading.

What USDT is — and what "safe" means here

USDT (Tether) is a stablecoin designed to hold a 1:1 peg to the US dollar. Each token is meant to be redeemable for one dollar, backed by reserves Tether holds. For a business, "safe" breaks into three practical questions:

- Peg risk — will 1 USDT still be worth ~$1 when my recipient cashes out?

- Counterparty risk — is the issuer solvent and are the reserves real?

- Operational and regulatory risk — can I legally and reliably use it where I operate?

Let's take them in order.

Peg stability: strong, with rare wobbles

In normal conditions, USDT trades within a fraction of a cent of $1. Its depth of liquidity is unmatched — it's the most traded crypto asset on earth, which makes the peg resilient.

It is not immune, though. During acute market stress (the 2022 Terra/UST collapse, the 2023 US regional-bank episode) USDT briefly de-pegged by a few percent before recovering. For a payout business, the takeaway is not "avoid USDT" but "don't sit on large idle balances." If you convert at payout time rather than warehousing Tether, short-lived wobbles rarely reach the recipient.

Reserves: what backs USDT in 2026

This is where scrutiny has historically been sharpest, and where transparency has improved.

Per Tether's Q1 2026 attestation (BDO Italia), the company reported roughly $191.8 billion in total assets against its liabilities, with a reserve mix heavily weighted toward liquid, low-risk holdings:

- ~$135 billion in US Treasuries — the bulk of reserves in the most liquid safe asset there is.

- ~$13 billion in gold, plus Bitcoin and other holdings.

- Reported net equity of around $8 billion, a buffer above the tokens in circulation.

Two honest caveats remain:

- Tether publishes attestations, not a full audit by a Big Four firm. An attestation confirms balances at a point in time; it's less rigorous than a continuous audit. Critics have pushed Tether on this for years.

- A minority of reserves has historically included assets beyond cash and Treasuries. The direction of travel is toward higher-quality, more liquid reserves, but it's worth knowing what you hold.

For most businesses, a reserve base dominated by US Treasuries is reassuring. The transparency gap versus a fully audited competitor is real but narrowing.

Regulatory risk: the biggest practical issue for EU businesses

Here's the risk that most directly affects where and how you can use USDT: Tether did not seek authorization under the EU's MiCA regulation.

The consequences are concrete. Through late 2024 and 2025, MiCA-regulated exchanges removed USDT for customers in the European Economic Area — Coinbase, Crypto.com, Binance (EEA) and others delisted or restricted it — because offering a non-authorized stablecoin put their own licenses at risk. USDT trading volumes on EU venues fell sharply, while MiCA-compliant alternatives like USDC and EURC gained share.

USDT is not banned to hold, but its regulated on/off-ramp availability in the EU has narrowed. Tether has instead pursued a US federal path (under the GENIUS Act) via a US-domiciled entity. If your recipients or your business are EU-based, this matters: a MiCA-compliant stablecoin may be the more durable choice for European corridors. (See "Is USDC regulated?" and our USDT vs USDC comparison.)

Operational risk: irreversibility and wrong-network errors

Independent of Tether the company, USDT carries the operational risks of any on-chain asset:

- Irreversibility. A payout sent to a wrong or wrong-network address is typically gone.

- Network fragmentation. USDT on Tron, Ethereum, Solana and others isn't interchangeable at the address level.

- Compliance exposure. Paying a sanctioned or high-risk wallet is a legal problem, not just a technical one.

These are managed with address validation, test transfers, and — at volume — KYT and sanctions screening built into your payout flow.

So, is USDT safe for business payouts?

A fair summary:

- Peg: Strong in normal conditions; convert at payout time to avoid stress-window exposure.

- Reserves: Large and Treasury-heavy, but attested rather than fully audited.

- Regulation: The real watch-item — limited MiCA standing constrains EU usage.

- Operations: Safe when you use validation, screening, and disciplined records.

For high-volume global payouts, USDT remains the most liquid and widely accepted stablecoin. The smart posture is to use it deliberately: don't warehouse it, screen your recipients, keep clean fiat records, and choose a MiCA-compliant asset where European regulation demands it.

Frequently asked questions

Is USDT backed by real dollars? USDT is backed by reserves that, per Tether's 2026 attestations, are dominated by US Treasuries plus cash equivalents, gold, and other assets. These are confirmed by attestation rather than a full independent audit.

Can USDT lose its peg? It can briefly deviate during extreme market stress, as it has a few times historically, but it has recovered each time. Deep liquidity supports the peg in normal conditions.

Is USDT legal in the EU? Holding USDT is not illegal, but Tether is not MiCA-authorized, and many EU-regulated exchanges have delisted it for EEA users. For EU corridors, a MiCA-compliant stablecoin is often more practical.

Is USDT safe enough for payroll and affiliate payouts? For most businesses, yes — provided you convert near payout time, screen recipients, and keep proper records. The controls matter as much as the asset.

Use USDT with the controls built in

The safest way to use USDT for business isn't to trust a single wallet — it's to run payouts through infrastructure that screens recipients, validates networks, and reports in fiat. That's how INXY's mass USDT payouts are designed: fund in EUR or USD, pay out globally, and keep audit-ready records — without warehousing crypto risk.

This article is general information, not financial or legal advice. Evaluate stablecoin exposure against your own jurisdiction and risk policy.

USDT Network Fees Compared: TRC-20 vs ERC-20 vs BEP-20 vs Solana vs TON (2026)

USDT is a single asset, but it lives on more than a dozen blockchains — and the network you choose can change the cost of a transfer by 100x or more. For a one-off payment that's a rounding error. For a business sending thousands of payouts a month, picking the wrong chain quietly burns thousands of dollars.

USDT is a single asset, but it lives on more than a dozen blockchains — and the network you choose can change the cost of a transfer by 100x or more. For a one-off payment that's a rounding error. For a business sending thousands of payouts a month, picking the wrong chain quietly burns thousands of dollars.

This is a practical breakdown of the cheapest network to send USDT in 2026, what drives the fee on each chain, and how to match the network to the payout.

Why USDT fees vary so much

The fee to move USDT has nothing to do with Tether itself. It's the network's gas fee — paid in the chain's native token — that varies:

- On Ethereum (ERC-20) you pay ETH gas, which is priced by network congestion and can spike sharply.

- On Tron (TRC-20) you pay in TRX energy/bandwidth, which is low and stable.

- On Solana, TON, and BNB Chain, base fees are engineered to be very small.

So "how much does it cost to send USDT" is really "which network did you send it on."

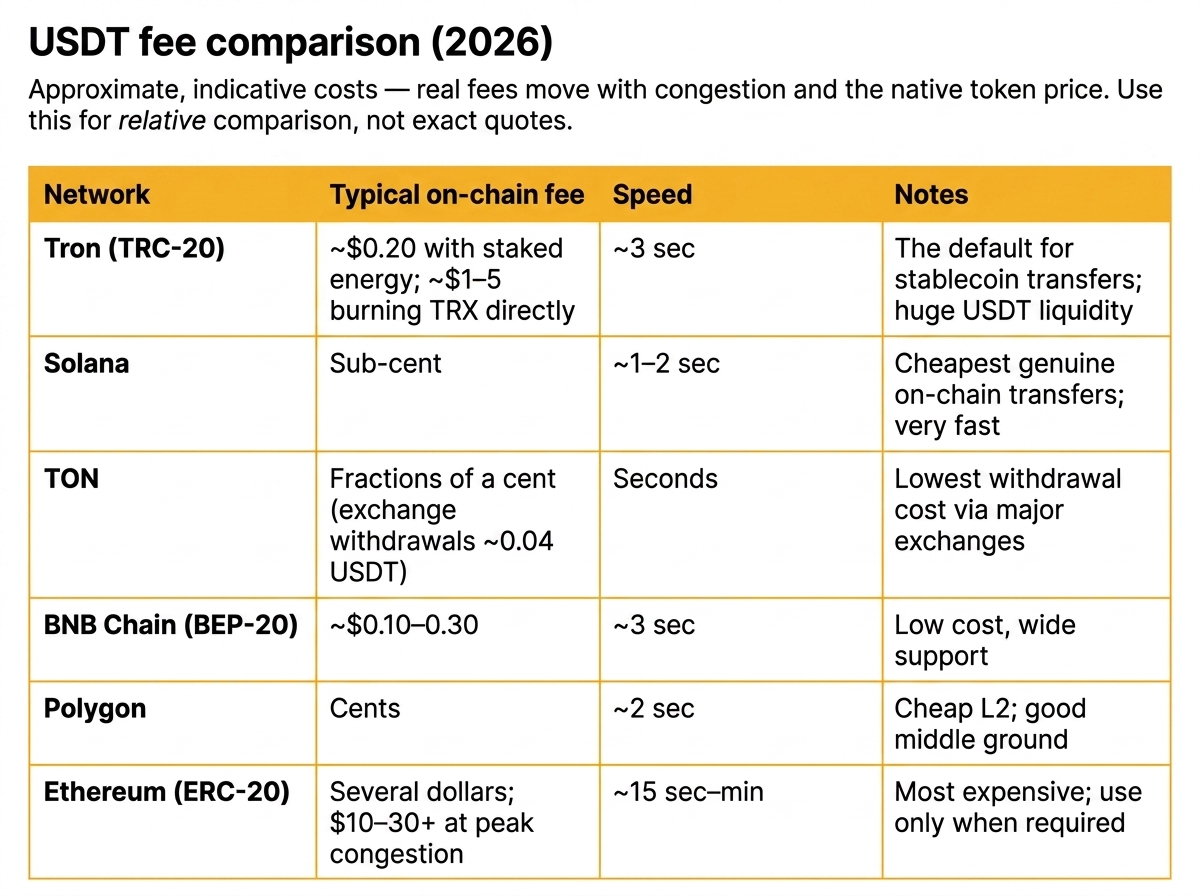

USDT fee comparison (2026)

Approximate, indicative costs — real fees move with congestion and the native token price. Use this for relative comparison, not exact quotes.

The short version: for pure on-chain cost, Solana and TRC-20 lead, with TON unbeatable for exchange withdrawals. ERC-20 is the most expensive and should be reserved for recipients who specifically need it.

Match the network to the payout amount

Cheapest isn't always "correct." The right network depends on the size of the transfer and where the recipient wants the funds.

- Micro-payouts (under ~$50): TRC-20, Solana, or TON. Fees would otherwise eat a meaningful slice of the payment.

- Standard payouts ($50–$5,000): Solana, Polygon, or TRC-20 keep costs to pennies while settling fast.

- Large transfers (over ~$5,000): Cost matters less relative to the amount. ERC-20 is acceptable if the counterparty requires it — the $10–20 fee is small against the principal, and Ethereum's liquidity and integrations are unmatched.

Beyond the headline fee

Fee-per-transfer is the obvious number. Three others matter just as much at scale:

1. Recipient acceptance. The cheapest network is useless if the recipient's wallet or exchange doesn't support it. Always confirm the network before sending — cross-network mistakes are irreversible.

2. Native-token overhead. Every network needs its gas token in your wallet. Running payouts across five chains means monitoring and topping up five different balances — an operational cost that doesn't show up in the per-transfer fee.

3. Failed and stuck transfers. Underpriced gas on congested networks means stuck transactions and support tickets. Reliability has a cost, too.

How platforms cut costs further

When you run payouts through a fiat-native platform instead of manually, network fees stop being your problem in two ways:

- Automatic routing. The platform sends each payout on a supported low-fee network without you managing gas on every chain.

- No native-token juggling. You fund a balance in EUR or USD; the provider handles conversion and gas. Your reporting stays in fiat.

That removes the hidden operational cost of multi-chain payouts, not just the visible per-transfer fee.

Frequently asked questions

What is the cheapest network to send USDT? For on-chain self-custody transfers, Solana and Tron (TRC-20) are cheapest, and TON offers the lowest withdrawal fees on major exchanges. Ethereum (ERC-20) is the most expensive.

Is TRC-20 always the cheapest for USDT? Not always. TRC-20 is very cheap and has the deepest USDT liquidity, but Solana and TON can be cheaper still per transfer. TRC-20 remains the most widely accepted low-fee option.

Why is sending USDT on Ethereum so expensive? ERC-20 transfers pay ETH gas, priced by network demand. During congestion, a single USDT transfer can exceed $30 in gas.

Does the network affect how much USDT the recipient receives? The network sets the fee you pay to send. Choosing a low-fee chain means more of your budget reaches recipients, especially across many small payouts.

Can I send USDT across networks? An address is tied to one network. To move USDT between chains you need a bridge or an exchange — you can't send TRC-20 USDT directly to an ERC-20 address.

Send on the right network, automatically

If you're running regular USDT payouts, you shouldn't be managing gas tokens across five blockchains. INXY's mass USDT payouts route each transfer over low-fee networks and report everything back in EUR or USD — so you get the cheapest path without the multi-chain overhead. New to bulk sending? Start with our step-by-step USDT payout guide.

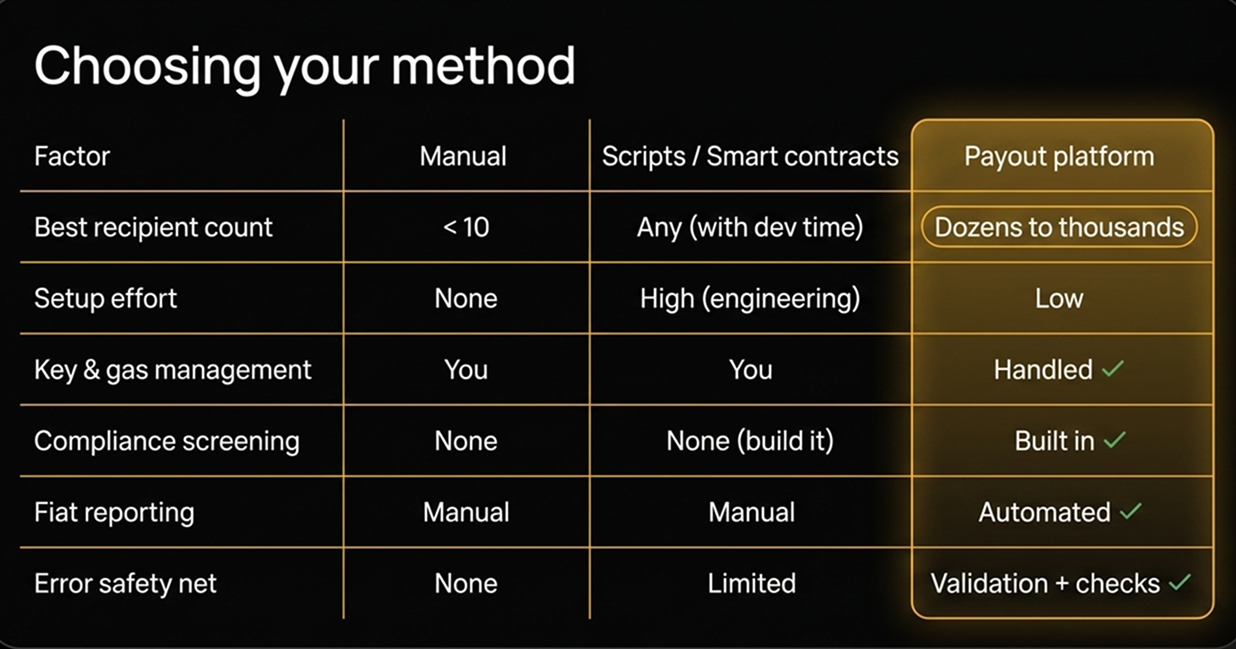

How to Send USDT to Multiple Wallets: A Step-by-Step Bulk Payout Guide

Manual works for a handful of payees; scripts work if you want to run infrastructure. If you'd rather send USDT to hundreds or thousands of recipients from a fiat balance — with screening and clean reporting built in — that's exactly what INXY's mass USDT payouts are built for.

Paying twenty affiliates, two hundred contractors, or two thousand players one transaction at a time does not scale. If you need to send USDT to multiple wallets, the method you choose determines your cost, your error rate, and how much of your finance team's week disappears into copy-pasting addresses.

This guide covers the three practical ways to run a bulk USDT transfer in 2026 — manual, scripted, and platform-based — with the trade-offs of each, the mistakes that cost real money, and how to keep clean records for accounting.

What "mass USDT payout" actually means

A mass USDT payout is a single, structured operation that distributes Tether to many recipients at once. Instead of initiating each transfer by hand, you prepare a list of addresses and amounts and process them as a batch.

Three things make this harder than it looks:

- Network choice. USDT exists on Tron (TRC-20), Ethereum (ERC-20), BNB Chain (BEP-20), Solana, TON, Polygon and others. A recipient's address is network-specific — send TRC-20 USDT to an ERC-20 address and the funds are typically lost.

- Fees at volume. A fee that looks trivial for one transfer becomes a line item when multiplied across thousands of recipients.

- Reconciliation. Finance needs a fiat value, a timestamp, and a transaction hash for every payout — not just a wall of blockchain data.

Keep these three in mind; every method below is really a different answer to them.

Method 1: Manual transfers from a wallet or exchange

The simplest approach is to send USDT one recipient at a time from a self-custody wallet (MetaMask, Trust Wallet, Tronlink) or an exchange account.

When it works: fewer than ~10 recipients, infrequent payouts, no automation budget.

Steps:

- Confirm each recipient's network and address in writing. Never assume the network.

- Fund your wallet with enough USDT and the native gas token (TRX for TRC-20, ETH for ERC-20, and so on).

- Send each transfer, double-checking the first and last four characters of every address.

- Save each transaction hash against the recipient's name for your records.

The catch: manual sending does not scale and has no safety net. A single mistyped address is irreversible. There is no batch confirmation, no built-in fiat reporting, and no sanctions screening. Beyond a handful of recipients, error risk climbs fast.

Method 2: Scripts and smart-contract batching

Technical teams can automate payouts with the blockchain's own tooling — a script that loops through a recipient list, or a "multisend" / "disperse" smart contract that pushes many transfers in one on-chain transaction.

When it works: you have engineering resources, a stable set of networks, and you want control over the flow.

What you gain:

- Batching efficiency. Multisend contracts bundle many recipients into a single transaction, which can reduce total gas versus sending individually on some networks.

- Full automation. A script can pull addresses from your database and fire payouts on a schedule.

What you take on:

- Key management. Your script needs access to a funded hot wallet holding private keys — an operational and security liability.

- Gas handling. You must monitor and top up the native token on every network you use.

- No compliance layer. Scripts don't screen recipients against sanctions lists or flag high-risk addresses. That's on you.

- Accounting glue. You still have to convert on-chain data into fiat-denominated records your auditors will accept.

Scripting trades human error for engineering overhead. It's powerful, but you are now running payment infrastructure as a side project.

Method 3: A payout platform (CSV or API)

A dedicated payout platform abstracts the wallet, keys, gas, and networks away. You upload a CSV of recipients or call an API, and the platform handles conversion, routing, screening, and delivery.

When it works: recurring payouts, dozens to thousands of recipients, finance teams that need clean fiat reporting, and businesses that don't want to become a crypto operation.

How a typical batch runs:

- Fund in fiat or stablecoin. Top up a balance — with a provider like INXY you can fund in EUR or USD via SEPA or SWIFT, so you never have to source crypto yourself.

- Upload or connect. Submit a CSV (recipient, amount, network) or send the batch through the API.

- Automated checks. The platform runs KYT and sanctions screening, auto-converts, and routes each payout to the right network.

- Recipients get paid. Delivery happens in minutes on supported low-fee networks.

- Report in fiat. You get batch-level exports with fiat values, fees, payout IDs, and transaction hashes — ready for reconciliation.

The trade-off is that you rely on a provider, but you remove key management, gas operations, compliance gaps, and accounting cleanup in one move.

Five mistakes that cost real money

- Wrong network. The most common irreversible loss. Always match the recipient's network to the address.

- Forgetting gas. A wallet full of USDT can't move without the native token for fees.

- No test transfer. For a new large recipient, send a small amount first and confirm receipt.

- Skipping screening. Paying a sanctioned or high-risk address is a legal and banking risk, not just a crypto one.

- Weak records. If you can't tie every hash to a fiat value and a recipient, month-end close becomes painful.

Frequently asked questions

Can I send USDT to many wallets in one transaction? On some networks, yes — a "multisend" smart contract bundles multiple recipients into one on-chain transaction. Otherwise, batching is handled off-chain by a platform that submits the transfers for you.

What's the cheapest way to send USDT in bulk? Low-fee networks such as Tron (TRC-20), Solana, and TON dramatically reduce per-transfer cost versus Ethereum. See our full USDT network fees comparison.

Do I need to hold crypto to run USDT payouts? Not with a fiat-native platform. You can fund in EUR or USD, keep your accounting in fiat, and let the provider handle conversion and delivery.

Is bulk USDT sending safe? The transfer itself is irreversible, so accuracy matters. Reputable platforms add address validation, KYT, and sanctions screening to reduce risk — protections that manual and script-based methods lack.

Scale it without the overhead

Manual works for a handful of payees; scripts work if you want to run infrastructure. If you'd rather send USDT to hundreds or thousands of recipients from a fiat balance — with screening and clean reporting built in — that's exactly what INXY's mass USDT payouts are built for.

MiCA Is Here: How INXY Built a Multi-Jurisdiction Model — and Migrated Every Client Before July 1

1 July 2026. Today marks the beginning of a new chapter for Europe's digital asset industry. The transitional period under the EU's Markets in Crypto-Assets Regulation (MiCA) has ended, and the standard for operating a crypto business in Europe has been raised for good.

1 July 2026. Today marks the beginning of a new chapter for Europe's digital asset industry. The transitional period under the EU's Markets in Crypto-Assets Regulation (MiCA) has ended, and the standard for operating a crypto business in Europe has been raised for good.

For years, much of the industry was built around a single jurisdiction. One license. One operating model. That worked while the rules were still evolving. It works less well now.

We want to be transparent with our clients about where INXY stands and what we did about it. INXY did not obtain a MiCA authorization in Poland. So rather than depend on any single jurisdiction, we moved to a multi-jurisdiction operating model — and before 1 July, we completed the migration of every client off our Polish entity. No payments paused. No settlement stopped.

Here's what MiCA is, what changed on 1 July, and how our model is built to keep your payments running through moments exactly like this one.

What is MiCA?

MiCA (Markets in Crypto-Assets Regulation) is the European Union's comprehensive framework for regulating crypto-assets and the companies that provide crypto services. It replaces a patchwork of national rules with a single, harmonized rulebook across all 27 member states.

In practice, MiCA does three main things:

- Licenses providers. Any company offering crypto-asset services — custody, exchange, transfers, payouts — must be authorized as a Crypto-Asset Service Provider (CASP) by a national regulator. A CASP license can then be "passported" across the EU.

- Regulates stablecoins. Issuers of stablecoins ("e-money tokens") must be authorized and hold strict, fully-backed reserves. This is why compliant stablecoins like USDC and EURC stayed available on EU-regulated venues while non-authorized ones were delisted. (More on this in "Is USDC regulated?")

- Sets conduct and transparency standards for how services are marketed and delivered.

MiCA's rules for service providers began applying on 30 December 2024, with a transitional window for existing firms.

What changed on 1 July 2026

MiCA included a transitional ("grandfathering") period under Article 143. Firms already operating legally under national regimes before 30 December 2024 could continue serving clients — but only until they obtained a CASP license or until 1 July 2026, whichever came first. That date has now passed, and there is no extension mechanism in the regulation.

From today, any provider serving EU clients must hold a MiCA CASP authorization. A legacy national registration no longer provides cover.

The situation in Poland made this especially clear. Poland has not yet enacted the national Crypto-Asset Market Act needed for its regulator (KNF) to issue CASP licenses — the act has been vetoed repeatedly, most recently in June 2026. In practice, that left Polish-registered providers with no domestic path to a CASP license before the deadline.

The limits of a single-jurisdiction model

MiCA is not simply making it harder to launch a crypto business. It is redefining what it means to run one: no longer just "get a license and go," but "operate reliably inside a regulated financial system."

That shift began well before 1 July. Across the market, some companies are spending the coming months restructuring. Some are migrating clients. Some are rethinking how they serve Europe altogether. The common thread is that betting an entire operation on one jurisdiction has become a single point of failure.

INXY's response: a multi-jurisdiction operating model

For payment infrastructure providers, continuity is not optional. Payments cannot pause because the regulatory landscape changes. Businesses still need to settle funds. Cross-border commerce continues every day. Infrastructure should adapt so that businesses don't have to.

That is why INXY expanded beyond a single jurisdiction and built a multi-jurisdiction operating model, spanning:

- Canada — registered Money Services Business (FINTRAC MSB M23375535)

- El Salvador

- Cyprus

- Switzerland

We did not build this because a deadline forced our hand at the last minute. We built it because our B2B clients need reliability that does not depend on the regulatory status of any one country. When the Polish route closed, that model is what let us complete the migration of all clients off our Polish entity before 1 July 2026 — with no interruption to payouts, settlement, or reporting.

What this means for you

- Your service continues. Clients were migrated ahead of the deadline and are served through our appropriately licensed entities. There is no gap in payouts or settlement.

- Your funds and reporting are unaffected. Fiat-denominated reporting, payout records, and reconciliation continue exactly as before.

- Your compliance standards are unchanged. Full KYB, KYC where needed, real-time transaction monitoring (KYT), and sanctions screening remain in force across every jurisdiction we operate in.

Regulation is becoming the foundation, not the obstacle

One conclusion runs through all of this: regulation is no longer just about compliance. It is becoming the foundation that enables institutional adoption of stablecoin infrastructure at scale. The businesses that treat regulatory resilience as core infrastructure — not paperwork — are the ones that will serve the next phase of the market.

That's the central theme of our latest research, Stablecoins 2026: The New Global Financial Settlement Layer, which maps the regulatory landscape and what it means for businesses building on stablecoin rails. (Link / request the report: [add URL].)

Frequently asked questions

Did INXY obtain a MiCA license? No. INXY did not obtain a MiCA authorization in Poland. Instead of relying on a single jurisdiction, we operate a multi-jurisdiction model across Canada, El Salvador, Cyprus, and Switzerland, chosen to give our B2B clients continuity.

What happened to clients on the Polish entity? All clients were migrated off our Polish entity before 1 July 2026. The migration was completed ahead of the MiCA transitional deadline, with no interruption to payments.

What is MiCA, in simple terms? MiCA is the EU's single set of rules for crypto companies and crypto-assets. It requires service providers to be licensed as CASPs and sets strict standards for stablecoins, consumer protection, and transparency across all member states.

What happened on 1 July 2026? MiCA's transitional period ended. From this date, providers serving EU clients must hold a MiCA CASP license; legacy national registrations no longer provide cover.

Will my payments pause? No. Continuity was the entire point of moving to a multi-jurisdiction model. Client migration was completed before the deadline, and settlement continues without interruption.

Talk to us

Regulatory change raises real questions for any business that moves money across borders. If you'd like to understand how our multi-jurisdiction model supports your payouts, contact our team — and we'd be glad to share our perspective as the industry enters this new phase.

This update is provided for information and does not constitute legal advice. Regulatory details are accurate as of 1 July 2026 and may evolve.

Crypto Checkout That Converts: Reducing Drop-off on Stablecoin Payments

You added crypto checkout to win new buyers — but the payment page is quietly leaking them. This guide breaks down exactly where stablecoin payments lose customers: network confusion, price-lock anxiety, wallet friction, unclear confirmations, and surprise fees. Learn the design and infrastructure fixes that turn a leaky pay page into one that converts — including why a well-built crypto checkout can beat cards, clearing ~99.9% of attempts with no chargebacks.

You added a crypto checkout to capture a new segment of buyers, and the demand is real — but the payment page is leaking customers. A shopper picks crypto, lands on the pay screen, hesitates, and disappears. That gap between intent and completed payment is checkout drop-off, and on crypto rails it has its own specific causes that most teams never diagnose.

This guide breaks down where stablecoin payments lose customers, the friction points that drive abandonment, and the concrete design and infrastructure choices that turn a leaky pay page into one that converts. The goal is simple: every shopper who chooses crypto should finish paying.

Why crypto checkouts lose customers

A crypto checkout is not just a card form with different logos. It introduces steps a Web2 buyer has never seen — choosing a network, copying an address, waiting for confirmations — and every unfamiliar step is a place to quit. Unlike a card decline, which the customer understands, a stalled or confusing crypto payment feels risky, and risk kills conversion.

Where drop-off actually happens

Most teams treat the checkout as a single event. It isn't. Crypto payment drop-off clusters at four distinct stages:

- Method selection — the customer considers crypto but doesn't trust it on your site, so they bounce before starting.

- Network and asset choice — faced with "ERC20 / TRC20 / BEP20" they don't recognize, they freeze.

- Wallet action — copying an address or scanning a QR code, switching apps, and fearing a mistake.

- Confirmation wait — the payment is sent but the page gives no clear signal it worked.

You cannot fix abandonment you can't see. Instrument each of these stages separately before changing anything.

Why a one-point conversion gain is worth chasing

Checkout is the highest-leverage surface you own. Traffic, ads, and product pages all exist to deliver a customer to this screen. Recovering even a few percentage points of crypto payment conversion rate here costs nothing in additional traffic — it simply stops you paying for visitors you then lose at the last step. For a business processing meaningful volume, a high-conversion gateway is not a nice-to-have; it is the difference between crypto being a growth channel and a vanity feature.

The main causes of stablecoin payment drop-off

Network and asset confusion

The single biggest source of friction is choice the customer can't evaluate. Asking a non-technical buyer to select between Tron, Ethereum, BNB Chain, and Polygon — each with different fees and speeds — is asking them to make a decision they're unqualified to make. Hesitation becomes abandonment.

Volatility and price-lock anxiety

If the amount due appears to move while the customer reads it, they assume they'll overpay or underpay. Even with stablecoin payments, buyers worry the quote will expire or shift. Without a visibly locked rate, the page feels unsafe.

Wallet friction and manual errors

Copy the address. Switch to the wallet app. Paste. Check the network matches. Confirm the gas. Send. Switch back. Each handoff is a chance to abandon — and the fear of sending funds to the wrong address or wrong chain is enough to make cautious buyers stop entirely.

Slow or unclear confirmation

A customer who has paid but sees a spinning loader with no explanation assumes the worst. On-chain confirmation times vary by network, and a checkout that doesn't explain the wait — or sets no expectation for it — converts the final, already-committed moment into a drop-off. (For the underlying mechanics, see our guide on how long crypto withdrawals and confirmations take.)

Fees, minimums, and surprise costs

A network fee that appears only at the final step, or a minimum the customer trips over, reads as a bait-and-switch. Surprise costs at the moment of payment are one of the most reliable abandonment triggers in any checkout — crypto included.

Missing trust and compliance signals

Crypto still carries a perception of risk for mainstream buyers. A pay page with no licensing, security, or brand reassurance gives a nervous customer every reason to close the tab. Trust is not decoration here; it is a conversion input.

How to design a crypto checkout that converts

Invoice in fiat, settle in stablecoins

Let the customer see the price in the currency they think in — EUR or USD — and pay in crypto behind the scenes, with automatic conversion to stablecoins or fiat on your side. This removes mental math, neutralizes volatility, and lets a Web2 buyer treat the transaction like any other payment. It is the foundation of a converting crypto checkout.

Reduce choices and default to the right network

Don't make the customer a blockchain expert. Pre-select a fast, low-fee network as the default and present asset options in plain language ("Pay with USDT" rather than "TRC20"). Fewer decisions mean fewer exit points. Every option you remove from the critical path is a conversion you keep.

Lock the rate and show a countdown

Display a fixed amount due with a clear, time-boxed quote ("This price is locked for 15:00"). A visible countdown does two things at once: it removes price anxiety and creates gentle urgency that pulls the customer through. Certainty converts.

Make the confirmation state legible

Tell the customer exactly what's happening: "Payment detected — confirming on-chain. This usually takes under a minute." Replace ambiguous spinners with a status that names the step and sets a time expectation. The moment after a customer pays is the worst possible time to leave them guessing.

Add fallback paths

Some customers will start a crypto payment and stall. Offer a clean way to switch methods or retry without losing the cart. A dead-end on a failed or abandoned crypto payment is a guaranteed loss; a graceful fallback recovers a share of it.

Build trust into the page

Show licensing and security signals where the customer makes the decision. INXY operates as licensed and regulated payment infrastructure with AML/KYB controls and partners including Sumsub, Elliptic, and Crystal — the kind of compliance signal that reassures a cautious buyer at exactly the right moment. Surface it; don't bury it in a footer.

Conversion benchmarks: crypto vs cards

When the checkout is built well, crypto doesn't just match card conversion — it can beat it. The structural advantages are real:

Cards fail far more often than most merchants realize — declines, 3-D Secure friction, and cross-border blocks routinely cost 5–30% of attempts. Crypto settlement is final and irreversible, which removes chargebacks entirely and lets a well-designed gateway clear close to every legitimate attempt. For merchants serving Europe, Asia, and LatAm, that reliability is a direct conversion uplift — INXY reports helping customers increase conversion rates by up to 40%. (For a wider comparison of providers and rails, see best payment gateways for SaaS in 2026.)

A pre-launch checklist

Before you ship a crypto checkout, confirm it does all of the following:

- Prices in the customer's fiat currency, with conversion handled automatically.

- Defaults to a fast, low-fee network instead of forcing a choice.

- Locks the rate with a visible countdown.

- Shows total cost up front, including any network fee — no surprises at the last step.

- Names the confirmation step and sets a time expectation.

- Offers a retry or fallback for stalled payments.

- Displays trust and compliance signals on the pay page itself.

- Tracks drop-off by stage, not just overall completion.

How INXY reduces crypto checkout drop-off

INXY's high-conversion API paygate is built around the principles above. Customers are invoiced in fiat and pay in crypto, with automatic conversion to stablecoins or fiat to remove volatility risk. You get settled in your bank account — in EUR or USD — as soon as the next day, with full reporting and an accounting-friendly setup for Web2 companies. The gateway supports 20+ cryptocurrencies across major networks (ERC20, TRC20, BEP20, Polygon, Tron, TON, and more), charges below 1% per transaction with no setup or hidden fees, and is engineered for a ~99.9% success rate.

The result is a checkout your customers finish — built to convert, not just to accept. Add it to your checkout page, webstore, platform, or app via API integration, or book a demo to see the conversion data for your business model.

FAQ

What causes drop-off on crypto checkouts? The most common causes are network and asset confusion, price-lock anxiety, manual wallet friction, unclear confirmation states, surprise fees, and missing trust signals. Each maps to a specific stage of the checkout, so the fix starts with measuring drop-off stage by stage rather than as a single number.

How do stablecoin payments improve checkout conversion? Stablecoins remove volatility from the transaction, so the amount due stays fixed while the customer pays. Pairing that with fiat-denominated pricing and automatic conversion lets a mainstream buyer complete a crypto payment as easily as a card payment — without exposure to price swings.

Is crypto checkout conversion really higher than cards? It can be. Crypto payments have no chargebacks and final settlement, and a well-built gateway can clear close to 99.9% of legitimate attempts versus 70–95% typical card success. The advantage is largest for cross-border and emerging-market customers, where cards are frequently declined or restricted.

Which network should a crypto checkout default to? Default to a fast, low-fee network so customers don't have to choose. Stablecoins on high-throughput networks settle in seconds for a fraction of the cost of slower chains, which both speeds confirmation and reduces the fee shown at checkout.

How do I add a high-conversion crypto checkout to my site? Use a payment gateway with API integration that handles fiat pricing, network selection, rate locking, and conversion for you. INXY integrates with your existing checkout, webstore, or app, and settles to your bank in EUR or USD — see get started.

Losing customers at the crypto pay page? Explore INXY's high-conversion payment gateway and turn stablecoin checkout into a channel that converts.

The Travel Rule for Crypto Payouts: What B2B Senders Must Know in 2026

The Travel Rule requires sender and recipient identity data to accompany crypto transfers, and in 2026 it directly affects any business paying contractors, suppliers, or partners in crypto. This guide breaks down the regulatory picture by region — the EU's no-threshold TFR, the US $3,000 BSA rule plus new GENIUS Act stablecoin obligations, and FATF's $1,000 baseline — and the exact originator/beneficiary data each payout must carry, including the extra step for self-hosted wallets. It then shows how a regulated crypto gateway runs pre-send screening, KYT/AML checks, and the Travel Rule inside the payout flow, so B2B senders stay compliant without building their own compliance stack.

If your business sends crypto payouts — to contractors, suppliers, affiliates, or partners — the crypto Travel Rule now sits between you and every transfer. It is the single piece of kyc aml crypto payments regulation most likely to delay, freeze, or return a B2B payout in 2026, and most senders only learn about it after a payment is held. This guide explains what the Travel Rule is, how the 2026 rules differ by region, what data must accompany each payout, and how a regulated crypto gateway runs the checks so you don't have to build a compliance stack yourself.

What the crypto Travel Rule is (and why it now applies to your payouts)

The Travel Rule is an anti-money-laundering standard that requires identifying information about the sender (originator) and recipient (beneficiary) to "travel" alongside a transfer of value. It originated in traditional banking and now applies to crypto.

FATF Recommendation 16, extended to crypto

The rule comes from the Financial Action Task Force (FATF), whose Recommendation 16 was extended in 2019 to cover virtual assets. The principle is simple: when a regulated provider moves crypto on a customer's behalf, it must collect, transmit, and retain originator and beneficiary details so that law enforcement can trace funds. FATF recommendations are influential but not law in themselves — each jurisdiction decides how to implement them, which is why the picture is fragmented (more on that below).

Who counts as a VASP — and when you are the originator

The obligation falls on Virtual Asset Service Providers (VASPs): exchanges, custodial wallet providers, and crypto payment gateways. When your business initiates a payout through such a provider, the provider is the "originating institution" and carries the Travel Rule duty — but it can only meet that duty with your data. In practice this means the gateway must know who you are paying and why, and you must be able to supply recipient details on demand. The compliance burden is shared: the provider operates the machinery, but incomplete sender data is the most common reason a payout stalls.

The 2026 regulatory picture: crypto compliance and regulations by region

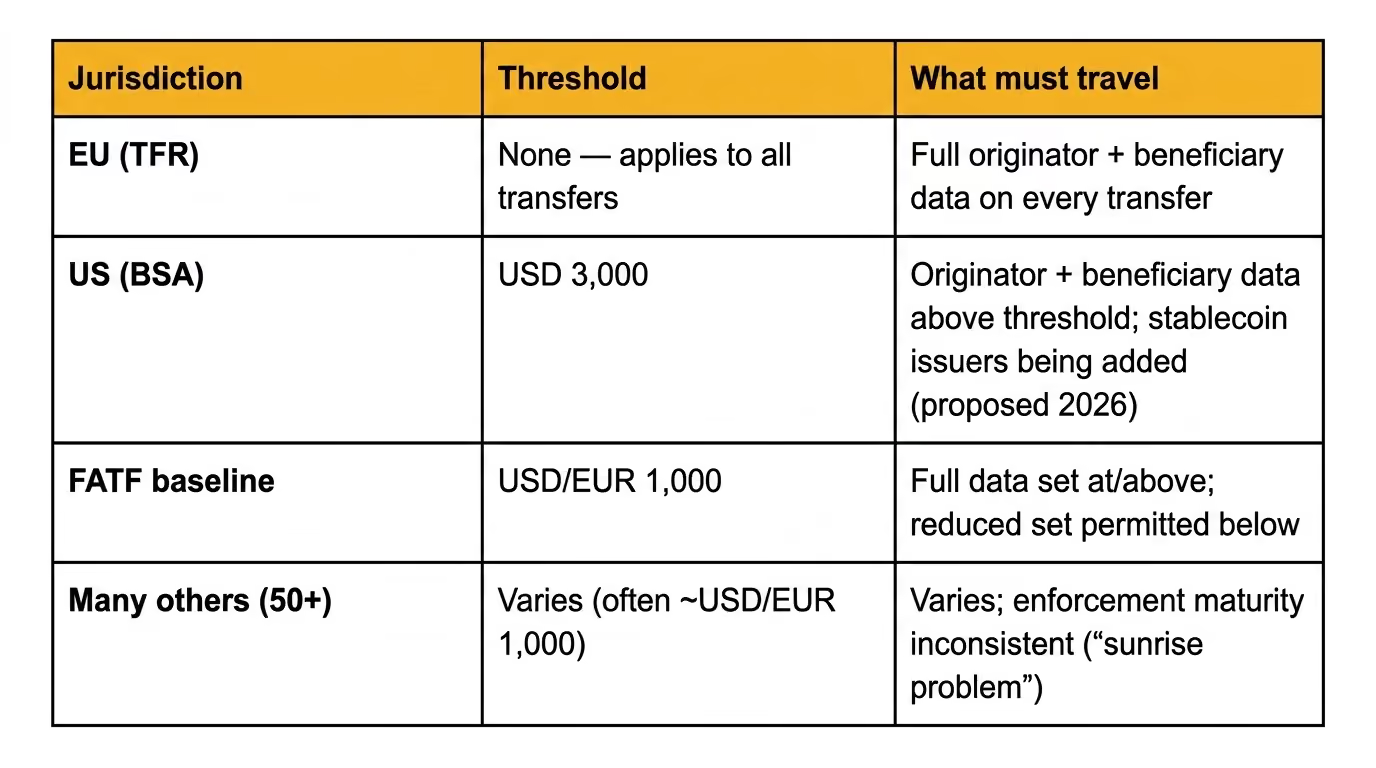

By 2026, over 50 jurisdictions have enacted Travel Rule legislation — roughly 73% of FATF-assessed jurisdictions, up from a far smaller base two years earlier. Enforcement maturity, thresholds, and required data still vary widely, so a payout that is routine in one corridor can be blocked in another.

EU — Transfer of Funds Regulation (TFR), no de-minimis threshold

The EU's recast Transfer of Funds Regulation (TFR) took effect on 30 December 2024. It is the strictest major regime: full originator and beneficiary data must accompany every crypto-asset transfer handled by a regulated provider, with no minimum threshold. A €5 payout and a €500,000 payout carry the same data obligation. The TFR operates alongside MiCA, the EU's broader crypto-asset framework, which governs licensing of providers.

US — Bank Secrecy Act Travel Rule, USD 3,000 threshold

In the United States the Travel Rule lives under the Bank Secrecy Act (BSA), administered by FinCEN, with a threshold of USD 3,000 — notably higher than FATF's recommendation. A 2026 development matters for stablecoin senders: following the GENIUS Act (signed July 2025), the U.S. Treasury proposed a rule on 8 April 2026 treating permitted stablecoin issuers as BSA financial institutions, subject to AML programs, recordkeeping, and the Travel Rule, with compliance expected around April 2027. The direction of travel is clear — stablecoin rails are being pulled fully into the same compliance perimeter as the banking system.

FATF global threshold and the "sunrise problem"

FATF recommends a standard threshold of USD/EUR 1,000, below which a reduced data set may apply. Because jurisdictions adopt the rule at different speeds, the industry faces the "sunrise problem": a compliant provider in a regulated market may need to send Travel Rule data to a counterparty in a market that has not yet implemented the rule and cannot receive it. For B2B senders this means a payout's success can depend on the recipient platform's jurisdiction, not just your own.

What data must "travel" with a B2B crypto payout

The required data set is consistent across regimes, even where thresholds differ.

Required originator (sender) fields

- Name of the originator (your business or the paying entity).

- Wallet address used for the transfer (or a transaction reference).

- Physical/registered address, and in some regimes an official identifier or account number.

Required beneficiary (recipient) fields

- Name of the recipient.

- Wallet address receiving the funds.

In addition, the transaction amount, execution date, and a unique transaction identifier are recorded with every transfer. For your operations, the practical takeaway is that recipient name + wallet must be accurate and verifiable before you send — a mismatch is a hold.

Self-hosted (unhosted) wallet payouts — the extra step

Paying out to a self-hosted (non-custodial) wallet — common when paying contractors or partners who hold their own keys — changes the mechanics. There is no counterparty VASP to receive the Travel Rule message, so the data isn't transmitted onward; instead, your provider must still collect originator and beneficiary information from you, and above the relevant threshold may require verification of wallet ownership based on a risk assessment. Expect to attest that the recipient controls the destination address for larger payouts.

How a regulated crypto gateway runs the Travel Rule on outbound payouts

This is where a regulated crypto gateway earns its keep. Rather than connecting to Travel Rule messaging protocols, screening providers, and sanctions lists yourself, the gateway runs the controls inside the payout flow. Using INXY's outbound model as a concrete example, an outgoing payout passes through several gates before any transfer is created.

Pre-send checks — address risk and blacklist screening

A payout starts as a withdrawal request, not an immediate send. A pre-send validation stage runs first and can stop the operation with an error so that no transaction is ever formed. As part of this, the recipient address is looked up against historical risk data: a previously unseen address is treated cautiously, while a known address carries its last risk result. This means a problematic payout is caught at draft stage, not after funds have left.

KYT/AML screening of the recipient

Next is the outbound KYT (Know Your Transaction) sequence. The recipient address is checked against a blacklist; a match fails the request outright with no transaction created. If it clears, a risk provider screens the address and returns an outcome:

- Low or Medium → the payout draft passes and proceeds.

- High → the request fails, no transaction is created, and an error is returned.

This is the kyc aml crypto payments layer working in real time on the money leaving your account.

The Travel Rule message exchange

Only after screening passes does the Travel Rule step run, packaging and exchanging the required originator/beneficiary information with the counterparty provider where one exists. The payout then proceeds to settlement. The sequence matters: screen first, transmit data, then send.

Approved contacts and recipient allow-lists

Gateways typically maintain a contact list of approved recipients. A recipient flagged as declined blocks the payout regardless of other checks — a useful control for finance teams that want a vetted, reusable set of payees for recurring or mass payouts.

KYB is the gate to the platform; KYT is the gate to each transaction; the Travel Rule is the data that rides along with it. A gateway that handles all three is what "secure crypto payments" actually means in operational terms.

Compliance risks of getting payouts wrong

For a B2B sender, Travel Rule failures are not abstract — they hit cash flow and counterparties directly:

- Held or returned transfers. Missing or mismatched recipient data is the most common cause of a stalled payout. Funds can sit in review or be returned, delaying contractor and supplier payments.

- Counterparty refusal. If the receiving platform can't accept Travel Rule data (the sunrise problem) or flags your transfer, it may bounce the payment.

- Regulatory exposure. Operating outbound flows without proper screening and recordkeeping exposes the business to AML penalties — increasingly so as stablecoin issuers are folded into BSA-style obligations.

- Operational drag. Building and maintaining screening, sanctions, and Travel Rule messaging in-house is expensive and never "done," because rules and thresholds keep shifting.

How to automate crypto payouts without owning the compliance stack

The practical answer for most B2B senders is to run payouts through a regulated crypto gateway that treats the Travel Rule, KYT, and sanctions screening as part of the payout itself — not as something you bolt on.

With INXY, every outbound payout passes through pre-send validation, blacklist and KYT risk screening, and the Travel Rule step before settlement, and recurring payees can be managed through an approved contact list. Because the same flow is exposed via API and webhooks, you can run mass payouts — paying hundreds of contractors or partners at once — with compliance checks applied per recipient automatically, and receive status events back into your own systems. That is what "how to automate crypto payouts" looks like when compliance is built in rather than improvised.

If compliance posture is your priority, start with INXY's security & compliance capabilities; if payout mechanics are the focus, see crypto payouts and the cross-border and payroll options that build on the same rails.

FAQ

Does the Travel Rule apply to stablecoin payouts? Yes. Stablecoin transfers handled by a regulated provider are subject to the Travel Rule like any other virtual asset. In the EU, full data is required regardless of amount; in the US, stablecoin issuers are being brought explicitly into BSA Travel Rule obligations under a rule proposed in April 2026.

What is the Travel Rule threshold in 2026? It depends on the jurisdiction. FATF recommends USD/EUR 1,000; the US applies USD 3,000 under the BSA; the EU applies no threshold — every transfer carries full data.

Do I need to collect data for self-hosted (unhosted) wallet payouts? Yes. Even though there's no counterparty provider to receive the message, your gateway must still collect originator and beneficiary information, and above the relevant threshold may require proof that the recipient controls the destination wallet.

Is the Travel Rule the same as KYC? No. KYC/KYB verifies identity at onboarding. The Travel Rule governs the transmission of identity data alongside each transfer. They work together but are distinct obligations.

Who is responsible — the sender or the recipient platform? Both sides carry obligations. The originating provider must collect and transmit sender/recipient data; the beneficiary provider must receive and retain it. As the business initiating the payout, you're responsible for supplying accurate recipient information to your provider.

News

.avif)

INXY Releases Cinematic Short Film on the Future of Global Mass Payouts

Unlock Global Scale: Meet INXY Payments at Affiliate World Asia in Bangkok

Let’s work together

See how easy it is to start with crypto payments without interrupting your current business flow

By clicking "Accept", you agree to the storing of cookies on your device to enhance site navigation, analyze site usage, and assist in our marketing efforts. View our Privacy Policy for more information.